The information in this preliminary prospectus supplement and the accompanying prospectus is not complete and may be changed. This preliminary prospectus supplement and the accompanying prospectus are not an offer to sell these securities and we are not soliciting an offer to buy these securities in any state where the offer or sale is not permitted.

Filed pursuant to Rule 424(b)(5)

Registration No. 333-166328

SUBJECT TO COMPLETION, DATED MAY 31, 2011

PRELIMINARY PROSPECTUS SUPPLEMENT To Prospectus dated May 5, 2010

8,700,000 Shares

Cheniere Energy, Inc.

Common Stock

We are offering to sell 8,700,000 shares of our common stock, par value $0.003 per share. Our common stock is listed on the NYSE Amex Equities, or AMEX, under the symbol “LNG.” The last reported sale price on AMEX on May 27, 2011 was $11.56.

We have granted the underwriter the right to purchase up to 1,300,000 additional shares of common stock to cover any over-allotments. The underwriter can exercise this right at any time within 30 days after the offering.

Investing in our common stock involves risks, including those described under “Risk Factors” beginning on page S-9 of this prospectus supplement.

We are selling to the underwriter the shares of common stock at a price of $ per share, resulting in net proceeds to us, before deducting expenses related to the offering, of $ , or $ assuming full exercise of the underwriter’s option to purchase additional shares.

The underwriter proposes to offer the shares of common stock from time to time for sale in negotiated transactions or otherwise, at market prices prevailing at the time of sale, at prices related to such prevailing market prices or at negotiated prices.

The underwriter expects to deliver the shares of common stock to investors on or about June , 2011.

Neither the Securities and Exchange Commission nor any state securities commission has approved or disapproved these securities or determined if this prospectus supplement or the accompanying prospectus is accurate or complete. Any representation to the contrary is a criminal offense.

Credit Suisse

The date of this prospectus supplement is June , 2011

PROSPECTUS SUPPLEMENT

| i | ||||

| ii | ||||

| ii | ||||

| iii | ||||

| iii | ||||

| S-1 | ||||

| S-9 | ||||

| S-28 | ||||

| S-29 |

| S-30 | ||||

| S-31 | ||||

| S-44 | ||||

| Certain United States Federal Income Tax Consequences to Non-U.S. Holders |

S-48 | |||

| S-51 | ||||

| S-56 | ||||

| S-56 |

| PROSPECTUS | ||||

| 1 | ||||

| 1 | ||||

| 1 | ||||

| 2 | ||||

| 3 | ||||

| 10 |

| 21 | ||||

| 22 | ||||

| 22 | ||||

| 23 | ||||

| 25 | ||||

| 25 |

ABOUT THIS PROSPECTUS SUPPLEMENT

This prospectus supplement, which describes the terms of this offering of shares of our common stock, supplements the accompanying prospectus, which provides more general information. Generally, when we refer to the prospectus, we are referring to this prospectus supplement and the accompanying prospectus combined. If the description of this offering varies between this prospectus supplement and the accompanying prospectus, you should rely on the information in this prospectus supplement. This prospectus supplement contains information about the shares of our common stock offered in this offering and may add to, update or change the information in the accompanying prospectus. Before you invest in shares of our common stock, you should carefully read this prospectus supplement, along with the accompanying prospectus, in addition to the information contained in the documents incorporated by reference into this prospectus supplement and referred to under the heading “Where You Can Find More Information.”

We have not, and the underwriter has not, authorized anyone to provide you with any information that is not contained in or incorporated by reference into this prospectus supplement or in any related free writing prospectus filed with the Securities and Exchange Commission, or SEC. If anyone provides you with different or inconsistent information, you should not rely on it. We are offering to sell, and seeking offers to buy, shares of our common stock only in jurisdictions where offers and sales are permitted. The information contained in this prospectus supplement is accurate only as of the date of this prospectus supplement, regardless of the time of delivery of this prospectus supplement or any sale of our common stock. Our business, financial condition, results of operations and prospects may have changed since that date.

i

In this prospectus supplement, unless the context otherwise requires:

| • | Bcf means billion cubic feet; |

| • | Bcf/d means billion cubic feet per day; |

| • | LNG means liquefied natural gas; |

| • | LNG train means an independent modular unit for gas liquefaction; |

| • | MMBtu means million British thermal units; |

| • | Mtpa means million metric tons per annum; and |

| • | TUA means terminal use agreement. |

CAUTIONARY STATEMENT REGARDING FORWARD-LOOKING STATEMENTS

This prospectus supplement, the accompanying prospectus and the documents incorporated herein by reference contain certain statements that are, or may be deemed to be, “forward-looking statements” within the meaning of Section 27A of the Securities Act of 1933, as amended, or the Securities Act, and Section 21E of the Securities Exchange Act of 1934, as amended, or the Exchange Act. All statements, other than statements of historical facts, included herein or incorporated herein by reference are “forward-looking statements.” Included among “forward-looking statements” are, among other things:

| • | statements relating to the construction or operation of each of our proposed LNG terminals or our proposed pipelines or liquefaction facilities, or expansions or extensions thereof, including statements concerning the completion or expansion thereof by certain dates or at all, the costs related thereto and certain characteristics, including amounts of regasification, transportation, liquefaction and storage capacity, the number of storage tanks, LNG trains, docks, pipeline deliverability and the number of pipeline interconnections, if any; |

| • | statements that we expect to receive an order from the Federal Energy Regulatory Commission, or FERC, authorizing us to construct and operate proposed LNG receiving terminals, liquefaction facilities or proposed pipelines by certain dates, or at all; |

| • | statements regarding future levels of domestic natural gas production, supply or consumption; future levels of LNG imports into North America; sales of natural gas in North America or other markets; exports of LNG from North America; and the transportation, other infrastructure or prices related to natural gas, LNG or other energy sources or hydrocarbon products; |

| • | statements regarding any financing or refinancing transactions or arrangements, or ability to enter into such transactions or arrangements, whether on the part of Cheniere Energy, Inc., or Cheniere, or any subsidiary or at the project level; |

| • | statements regarding any commercial arrangements presently contracted, optioned or marketed, or potential arrangements, to be performed substantially in the future, including any cash distributions and revenues anticipated to be received and the anticipated timing thereof, and statements regarding the amounts of total LNG regasification, liquefaction or storage capacity that are, or may become, subject to such commercial arrangements; |

| • | statements regarding counterparties to our commercial contracts, memoranda of understanding, or MOUs, construction contracts and other contracts; |

| • | statements regarding any business strategy, any business plans or any other plans, forecasts, projections or objectives, including potential revenues and capital expenditures, any or all of which are subject to change; |

ii

| • | statements regarding legislative, governmental, regulatory, administrative or other public body actions, requirements, permits, investigations, proceedings or decisions; |

| • | statements regarding our anticipated LNG and natural gas marketing activities; and |

| • | any other statements that relate to non-historical or future information. |

These forward-looking statements are often identified by the use of terms and phrases such as “achieve,” “anticipate,” “believe,” “contemplate,” “develop,” “estimate,” “expect,” “forecast,” “plan,” “potential,” “project,” “propose,” “strategy” and similar terms and phrases, or by the use of future tense. Although we believe that the expectations reflected in these forward-looking statements are reasonable, they do involve assumptions, risks and uncertainties, and these expectations may prove to be incorrect. You should not place undue reliance on these forward-looking statements, which are made as of the date of and speak only as of the date of this prospectus supplement.

Our actual results could differ materially from those anticipated in these forward-looking statements as a result of a variety of factors, including those discussed in “Risk Factors.” All forward-looking statements attributable to us or persons acting on our behalf are expressly qualified in their entirety by these risk factors.

We obtained the market and competitive position data used throughout this prospectus supplement, the accompanying prospectus and the documents incorporated herein by reference from our own research, surveys or studies conducted by third parties and industry or general publications. Industry publications and surveys generally state that they have obtained information from sources believed to be reliable, but do not guarantee the accuracy and completeness of such information. While we believe that each of these studies and publications is reliable, we have not, and the underwriter has not, independently verified such data, and we and the underwriter make no representation as to the accuracy of such information. Similarly, we believe that our internal research is reliable, but it has not been verified by any independent sources.

