Exhibit

99.1

1

Credit Suisse Energy Summit February 2008 CHENIERE ENERGY, INC. (Gp:) *Corpus

Christi LNG, LLC Cheniere Energy, Inc. 100% *Artist’s Rendition (Gp:)

*Creole Trail LNG, L.P. Cheniere Energy, Inc. 100% *Freeport LNG

Development, L.P. Cheniere Energy, Inc. 30% * Sabine Pass LNG,

L.P. Cheniere Energy Partners, L.P. Cheniere Energy, Inc.

91%

2

This presentation contains certain statements that are, or may be deemed

to be,

“forward-looking statements” within the meaning of Section 27A of the Securities

Act and Section 21E of the Securities Exchange Act of 1934, as amended, or

the

Exchange Act. All statements, other than statements of historical

facts, included herein are “forward-looking statements.” Included

among “forward-looking statements” are, among other things: statements that we

expect to commence or complete construction of each or any of our proposed

liquefied natural gas, or LNG, receiving terminals by certain dates,

or at all; statements that we expect to receive authorization from the Federal

Energy Regulatory Commission, or FERC, to construct and operate proposed

LNG

receiving terminals by a certain date, or at all; statements regarding future

levels of domestic natural gas production and consumption, or the future

level

of LNG imports into North America, or regarding projected future capacity

of

liquefaction or regasification, liquifaction utilization or total monthly

LNG

trade facilities worldwide, regardless of the source of such information;

statements regarding any financing transactions or arrangements, whether

on the

part of Cheniere or at the project level; statements relating to the

construction of our proposed LNG receiving terminals, including statements

concerning estimated costs, and the engagement of any contractor; statements

regarding any Terminal Use Agreement, or TUA, or other commercial arrangements

presently contracted, optioned, marketed or potential arrangements to be

performed substantially in the future, including any cash distributions and

revenues anticipated to be received; statements regarding the commercial

terms

and potential revenues from activities described in this presentation;

statements regarding the commercial terms or potential revenue from any

arrangements which may arise from the marketing of uncommitted capacity from

any

of the terminals, including the Creole Trail and Corpus Christi terminals

which

do not currently have contractual commitments; statements regarding the

commercial terms or potential revenue from any arrangement relating to the

proposed contracting for excess or expansion capacity for the Sabine Pass

LNG

Terminal or the Indexed Purchase Agreement (“IPA”) or LNG spot purchase examples

described in this presentation; statements that our proposed LNG receiving

terminals, when completed, will have certain characteristics, including amounts

of regasification and storage capacities, a number of storage tanks and docks

and pipeline interconnections; statements regarding Cheniere and Cheniere

Marketing forecasts, and any potential revenues and capital expenditures

which

may be derived from any of Cheniere business groups; statements regarding

Cheniere Pipeline Company, and the capital expenditures and potential revenues

related to this business group; statements regarding our proposed LNG receiving

terminals’ access to existing pipelines, and their ability to obtain

transportation capacity on existing pipelines; statements

regarding the Cheniere Southern Trail Pipeline, and its potential

business opportunities; statements regarding possible expansions of the

currently projected size of any of our proposed LNG receiving terminals;

statements regarding the payment by Cheniere Energy Partners, L.P. of cash

distributions; statements regarding our business strategy, our business plan

or

any other plans, forecasts, examples, models, or objectives, any or all of

which

are subject to change; statements regarding estimated corporate

overhead expenses; and any other statements that relate to non-historical

information. These forward-looking statements are often identified by the

use of

terms and phrases such as “achieve,” “anticipate,” “believe,” “estimate,”

“example,” “expect,” “forecast,” “opportunities,” “plan,” “potential,”