WHERE YOU CAN FIND MORE INFORMATION

We have filed a registration statement with the SEC under the Securities Act that registers the issuance and sale of the common stock offered by this prospectus supplement. The registration statement, including the exhibits attached thereto, contains additional relevant information about us. The rules and regulations of the SEC allow us to omit some information included in the registration statement from this prospectus supplement and the accompanying prospectus.

We file annual, quarterly, and other reports, proxy statements and other information with the SEC under the Exchange Act. You may read and copy any materials we file with the SEC at the SEC’s Public Reference Room at 100 F Street, N.E. Washington, D.C. 20549. Please call the SEC at 1-800-SEC-0330 for further information on the Public Reference Room. Our SEC filings are also available to the public through the SEC’s website at http://www.sec.gov.

General information about us, including our annual reports on Form 10-K, quarterly reports on Form 10-Q and current reports on Form 8-K, as well as any amendments and exhibits to those reports, are available free of charge through our website at http://www.cheniere.com as soon as reasonably practicable after we file them with, or furnish them to, the SEC. Information on our website is not incorporated into this prospectus supplement or the accompanying prospectus and is not a part of this prospectus supplement or the accompanying prospectus.

iii

The SEC allows us to “incorporate by reference” the information that we file with the SEC, which means that we can disclose information to you by referring to those documents. The information incorporated by reference is an important part of this prospectus supplement and the accompanying prospectus, and information that we file later with the SEC will automatically update and take the place of this information. We are incorporating by reference in this prospectus supplement the following documents filed with the SEC under the Exchange Act (other than any portions of the respective filings that were furnished pursuant to Item 2.02 or 7.01 of Current Reports on Form 8-K or other applicable SEC rules):

| • | Annual Report on Form 10-K for the year ended December 31, 2010; |

| • | Quarterly Report on Form 10-Q for the quarter ended March 31, 2011; |

| • | Current Reports on Form 8-K, as filed with the SEC on January 10, 2011, March 8, 2011(two) and May 20, 2011; and |

| • | the description of our common stock contained in our registration statement on Form 8-A, filed on March 2, 2001, including any amendments or reports filed for the purpose of updating the description. |

All documents that we file pursuant to Section 13(a), 13(c), 14 or 15(d) of the Exchange Act after the date of this prospectus supplement and until our offering hereunder is completed will be deemed to be incorporated by reference into this prospectus supplement and will be a part of this prospectus supplement from the date of the filing of the document. Any statement contained in a document incorporated or deemed to be incorporated by reference in this prospectus supplement will be deemed to be modified or superseded for purposes of this prospectus supplement to the extent that a statement contained in this prospectus supplement or any other subsequently filed documents that also is or is deemed to be incorporated by reference in this prospectus supplement modifies or supersedes that statement. Any statement that is modified or superseded will not constitute a part of this prospectus supplement, except as modified or superseded.

We will provide each person, including any beneficial owner to whom a prospectus is delivered, a copy of these filings, other than an exhibit to these filings, unless we have specifically incorporated that exhibit by reference into the filing, upon written or oral request and at no cost. Requests should be made by writing or telephoning us at the following address:

Cheniere Energy, Inc.

700 Milam Street, Suite 800

Houston, Texas 77002

(713) 375-5100

Attn: Investor Relations

iv

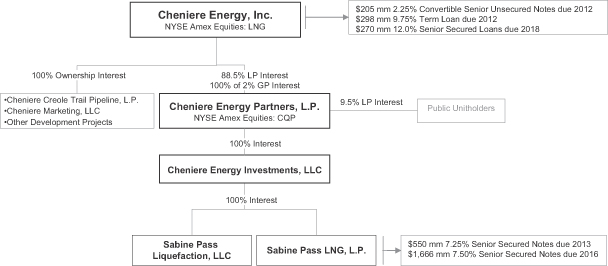

This summary, which highlights information contained elsewhere in this prospectus supplement, the accompanying prospectus and the documents incorporated herein by reference, is not complete and may not contain all of the information that you should consider before investing in shares of our common stock. You should read this entire prospectus supplement, the accompanying prospectus and the documents incorporated herein by reference. You should also consider, among other things, the information contained in “Risk Factors” in this prospectus supplement as well as the information contained in “Management’s Discussion and Analysis of Financial Condition and Results of Operations” and our consolidated financial statements and related notes thereto, each of which is incorporated by reference into this prospectus supplement. In this prospectus supplement, except as otherwise stated or required by the context, references to “Cheniere,” the “Company,” “we,” “us,” “our” and similar terms refer to Cheniere Energy, Inc. and its consolidated subsidiaries, collectively. References to “Cheniere Partners” refer to Cheniere Energy Partners, L.P. (NYSE Amex Equities: CQP), in which Cheniere has a 90.5% ownership interest.

Our Company

Cheniere is a Houston-based energy company primarily engaged in LNG-related businesses. We own and operate the Sabine Pass LNG terminal in Louisiana through our 90.5% ownership interest in and management agreements with Cheniere Partners, which is a publicly traded partnership that we created in 2007. We also own and operate the Creole Trail Pipeline, which interconnects the Sabine Pass LNG terminal with natural gas markets in North America. One of our subsidiaries, Cheniere Marketing, LLC, or Cheniere Marketing, is marketing LNG and natural gas on its own behalf and on behalf of Cheniere Partners, and is working to monetize LNG storage and regasification capacity reserved by Cheniere Partners at the Sabine Pass LNG terminal. Cheniere Partners is developing a liquefaction project to provide bi-directional LNG import and export service at the Sabine Pass LNG terminal. We are in various stages of developing other LNG terminal and pipeline related projects, each of which, among other things, will require acceptable commercial and financing arrangements before we make a final investment decision.

Our Business Strategy

In addition to safely maintaining the operations of the Sabine Pass LNG terminal and the Creole Trail Pipeline, our primary business strategies are to:

| • | monetize the 2.0 Bcf/d of regasification capacity at the Sabine Pass LNG terminal held by one of Cheniere Partners’ subsidiaries, Cheniere Energy Investments, LLC, which we refer to as Cheniere Investments, and monetize the 2.0 Bcf/d of natural gas transportation capacity on the Creole Trail Pipeline by: |

| – | entering into long-term commercial agreements for regasification or bi-directional service; |

| – | expanding operations to include bi-directional service capabilities; |

| – | developing a portfolio of long-term, short-term and spot LNG purchase and sale agreements; and |

| – | entering into business relationships for the marketing of natural gas that is processed at the Sabine Pass LNG terminal; and |

| • | restructure our finances and optimize our capital structure. |

In addition, our long-term strategy is to develop and construct additional LNG terminals and natural gas pipelines and related infrastructure when market and financial conditions are favorable.

S-1

Market Factors

Our ability to successfully execute our business strategies will be impacted by many factors, including: changes in worldwide supply and demand for natural gas and LNG; the relative prices for natural gas in North America and international markets; the willingness of LNG producers and international LNG buyers to invest new capital and secure access to North American natural gas markets on a long-term basis; and access to capital to market natural gas and LNG and to develop and construct liquefaction or other future LNG terminals, pipeline and other infrastructure projects.

We expect global demand for natural gas to grow significantly as more nations are seeking environmentally cleaner and more abundant and reliable fuel alternatives to oil and coal. In addition, global buyers of natural gas will need to source additional energy supplies to meet future economic growth and balance their energy portfolios. Most of the rapidly growing natural gas markets are in developing countries in Asia, particularly India and China, the Middle East and South America.

In recent years, North American domestic natural gas production has been on an upward trend, due in part to rapid growth in unconventional natural gas basins coupled with technological advances in horizontal drilling. As a result, natural gas reserves and production capacity in North America have increased significantly, exceeding expected North American natural gas demand as a result of a variety of factors, including improved energy efficiency and shifting economic activities to less energy-dependent activities. At the same time, however, natural gas prices in North America have generally trended downward since mid-2008 and many industry experts expect this trend to continue for a number of years.

In response to the shifting global and domestic natural gas market fundamentals, whereby demand for LNG regasification services and prices for natural gas in North America have decreased while prices for natural gas elsewhere in the world are generally higher, we are developing the Cheniere Partners liquefaction project to expand our operations at the Sabine Pass LNG terminal and Creole Trail Pipeline to provide bi-directional import and export services for new customers. We believe that the bi-directional service would offer customers an attractively priced option to access the North American market for natural gas supply or natural gas demand, as global fundamentals dictate. The new service would utilize the LNG storage capacity, ship berthing rights, regasification capacity, and pipeline transport capacity that we hold at the Sabine Pass LNG terminal and on the Creole Trail Pipeline through our subsidiaries. We are currently seeking regulatory authorization to construct and operate the expansion project, and we hope to enter into satisfactory long-term contracts with new customers for bi-directional services and to obtain sufficient financing so that we can begin construction of the liquefaction facilities as well as fund our business, including refinancing our existing indebtedness, until the bi-directional project is operational, which could occur as early as 2015.

Market factors have impacted the economic viability of importing natural gas for sale in the United States and could impact the success of implementing our strategy to develop liquefaction facilities. Limitations on our ability to generate additional cash flows from our existing assets or our future projects could have a material adverse impact on our business, results of operations, financial condition, liquidity and prospects. See “Risk Factors—Decreases in the demand for and price of natural gas could lead to reduced development of LNG projects worldwide, which could adversely affect the regasification component of our LNG businesses and the performance of our customers and could have a material adverse effect on our business, results of operations, financial condition, liquidity and prospects,” and “Risk Factors—We may not be successful in implementing our proposed business strategy to provide liquefaction services at the Sabine Pass LNG terminal,” as well as the other risk factors relating to our regasification services business and liquefaction project under the caption “Risk Factors” in this prospectus supplement.

S-2

Our Business

Our business activities are conducted by the following three operating segments:

| • | LNG terminal business; |

| • | Natural gas pipeline business; and |

| • | LNG and natural gas marketing business. |

LNG Terminal Business

We began developing our LNG terminal business in 1999 and were among the first companies to secure sites and commence development of new LNG terminals in North America. We focused our development efforts on three LNG terminal projects: Sabine Pass LNG in western Cameron Parish, Louisiana on the Sabine Pass Channel; Corpus Christi LNG near Corpus Christi, Texas; and Creole Trail LNG at the mouth of the Calcasieu Channel in central Cameron Parish, Louisiana. We constructed the Sabine Pass LNG terminal, which is owned through Cheniere Partners, in which we hold an approximate 90.5% interest. We currently own 100% interests in both the Corpus Christi and Creole Trail LNG terminal projects.

Liquefaction Project

In June 2010, Cheniere Partners initiated a project to add liquefaction services at the Sabine Pass LNG terminal that would transform the terminal into a bi-directional facility capable of liquefying domestic natural gas and exporting LNG in addition to importing and regasifying foreign-sourced LNG. As currently contemplated, the liquefaction project would be designed and permitted for up to four LNG trains, each with a nominal production capacity of approximately 4.0 million metric tons per annum, or mtpa. We anticipate LNG export from the Sabine Pass LNG terminal could commence as early as 2015, and may be constructed in phases, with each LNG train commencing operations as early as approximately six to nine months after the previous LNG train.

We intend for Sabine Pass Liquefaction, LLC, or Sabine Liquefaction, to enter into long-term, fixed-fee contracts for at least 3.5 mtpa (approximately 0.5 Bcf/d) of bi-directional LNG processing capacity per LNG train, for a fee of $1.75 per MMBtu. As of May 6, 2011, we had entered into and publicly announced memoranda of understanding, or MOUs, with potential customers for the proposed bi-directional facility representing a total of up to 9.8 mtpa of capacity. Each MOU is subject to negotiation and execution of definitive agreements and certain other customary conditions and does not represent a final and binding agreement with respect to its subject matter. Sabine Liquefaction is currently negotiating potential definitive agreements with these and other potential customers.

In August 2010, Sabine Liquefaction received approval from the Director of FERC’s Office of Energy Projects to begin the pre-filing process required to seek authorization to commence construction of the liquefaction project. In January 2011, the pre-filing period was completed and therefore Sabine Liquefaction submitted an application to the FERC requesting authorization to site, construct and operate liquefaction and export facilities at the Sabine Pass LNG terminal. In September 2010, the Department of Energy, or DOE, granted Sabine Liquefaction an order authorizing Sabine Liquefaction to export up to 16 mtpa (approximately 800 Bcf per year) of domestically produced LNG from the Sabine Pass LNG terminal to Free Trade Agreement, or FTA, countries for a 30-year term, beginning on the earlier of the date of first export or September 7, 2020. In May 2011, the DOE granted Sabine Liquefaction a second order authorizing Sabine Liquefaction to export up to the equivalent of 803 Bcf per year (approximately 16 mtpa) of domestically produced LNG from the Sabine Pass

S-3

LNG terminal to non-FTA countries for a 20-year term, beginning on the earlier of the date of first export or May 20, 2016.

Sabine Liquefaction has engaged Bechtel Corporation to complete front-end engineering and design work and to negotiate a lump-sum, turnkey contract based on an open book cost estimate. We currently estimate that total construction costs will be consistent with other recent liquefaction expansion projects constructed by Bechtel, or approximately $400 per metric ton, before financing costs. We have additional work to complete with Bechtel to be able to make an estimate specific to our site and project. Our cost estimates are subject to change due to factors such as changes in design, increased component and material costs, escalation of labor costs, cost overruns and increased spending to maintain a construction schedule.

Natural Gas Pipeline Business

We formed Cheniere Pipeline Company, a wholly owned subsidiary, to develop natural gas pipelines to provide access to North American natural gas markets for customers of our Sabine Pass and proposed Corpus Christi and Creole Trail LNG terminals. We are also developing other pipeline projects not primarily related to our LNG terminals. Our pipeline systems developed in conjunction with our LNG terminals will interconnect with multiple interstate pipelines, providing a means of transporting natural gas between trading points in the Gulf Coast and our LNG terminals. Our other projects are market-focused, seeking to connect natural gas supplies to growing markets. Our ultimate decisions regarding further development of new pipeline projects will depend upon future events, including, in particular, customer preferences and general market demand for pipeline transportation of natural gas from or to a particular LNG terminal.

LNG and Natural Gas Marketing Business

Our wholly owned subsidiary, Cheniere Marketing, is engaged in the LNG and natural gas marketing business and is seeking to monetize the 2.0 Bcf/d of regasification capacity at the Sabine Pass LNG terminal held by Cheniere Energy Investments, LLC, or Cheniere Investments, a wholly owned subsidiary of Cheniere Partners, through Cheniere Marketing’s variable capacity rights agreement with Cheniere Investments. Cheniere Marketing is seeking to develop a portfolio of long-term, short-term and spot LNG purchase and sale agreements; assist Cheniere Investments in negotiating with potential customers for bi-directional service at the Sabine Pass LNG terminal; and enter into business relationships for the domestic marketing of natural gas imported by Cheniere Marketing as LNG to the Sabine Pass LNG terminal.

In 2009, Cheniere Marketing began purchasing, transporting and unloading commercial LNG cargoes into the Sabine Pass LNG terminal and has used trading strategies intended to maximize margins on these cargoes. In addition, Cheniere Marketing has continued to enter into various business relationships to facilitate purchasing and selling commercial LNG cargoes.

Recent Developments

DOE Approval

In May 2011, the DOE granted Sabine Liquefaction an order authorizing Sabine Liquefaction to export LNG to countries with which the U.S. does not have an FTA. This order expands upon the authorization Sabine Liquefaction received in September 2010, which authorized the exports of natural gas as LNG to all current and future FTA countries. Under the order, Sabine Liquefaction received long-term, multi-contract authority to export on its own behalf, or as agent for others, up to the equivalent of 803 Bcf per year (approximately 16 mtpa) of domestically produced natural gas as LNG. The 20-year authorization commences the earlier of the first

S-4

export or May 2016, and is conditioned upon satisfactory completion of the FERC review process and upon Sabine Liquefaction commencing export operations by May 20, 2018.

Refinancing of Debt

We continue to work on restructuring our finances and improving our capital structure, including the refinancing of existing debt, with the earliest maturity date thereof being approximately $298.0 million of principal due in May 2012.

Company Information

We are incorporated under the laws of the state of Delaware. Our principal executive offices are located at 700 Milam Street, Suite 800, Houston, Texas 77002, and our telephone number at that address is (713) 375-5000. Our website address is www.cheniere.com. However, information contained on our website is not incorporated by reference into this prospectus supplement, and you should not consider the information contained on our website to be part of this prospectus supplement.

S-5

The Offering

| Issuer |

Cheniere Energy, Inc. |

| AMEX Symbol |

“LNG” |

| Common stock offered by us |

8,700,000 shares (or 10,000,000 shares if the underwriter’s over-allotment option is exercised in full) |

| Common stock to be outstanding after the offering |

78,855,504 shares (or 80,155,504 shares if the underwriter’s over-allotment option is exercised in full) |

| Use of proceeds |

We will use the net proceeds of approximately $ million from the offering ($ million if the underwriter’s over-allotment option is exercised in full), after deducting underwriting discounts and fees of approximately $ million in the aggregate but before paying estimated offering expenses of approximately $200,000, for general corporate purposes. |

| Risk Factors |

An investment in our common stock involves various risks, and prospective investors should carefully consider the matters discussed under “Risk Factors” beginning on page S-8 of this prospectus supplement. |

The number of shares of common stock outstanding before and after this offering is based on the number of shares outstanding as of May 25, 2011 and excludes:

| • | 782,593 shares of common stock reserved for issuance upon the exercise of outstanding stock options at a weighted average exercise price per share of $26.44; |

| • | 5,966,397 shares of common stock reserved for issuance upon the conversion of our outstanding convertible notes; and |

| • | 1,681,000 shares of common stock reserved for issuance upon the conversion of Series B Preferred Stock issuable upon exchange of certain outstanding debt. |

Unless we indicate otherwise, the number of shares of common stock shown to be outstanding after the offering in this prospectus supplement:

| • | assumes no exercise by the underwriter of its option to purchase up to 1,300,000 additional shares of our common stock to cover over-allotments; and |

| • | does not give effect to the use of proceeds of this offering. |

S-6

SUMMARY HISTORICAL CONSOLIDATED FINANCIAL DATA

The following summary historical consolidated financial information as of December 31, 2009 and 2010 and for each of the years ended December 31, 2008, 2009 and 2010 has been derived from Cheniere’s audited consolidated financial statements incorporated by reference into this prospectus supplement. The summary historical consolidated financial information as of December 31, 2008 has been derived from our audited financial statements not incorporated by reference into this prospectus supplement. The summary historical consolidated financial information as of March 31, 2011 and for the three months ended March 31, 2011 and 2010 has been derived from Cheniere’s unaudited consolidated financial statements incorporated by reference into this prospectus supplement. This information is only a summary and you should read it in conjunction with “Capitalization” in this prospectus supplement and “Management’s Discussion and Analysis of Financial Condition and Results of Operations,” which discusses factors affecting the comparability of the information presented, and our consolidated financial statements and related notes, each of which is incorporated herein by reference from our Annual Report on Form 10-K for the fiscal year ended December 31, 2010 and our Quarterly Report on Form 10-Q for the quarter ended March 31, 2011. Our historical results included below are not necessarily indicative of our future performance.

| For the Years Ended December 31, | For the Three Months Ended March 31, |

|||||||||||||||||||

| 2008 | 2009 | 2010 | 2010 | 2011 | ||||||||||||||||

| (In thousands, except per share data) | ||||||||||||||||||||

| (audited) | (unaudited) | |||||||||||||||||||

| Consolidated Statements of Operations Data: |

||||||||||||||||||||

| Revenues |

$ | 7,144 | $ | 181,126 | $ | 291,513 | $ | 79,517 | $ | 79,231 | ||||||||||

| LNG terminal and pipeline development expenses |

10,556 | 223 | 11,971 | 718 | 8,437 | |||||||||||||||

| LNG terminal and pipeline operating expenses |

14,522 | 36,857 | 42,415 | 12,813 | 10,194 | |||||||||||||||

| Depreciation, depletion and amortization |

24,346 | 54,229 | 63,251 | 15,624 | 15,386 | |||||||||||||||

| Oil and gas production and exploration costs |

526 | 471 | 627 | 99 | 138 | |||||||||||||||

| General and administrative expense |

122,678 | 65,830 | 68,626 | 19,217 | 21,510 | |||||||||||||||

| Restructuring charges(2) |

78,704 | 20 | — | — | — | |||||||||||||||

| Income (loss) from operations |

(244,188 | ) | 23,496 | 104,623 | 31,046 | 23,566 | ||||||||||||||

| Gain (loss) from equity method investments(3) |

(4,800 | ) | — | 128,330 | — | — | ||||||||||||||

| Gain (loss) from early extinguishment of debt(4) |

(10,691 | ) | 45,363 | (50,320 | ) | — | — | |||||||||||||

| Derivative gain |

4,652 | 5,277 | 461 | 505 | — | |||||||||||||||

| Interest expense, net |

(147,136 | ) | (243,295 | ) | (262,046 | ) | (67,194 | ) | (64,154 | ) | ||||||||||

| Interest income |

20,337 | 1,405 | 534 | 97 | 84 | |||||||||||||||

| Other income (expense) |

90 | 99 | 24 | (103 | ) | 25 | ||||||||||||||

| Non-controlling interest |

8,777 | 6,165 | 2,191 | 482 | 641 | |||||||||||||||

| Net loss |

$ | (372,959 | ) | $ | (161,490 | ) | $ | (76,203 | ) | $ | (35,167 | ) | $ | (39,838 | ) | |||||

| Net loss per share (basic and diluted) |

$ | (7.87 | ) | $ | (3.13 | ) | $ | (1.37 | ) | $ | (0.64 | ) | $ | (0.60 | ) | |||||

| Weighted average shares outstanding (basic and diluted) |

47,365 | 51,598 | 55,756 | 54,870 | 66,950 | |||||||||||||||

S-7

| As of December 31, | As of March 31, 2011 |

|||||||||||||||

| 2008 | 2009 | 2010 | ||||||||||||||

| (In thousands) | ||||||||||||||||

| (audited) | (unaudited) | |||||||||||||||

| Balance Sheet Data: |

||||||||||||||||

| Cash and cash equivalents |

$ | 102,192 | $ | 88,372 | $ | 74,161 | $ | 24,473 | ||||||||

| Current restricted cash and cash equivalents |

301,550 | 138,309 | 73,062 | 105,439 | ||||||||||||

| Working capital |

350,459 | 220,063 | 99,276 | 87,443 | ||||||||||||

| Non-current restricted cash and cash equivalents |

138,483 | 82,892 | 82,892 | 82,892 | ||||||||||||

| Total liabilities |

3,194,136 | 3,164,749 | 3,026,117 | 3,074,111 | ||||||||||||

| Total stockholders’ deficit |

(524,216 | ) | (649,732 | ) | (661,631 | ) | (693,520 | ) | ||||||||

| (1) | General and administrative expenses include $16.1 million, $19.2 million and $55.0 million of share-based compensation expense recognized in the years ended December 31, 2010, 2009 and 2008, respectively. |

| (2) | In the second quarter of 2008, we announced a cost savings program in connection with the downsizing of our natural gas marketing business activities, the nearing completion of significant construction activities for both the Sabine Pass LNG terminal and Creole Trail Pipeline and the seeking of alternative arrangements for our time charter interest in two LNG vessels. |

| (3) | In 2010, our investment in Freeport LNG Development, L.P. was sold, generating net cash proceeds of $104.3 million and a gain to Cheniere of $128.3 million. |

| (4) | Amount in 2010 relates to the cost to amend certain provisions of the term loan agreement that we entered into in August 2008 pursuant to which we obtained $250 million, which we refer to herein as the “2008 Loans.” Amount in 2009 relates to gains on the termination of $120.4 million of our Convertible Senior Unsecured Notes. Amount in 2008 relates to losses on the termination of a $95.0 million bridge loan in August 2008. |

S-8

The shares of common stock offered by this prospectus supplement may involve a high degree of risk. The following are some of the important factors that could affect our financial performance or could cause actual results to differ materially from estimates or expectations contained in our forward-looking statements. We may encounter risks in addition to those described below. Additional risks and uncertainties not currently known to us, or that we currently deem to be immaterial, may also impair or adversely affect our business, results of operation, financial condition, liquidity and prospects.

The risk factors in this prospectus supplement are grouped into the following categories:

| • | Risks Relating to Our Financial Matters; |

| • | Risks Relating to Our LNG Terminal Business; |

| • | Risks Relating to Our Natural Gas Pipeline Business; |

| • | Risks Relating to Our LNG and Natural Gas Marketing Business; |

| • | Risks Relating to Our LNG Businesses in General; |

| • | Risks Relating to Our Business in General; and |

| • | Risks Relating to Our Common Stock and This Offering |

Risks Relating to Our Financial Matters

Our existing level of cash resources, negative operating cash flow and significant debt could cause us to have inadequate liquidity and could materially and adversely affect our business, financial condition and prospects.

As of March 31, 2011, we had $24.5 million of cash and cash equivalents and $105.4 million of current restricted cash and cash equivalents, and we had $3.0 billion of total debt outstanding on a consolidated basis (before debt discounts). We incur significant depreciation and interest expense relating to the assets at the Sabine Pass LNG terminal, and we may incur significant additional debt and costs in connection with expansion of the Sabine Pass LNG terminal to provide bi-directional service. Our ability to generate positive cash flow and achieve profitability, so as to enhance our liquidity position in the future and be able to repay or refinance our debt, is subject to these and other risks, including those discussed in these Risk Factors.

We have a significant amount of debt which we may be unable to repay, refinance, or extend on commercially reasonable terms or at all, which could materially and adversely affect our business, financial condition and prospects.

As of March 31, 2011, we had $3.0 billion of total consolidated indebtedness (before debt discounts). We do not currently have financial resources, and may not be able to access external financial resources, sufficient to enable us to repay our earliest maturing debt or our subsequently maturing debt. If we are unable to refinance, extend or otherwise satisfy our earliest maturing debt, we may seek to reorganize under the protection of available reorganization statutes and may make such a determination at a time prior to our earliest debt maturity date.

Even if we are able to repay, refinance or extend our debt, the terms required may adversely affect us.

In order to obtain many types of financing, we may have to accept terms that are disadvantageous to us or that may have an adverse impact on our current or future business, operations or financial condition. For example:

| • | borrowings, debt issuances, or extensions of debt maturities may subject us to certain restrictive covenants, including covenants restricting our ability to raise additional capital or cross-defaults to our other indebtedness; |

S-9

| • | borrowings or debt issuances at the project level may subject the project entity to restrictive covenants, including covenants restricting its ability to make distributions to us or limiting our ability to sell our interests in such entity; and |

| • | additional sales of interests in our projects would reduce our interest in future revenues. |

Our substantial indebtedness and restrictions contained in existing or future debt agreements could adversely affect our ability to operate our business and pursue our liquefaction project, and could prevent us from satisfying or refinancing our debt obligations.

Our substantial indebtedness and restrictions contained in existing or future debt agreements could have important adverse consequences, including:

| • | limiting our ability to attract customers; |

| • | limiting our ability to compete with other companies that are not as highly leveraged; |

| • | limiting our flexibility in and ability to plan for or react to changing market conditions in our industry and to economic downturns, and making us more vulnerable than our less leveraged competitors to an industry or economic downturn; |

| • | limiting our ability to use operating cash flow in other areas of our business because we must dedicate a substantial portion of these funds to service debt, including indebtedness that we may incur in the future; |

| • | limiting our ability to obtain additional financing to fund the expansion of the Sabine Pass LNG terminal to provide bi-directional service, our capital expenditures, working capital, acquisitions, debt service requirements or liquidity needs for general business or other purposes; and |

| • | resulting in a material adverse effect on our business, results of operations and financial condition if we are unable to service or refinance our indebtedness or obtain additional financing, as needed. |

Our substantial indebtedness and the restrictive covenants contained in our existing or future debt agreements may not allow us the flexibility that we need to operate our business in an effective and efficient manner and may prevent us from taking advantage of strategic and financial opportunities that would benefit our business, such as Cheniere Partners’ liquefaction project. If we fail to comply with the restrictions contained in the agreements governing our existing indebtedness or any subsequent financing agreements, a default may allow our creditors, if the agreements so provide, to accelerate the related indebtedness as well as any other indebtedness to which cross-acceleration or cross-default provision applies.

If we are unsuccessful in operating our business or taking advantage of such opportunities, due to our substantial indebtedness or other factors, we may be unable to repay, refinance or extend our indebtedness on commercially reasonable terms or at all.

To service our indebtedness, we require significant amounts of cash flow from operations.

We require significant amounts of cash flow from operations in order to make annual interest payments of approximately $212 million on (i) $550.0 million of 7 1/4% Senior Secured Notes and $1,665.5 million of 7 1/2% of Senior Secured Notes of Sabine Pass LNG, which we refer to collectively as the Senior Notes, which are issued pursuant to the terms of a single indenture, which we refer to as the Sabine Pass Indenture, (ii) the $298.0 million outstanding under a credit agreement entered into by our wholly owned subsidiary, Cheniere Subsidiary Holding, LLC, which we refer to as the 2007 Term Loan, (iii) the $204.6 million outstanding as of March 31, 2011 of 2 1/4% Convertible Senior Unsecured Notes, which we refer to as the Convertible Senior Unsecured Notes and (iv) the $270.4 million outstanding under term loans obtained by us, which we refer to as the 2008 Loans. Our ability to make payments on and to refinance our indebtedness and to fund our capital expenditures will depend on our ability to generate cash in the future. Our business may not generate sufficient cash flow from operations, currently anticipated costs may increase, or future borrowings may not be available to us, which could cause us to be unable to pay or refinance our indebtedness or to fund our other liquidity needs.

S-10

Sabine Pass LNG may be restricted under the terms of the Sabine Pass Indenture from making distributions under certain circumstances, which may limit Cheniere Partners’ ability to pay or increase distributions to us, which could materially and adversely affect us.

The Sabine Pass Indenture restricts payments that Sabine Pass LNG can make to Cheniere Partners in certain events and limits the indebtedness that Sabine Pass LNG can incur. Sabine Pass LNG is permitted to pay distributions to Cheniere Partners only after the following payments have been made:

| • | an operating account has been funded with amounts sufficient to cover the succeeding 45 days of operating and maintenance expenses, maintenance capital expenditures and obligations, if any, under an assumption agreement and a state tax sharing agreement; |

| • | one-sixth of the amount of interest due on the Senior Notes on the next interest payment date (plus any shortfall from any such month subsequent to the preceding interest payment date) has been transferred to a debt payment account; |

| • | outstanding principal on the Senior Notes then due and payable has been paid; |

| • | taxes payable by Sabine Pass LNG or the guarantors of the Senior Notes and permitted payments in respect of taxes have been paid; and |

| • | the debt service reserve account has on deposit the amount required to make the next interest payment on the Senior Notes. |

In addition, Sabine Pass LNG will only be able to make distributions to Cheniere Partners in the event that it could, among other things, incur at least $1.00 of additional indebtedness under the fixed charge coverage ratio test of 2:1 at the time of payment and after giving pro forma effect to the distribution.

Sabine Pass LNG is also prohibited under the Sabine Pass Indenture from paying distributions to Cheniere Partners or incurring additional indebtedness upon the occurrence of any of the following events, among others:

| • | a default for 30 days in the payment of interest on, or additional interest, if any, with respect to, the Senior Notes; |

| • | a failure to pay any principal of, or premium, if any, on the Senior Notes; |

| • | a failure by Sabine Pass LNG to comply with various covenants in the Sabine Pass Indenture; |

| • | a failure to observe any other agreement in the Sabine Pass Indenture beyond any specified cure periods; |

| • | a default under any mortgage, indenture or instrument governing any indebtedness for borrowed money by Sabine Pass LNG in excess of $25.0 million if such default results from a failure to pay principal or interest on, or results in the acceleration of, such indebtedness; |

| • | a final money judgment or decree (not covered by insurance) in excess of $25.0 million is not discharged or stayed within 60 days following entry; |

| • | a failure of any material representation or warranty in the security documents entered into in connection with the indenture to be correct; |

| • | the Sabine Pass LNG terminal project is abandoned; or |

| • | certain events of bankruptcy or insolvency. |

Sabine Pass LNG’s inability to pay distributions to Cheniere Partners or to incur additional indebtedness as a result of the foregoing restrictions in the Sabine Pass Indenture may inhibit Cheniere Partners’ ability to pay or increase distributions to Cheniere Partners’ unitholders.

S-11

The fixed charge coverage ratio test contained in the Sabine Pass Indenture could prevent Sabine Pass LNG from making cash distributions. As a result, Cheniere Partners may be prevented from making distributions to us, which could materially and adversely affect us.

Sabine Pass LNG is not permitted to make cash distributions if its consolidated cash flow is not at least twice its fixed charges, calculated as required in the Sabine Pass Indenture. In order to satisfy this fixed charge coverage ratio test, we estimate that Sabine Pass LNG’s consolidated cash flow, as defined in the Sabine Pass Indenture, must be greater than approximately $375 million. Thus, TUA payments from Cheniere Investments are needed in addition to the TUA payments from Chevron U.S.A., Inc., or Chevron, and Total Gas and Power North America, Inc., or Total. Cheniere Investments has not commercialized its reserved regasification capacity or implemented its liquefaction project and may have difficulty making its TUA payments.

The fixed charge coverage ratio test contained in the Sabine Pass Indenture may not be met if Cheniere Investments’ payments to Sabine Pass LNG cease to be recognizable as revenue under U.S. generally accepted accounting principles, or GAAP. Even if Sabine Pass LNG receives the contracted payments under the Cheniere Investments TUA, the fixed charge coverage test will not be satisfied if those payments do not constitute revenues under GAAP, as then in effect. If the fixed charge coverage ratio test is not satisfied, Sabine Pass LNG will not be permitted by the Sabine Indenture to make distributions to Cheniere Partners, which may prevent Cheniere Partners from making distributions to us, which could have a material and adverse effect on our business, results of operations, financial condition and prospects.

Cheniere Partners’ ability to pay cash distributions on the common units we hold could be limited if Cheniere Marketing fails to make payments to Cheniere Investments under the Variable Capacity Rights Agreement, or VCRA, if Cheniere Investments fails to make payments to Sabine Pass LNG under its TUA, or if Sabine Pass LNG fails to make cash distributions.

Under the VCRA, Cheniere Marketing is required to pay for taxes and new regulatory costs incurred under the Cheniere Investments TUA. Cheniere Marketing is also required to use commercially reasonable efforts to commercialize Cheniere Investments’ TUA to the extent that neither Cheniere Marketing nor Cheniere Investments is obligated to the contrary under other agreements. Cheniere Marketing is further obligated to make payments to Cheniere Partners up to a maximum of $1.6 million per year to the extent that Cheniere Partners has a shortfall between its available cash and its initial quarterly distributions to its common unitholders.

In addition, even if Sabine Pass LNG received the contracted payments under the Cheniere Investments TUA, the fixed charge coverage test will not be satisfied if those payments do not constitute revenue under GAAP as then in effect and as provided in the Sabine Pass Indenture. Because the Cheniere Investments TUA is an agreement between related parties, payments under the Cheniere Investments TUA may not constitute revenues under GAAP as currently in effect if Cheniere Investments is determined to lack economic substance apart from Sabine Pass LNG. We believe Cheniere Investments could be determined to lack economic substance apart from Sabine Pass LNG if, for example, Cheniere Investments has no substantive business and is not pursuing, and has no prospect of developing, any substantive business apart from its TUA with Sabine Pass LNG.

If Cheniere Investments does not receive distributions from Sabine Pass LNG, Cheniere Partners may not be able to continue to make distributions to us, which could have a material and adverse effect on our business, results of operations, financial condition and prospects.

Our ability to generate needed amounts of cash is substantially dependent upon TUAs with two third-party Sabine Pass LNG customers, and we will be materially and adversely affected if either customer fails to perform its TUA obligations for any reason.

Our future results and liquidity are substantially dependent upon performance by Chevron and Total, each of which has entered into a TUA with Sabine Pass LNG and agreed to pay us approximately $125 million annually. We are dependent on each customer’s continued willingness and ability to perform its obligations under its TUA.

S-12

We are also exposed to the credit risk of the guarantors of these customers’ obligations under their respective TUAs in the event that we must seek recourse under a guaranty. If either customer fails to perform its obligations under its TUA, our business, results of operations, financial condition and prospects could be materially and adversely affected, even if we were ultimately successful in seeking damages from that customer or its guarantor for a breach of the TUA.

Each customer’s TUA for capacity at the Sabine Pass LNG terminal is subject to termination under certain circumstances.

Each of Sabine Pass LNG’s long-term TUAs contains various termination rights. For example, each customer may terminate its TUA if the Sabine Pass LNG terminal experiences a force majeure delay for longer than 18 months, fails to redeliver a specified amount of natural gas in accordance with the customer’s redelivery nominations or fails to accept and unload a specified number of the customer’s proposed LNG cargoes. We may not be able to replace these TUAs on desirable terms, or at all, if they are terminated.

Our ability to generate needed amounts of cash is also dependent upon our ability to commercially exploit the capacity at the Sabine Pass LNG terminal that we have reserved for our own account.

Our ability to achieve profitability in the future is significantly dependent upon our ability to commercially exploit the capacity that Cheniere Investments has reserved at the Sabine Pass LNG terminal. As discussed below under “—Risks Relating to Our LNG and Natural Gas Marketing Business,” Cheniere Investments may be unable to commercially exploit its capacity at the Sabine Pass LNG terminal. There are significant risks attendant to Cheniere Investments’ future ability to generate additional operating cash flow. Failure by Cheniere Investments to succeed in commercially exploiting its reserved capacity at the Sabine Pass LNG terminal could materially and adversely affect our business, results of operations, financial condition and prospects.

In order to generate needed amounts of cash, we may sell equity or equity-related securities or assets, including equity interests in Cheniere Partners. Such sales could dilute our stockholders’ proportionate indirect interests in the assets, business operations and proposed liquefaction and other projects of Cheniere Partners or other subsidiaries, and could adversely affect the market price of our common stock.

We have pursued and are pursuing a number of alternatives in order to generate needed amounts of cash, including potential issuances and sales of additional equity or equity-related securities by us, Cheniere Partners, or both, and potential sales of assets, including units of limited partner interest we currently hold in Cheniere Partners. Such sales, in one or more transactions, could dilute our stockholders’ proportionate indirect interests in the assets. business operations and proposed projects of Cheniere Partners, including its proposed liquefaction project, or in other subsidiaries. In addition, such sales, or the anticipation of such sales, could adversely affect the market price of our common stock.

We have not been profitable historically, and we have not had positive operating cash flow. Our ability to achieve profitability and generate positive operating cash flow in the future is subject to significant uncertainty.

We had net losses of $76.2 million, $161.5 million and $373.0 million (as adjusted), for the years ended December 31, 2010, 2009 and 2008, respectively. In addition, our net cash flow used in operating activities was $16.9 million, $97.9 million and $142.1 million for the years ended December 31, 2010, 2009 and 2008, respectively. In the future, we may incur operating losses and experience negative operating cash flow. We may not be able to reduce costs, increase revenues, or reduce our debt service obligations sufficiently to maintain our cash resources, which could cause us to have inadequate liquidity to continue our business.

S-13

Risks Relating to Our LNG Terminal Business

Operation of the Sabine Pass LNG terminal, and other LNG terminals that we may construct, involves significant risks.

As more fully discussed in these Risk Factors, the Sabine Pass LNG terminal faces operational risks, including the following:

| • | performing below expected levels of efficiency; |

| • | breakdown or failures of equipment or systems; |

| • | operational errors by vessel or tug operators or others; |

| • | operational errors by us or any contracted facility operator or others; |

| • | labor disputes; and |

| • | weather-related interruptions of operations. |

To maintain the cryogenic readiness of the Sabine Pass LNG terminal, Sabine Pass LNG may need to purchase and process LNG. Sabine Pass LNG’s third-party customers have the obligation to procure LNG if necessary for the Sabine Pass LNG terminal to maintain its cryogenic state. If they fail to do so, Sabine Pass LNG may need to procure such LNG.

Sabine Pass LNG needs to maintain the cryogenic readiness of the Sabine Pass LNG terminal. Together with Sabine Pass LNG, the two third-party customers have the obligation to maintain minimum inventory levels, and under certain circumstances, to procure LNG to maintain the cryogenic readiness of the terminal. In the event that aggregate minimum inventory levels are not maintained, Sabine Pass LNG has the right to procure a cryogenic readiness cargo, and to the extent that the third-party customers have failed to maintain their minimum inventory levels, be reimbursed by each customer for their allocable share of the LNG acquisition costs. If Sabine Pass LNG is not able to obtain financing on acceptable terms, it will need to maintain sufficient working capital for such a purchase until it receives reimbursement for the allocable costs of the LNG from its third-party customers or sells the regasified LNG. Sabine Pass LNG may also bear commodity price and other risks of purchasing LNG, holding it in its inventory for a period of time and selling the regasified LNG.

Sabine Pass LNG may be required to purchase natural gas to provide fuel at the Sabine Pass LNG terminal, which would increase operating costs and could have a material adverse effect on our results of operations.

Sabine Pass LNG’s TUAs provide for an in-kind deduction of 2% of the LNG delivered to the Sabine Pass LNG terminal, which it uses primarily as fuel for revaporization and self-generated power and to cover natural gas unavoidably lost at the facility. There is a risk that this 2% in-kind deduction will be insufficient for these needs and that Sabine Pass LNG will have to purchase additional natural gas from third parties. Sabine Pass LNG will bear the cost and risk of changing prices for any such fuel.

Hurricanes or other disasters could adversely affect us.

In August and September of 2005, Hurricanes Katrina and Rita damaged coastal and inland areas located in Texas, Louisiana, Mississippi and Alabama. Construction at the Sabine Pass LNG terminal site was temporarily suspended in connection with Hurricane Katrina, as a precautionary measure. Approximately three weeks after the occurrence of Hurricane Katrina, the Sabine Pass LNG terminal site was again secured and evacuated in anticipation of Hurricane Rita, the eye of which made landfall to the east of the site. As a result of these 2005 storms and related matters, the Sabine Pass LNG terminal experienced construction delays and increased costs. In September 2008, Hurricane Ike struck the Texas and Louisiana coast, and we experienced damage at the Sabine Pass LNG terminal.

S-14

Future storms and related storm activity and collateral effects, or other disasters such as explosions, fires, floods or accidents, could result in damage to, or interruption of operations at, the Sabine Pass LNG terminal or related infrastructure, as well as delays or cost increases in the construction of Cheniere Partners’ proposed liquefaction facilities or our other LNG terminals. If there are changes in the global climate, storm frequency and intensity may increase; should it result in rising seas, our coastal operations would be impacted.

Failure to obtain and maintain approvals and permits from governmental and regulatory agencies with respect to the development, construction and operation of our LNG terminals could impede operations and construction and could have a material adverse effect on us.

The design, construction and operation of LNG terminals is a highly regulated activity. The FERC’s approval under Section 3 of the Natural Gas Act of 1938, which we refer to as the NGA, as well as several other material governmental and regulatory approvals and permits, are required in order to construct and operate an LNG terminal. Although Sabine Pass LNG has obtained all of the necessary authorizations to operate the Sabine Pass LNG terminal, such authorizations are subject to ongoing conditions imposed by regulatory agencies, and additional approval and permit requirements may be imposed.

Cheniere Partners and its subsidiaries will require governmental approvals and authorizations to implement the proposed business strategy to construct and operate a liquefaction and LNG export facility at the Sabine Pass LNG terminal site. In particular, Cheniere Partners and its subsidiaries will need authorization from the FERC to construct and operate the proposed liquefaction facilities.

There is no assurance that Cheniere Partners and its subsidiaries will obtain and maintain these governmental permits, approvals and authorizations, and failure to obtain and maintain any of these permits, approvals or authorizations could have a material adverse effect on our business, results of operations, financial condition and prospects.

We may not be able to enter into satisfactory commercial arrangements with third-party customers for services at the Sabine Pass LNG terminal or at our other proposed LNG terminals. We may change our business strategy regarding how and when we market LNG terminal capacity.

We have historically entered into long-term TUAs for a portion of the regasification capacity at our proposed LNG terminals, which include fixed-fee capacity reservation fees. The portion of our total regasification capacity that we plan to commit under such long-term TUAs has changed in the past and may change in the future for various reasons, including responding to market factors or perceived opportunities that we believe may be available to us.

Our ability to obtain financing for Cheniere Partners’ proposed liquefaction facilities or our other LNG facilities is expected to be contingent upon, among other things, our ability to enter into sufficient long-term commercial agreements in advance of the commencement of construction. To date, we have not entered into any definitive third-party agreements for Cheniere Partners’ proposed liquefaction facilities or either of our proposed LNG terminals, and we may not be successful in negotiating such agreements.

We may also change our business strategy due to our inability to enter into agreements with customers or based on our views regarding future prices, demand and supply of LNG, natural gas, liquefaction capacity and regasification capacity. If our efforts to market LNG terminal and related pipeline capacity are not successful, our business, results of operations, financial condition and prospects could be materially and adversely affected.

S-15

The construction of Cheniere Partners’ expansion project to add liquefaction capacity at the Sabine Pass LNG terminal will be subject to a number of development risks, which could cause cost overruns and delays or prevent completion of the project.

Key factors that may affect the timing of, and our ability to complete, the expansion project at the Sabine Pass LNG terminal to add bi-directional service include, but are not limited to:

| • | the issuance and/or continued availability of necessary permits, licenses and approvals from the FERC and the DOE, other governmental agencies and third parties as are required to construct and operate the expansion project; |

| • | the availability of sufficient financing on reasonable terms; |

| • | our ability to obtain satisfactory long-term agreements with customers for bi-directional service and for these customers to perform under those agreements during the terms thereof and to maintain their creditworthiness; |

| • | our ability to enter into a satisfactory agreement with an engineering, procurement and construction contractor and other contractors and to maintain good relationships with these contractors in order to construct the liquefaction facilities, and the ability of those contractors to perform their obligations under the contracts and to maintain their creditworthiness; |

| • | unanticipated changes in domestic and international market demand for and supply of natural gas and LNG, which will depend, in part, on supplies of, and prices for, alternative energy sources and the discovery of new sources of natural resources; |

| • | competition with other domestic and international LNG terminals; |

| • | local and general economic conditions; |

| • | catastrophes, such as explosions, fires and product spills; |

| • | resistance in the local community to the expansion of the Sabine Pass LNG terminal; |

| • | labor disputes; and |

| • | weather conditions, such as hurricanes. |

Delays in the construction of the Sabine Pass LNG expansion project beyond the estimated development periods, as well as cost overruns, could increase the cost of completion beyond the amounts that we estimate, which could require us to obtain additional sources of financing to fund our operations until the expansion project is constructed (which could cause further delays). Any delay in completion of the expansion project may also cause a delay in the receipt of revenues projected from the expansion project or cause a loss of one or more customers in the event of significant delays. As a result, any significant construction delay, whatever the cause, could have a material adverse effect on our business, results of operations, financial condition and prospects.

We may not be successful in implementing our proposed business strategy to provide liquefaction services at the Sabine Pass LNG terminal.

A significant element of our strategy to monetize our reserved capacity at the Sabine Pass LNG terminal is to develop liquefaction facilities at the terminal, which is in the early stages of development. Our proposed addition of liquefaction facilities and services at the Sabine Pass LNG terminal will require very significant financial resources, which may not be available on terms reasonably acceptable to us or at all. Costs overruns or delays could adversely affect permitting or construction of the liquefaction facilities. We also may not be able to obtain customer commitments to use the liquefaction services, without which we would not be able to finance the construction of liquefaction facilities. It will take several years to construct the liquefaction facilities, and we do not expect them to be operational until at least 2015. Even if successfully constructed, the liquefaction facilities would be subject to many of the same operating risks described herein with respect to the Sabine Pass LNG

S-16

terminal. Accordingly, there are many risks associated with our proposed liquefaction facilities, and if we are not successful in implementing our business strategy, we may not be able to generate additional cash flows, which could have a material adverse impact on our business, results of operations, financial condition, liquidity and prospects.

The operation of the Sabine Pass LNG terminal and the liquefaction project are subject to significant operating hazards and uninsured risks, one or more of which may create significant liabilities and losses that could have a material and adverse effect on us.

The operation of the Sabine Pass LNG terminal and the liquefaction project are subject to the inherent risks associated with this type of operation, including explosions, pollution, release of toxic substances, fires, hurricanes and adverse weather conditions, and other hazards, each of which could result in significant delays in commencement or interruptions of operations and/or in damage to or destruction of the Sabine Pass LNG terminal site and assets or damage to persons and property. In addition, operations at the Sabine Pass LNG terminal site and the facilities and vessels of third parties on which our operations are dependent face possible risks associated with acts of aggression or terrorism.

We do not, nor do we intend to, maintain insurance against all of these risks and losses. We may not be able to maintain desired or required insurance in the future at rates that we consider reasonable. The occurrence of a significant event not fully insured or indemnified against could have a material adverse effect on our business, results of operations, financial condition, liquidity and prospects.

Existing and future environmental and similar laws and regulations could result in increased compliance costs or additional operating costs and restrictions.

Our business is and will be subject to extensive federal, state and local laws and regulations that control, among other things, discharges to air and water; the handling, storage and disposal of hazardous chemicals, hazardous waste, and petroleum products; and remediation associated with the release of hazardous substances. Many of these laws and regulations, such as the Clean Air Act, or CAA, the Oil Pollution Act, the Clean Water Act, or CWA, and the Resource Conservation and Recovery Act, or RCRA, and analogous state laws and regulations, restrict or prohibit the types, quantities and concentration of substances that can be released into the environment in connection with the construction and operations of the Sabine Pass LNG terminal and liquefaction facilities and require us to maintain permits and provide governmental authorities with access to our facilities for inspection and reports related to our compliance. Violation of these laws and regulations could lead to substantial fines and penalties or to capital expenditures related to pollution control equipment that could have a material adverse effect on our business, results of operations, financial condition, liquidity and prospects. Federal and state laws impose liability, without regard to fault or the lawfulness of the original conduct, for the release of certain types or quantities of hazardous substances into the environment. As the owner and operator of an LNG terminal or liquefaction facility, we could be liable for the costs of cleaning up hazardous substances released into the environment and for damage to natural resources.

There are numerous regulatory approaches currently in effect or being considered to address greenhouse gases, including possible future U.S. treaty commitments, new federal or state legislation that may impose a carbon emissions tax or establish a cap-and-trade program, and regulation by the U.S. Environmental Protection Agency, or EPA. For example, the adoption of frequently proposed legislation implementing a carbon tax on energy sources that emit carbon dioxide into the atmosphere may have a material adverse effect on the ability of our customers (i) to import LNG, if imposed on them as importers of potential emission sources, or (ii) to sell regasified LNG, if imposed on them or their customers as natural gas suppliers or consumers. In addition, as we consume retainage gas at the Sabine Pass LNG terminal this carbon tax may also be imposed on us directly.

S-17

Risks Relating to Our Natural Gas Pipeline Business

Our existing and proposed pipelines will be dependent upon a few potential customers, and our pipeline business could be materially and adversely affected if we lost any one of those customers.

We do not currently have any third-party, firm transportation customers for our existing or proposed pipelines. Failure to obtain any third-party, firm transportation customers could have a material adverse impact on our business.

Our natural gas pipelines, including their FERC gas tariffs, are subject to FERC regulation.

Our FERC tariffs contain pro forma transportation agreements, which must be filed and approved by the FERC. Before we enter into a transportation agreement with a shipper that contains a term that materially deviates from our tariff, we must seek FERC approval. The FERC may approve the material deviation in the transportation agreement; however, in that case, the materially deviating terms must be made available to our other similarly-situated customers. If we fail to seek FERC approval of a transportation agreement that materially deviates from our tariff, or if the FERC audits our contracts and finds deviations that appear to be unduly discriminatory, the FERC could conduct a formal enforcement investigation, resulting in serious penalties and/or onerous ongoing compliance obligations.

Should we fail to comply with all applicable FERC-administered statutes, rules, regulations and orders, we could be subject to substantial penalties and fines. Under the Energy Policy Act of 2005, or EPAct, the FERC has civil penalty authority under the NGA to impose penalties for current violations of up to $1.0 million per day for each violation.

The FERC could change its current ratemaking policies, and those changes could have adverse effects on our proposed pipelines.

Pipeline safety integrity programs and repairs may impose significant costs and liabilities on us.

The Federal Office of Pipeline Safety has issued a final rule requiring pipeline operators to develop integrity management programs to comprehensively evaluate certain areas along their pipelines and to take additional measures to protect pipeline segments located in what the rule refers to as “high consequence areas” where a leak or rupture could potentially do the most harm. The final rule requires operators to:

| • | perform ongoing assessments of pipeline integrity; |

| • | identify and characterize applicable threats to pipeline segments that could impact a high consequence area; |

| • | improve data collection, integration and analysis; |

| • | repair and remediate the pipeline as necessary; and |

| • | implement preventive and mitigating actions. |

We are required to maintain pipeline integrity testing programs that are intended to assess pipeline integrity. The rule, or an increase in public expectations for pipeline safety, may require additional reporting and more frequent inspection or testing of our pipeline facilities. Any repair, remediation, preventative or mitigating actions may require significant capital and operating expenditures. Should we fail to comply with the Office of Pipeline Safety’s rules and related regulations and orders, we could be subject to penalties and fines.

Any reduction in the capacity of, or the allocations to, interconnecting, third-party pipelines could cause a reduction of volumes transported in our pipelines, which would adversely affect our revenues and cash flow.

We will be dependent upon third-party pipelines and other facilities to provide delivery options to and from our pipelines. If any pipeline connection were to become unavailable for volumes of natural gas due to repairs, damage to

S-18

the facility, lack of capacity or any other reason, our ability to continue shipping natural gas to end markets could be restricted, thereby reducing our revenues. Any permanent interruption at any key pipeline interconnect which caused a material reduction in volumes transported on our pipelines could have a material adverse effect on our business, results of operations and financial condition.

Failure to obtain and maintain approvals and permits from governmental and regulatory agencies with respect to the development and operation of our natural gas pipelines would have a detrimental effect on us and our pipeline projects.