“project,” “propose,” “subject to,” and similar terms and

phrases. Although we believe that the expectations reflected in these

forward-looking statements are reasonable, they do involve assumptions, risks

and uncertainties, and these expectations may prove to be

incorrect. You should not place undue reliance on these

forward-looking statements, which speak only as of the date of this

presentation. Our actual results could differ materially from those

anticipated in these forward-looking statements as a result of a variety

of

factors, including those discussed in “Risk Factors” in the Cheniere Energy,

Inc. Annual Report on Form 10-K for the year ended December 31, 2006, which

are

incorporated by reference into this presentation. All forward-looking

statements attributable to us or persons acting on our behalf are expressly

qualified in their entirety by these ”Risk Factors”. These

forward-looking statements are made as of the date of this presentation,

and we

undertake no obligation to publicly update or revise any forward-looking

statements. Safe Harbor Act

3

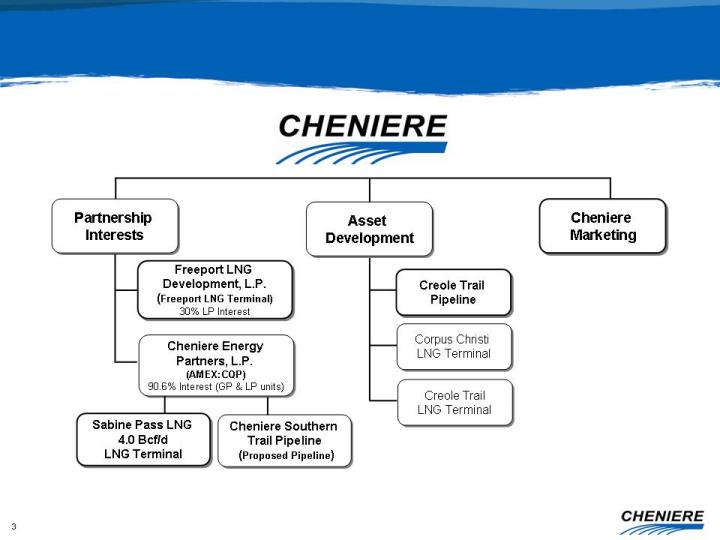

Cheniere Marketing Asset Development Partnership Interests Sabine Pass

LNG 4.0 Bcf/d LNG Terminal Cheniere Energy Partners,

L.P. (AMEX:CQP) 90.6% Interest (GP & LP units) Creole Trail LNG

Terminal Creole Trail Pipeline Corpus Christi LNG Terminal

Freeport LNG Development, L.P. (Freeport LNG Terminal) 30% LP Interest Cheniere

Southern Trail Pipeline (Proposed Pipeline)

4

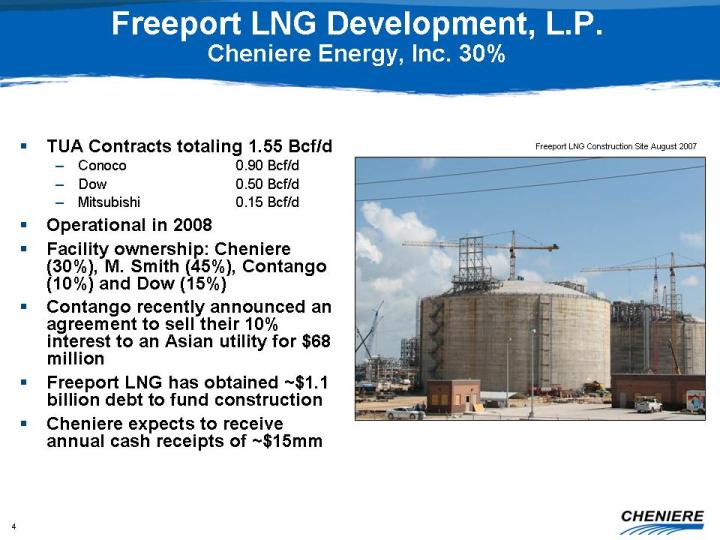

Freeport LNG Development, L.P. Cheniere Energy, Inc. 30% Freeport LNG

Construction Site August 2007 TUA Contracts totaling 1.55 Bcf/d Conoco 0.90

Bcf/d Dow 0.50 Bcf/d Mitsubishi 0.15 Bcf/d Operational in 2008 Facility

ownership: Cheniere (30%), M. Smith (45%), Contango (10%) and Dow

(15%) Contango recently announced an agreement to sell their 10%

interest to an Asian utility for $68 million Freeport LNG has obtained $1.1

billion debt to fund construction Cheniere expects to receive annual cash

receipts of $15mm

5

Cheniere Energy Partners, L.P. (AMEX: CQP) Sabine Pass LNG,

L.P. Cheniere Energy, Inc. 90.6% Sabine Pass Construction Site –

January 2008 4 Bcf/d capacity contracted at Sabine Pass facility resulting

in

annual revenues of approximately: $256 MM from CVX and Total ~$256 MM from

Marketing Operating costs, debt service and common unit holder distributions

are

estimated to be $245 MM to $255 MM* Annual distribution is $1.70 per unit

and

will be paid to all unit holders beginning mid 2009** Estimated construction

costs are $1.5 B * Estimate for 2010 full year basis **

Currently CQP is paying $1.70 per unit to common unit

holders. Distributions to GP and subordinated

units expected to reach $1.70 per unit by 2H09.

6

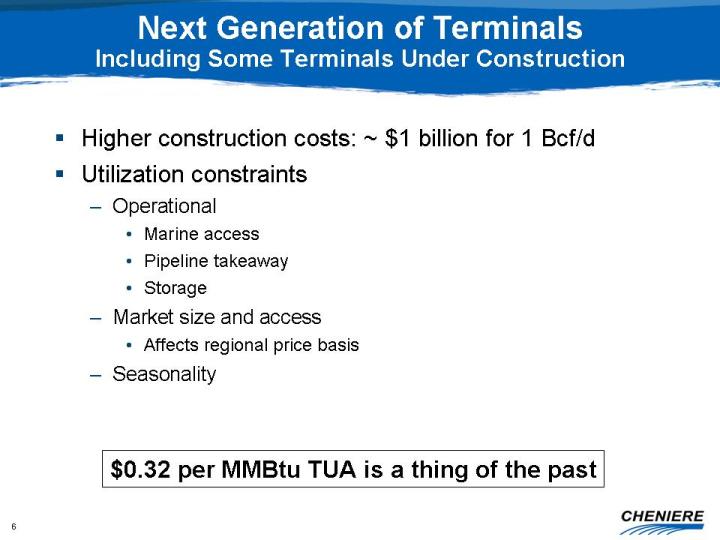

Next Generation of Terminals Including Some Terminals Under Construction

Higher

construction costs: $1 billion for 1 Bcf/d Utilization constraints Operational

Marine access Pipeline takeaway Storage Market size and access Affects regional

price basis Seasonality $0.32 per MMBtu TUA is a thing of the

past

7

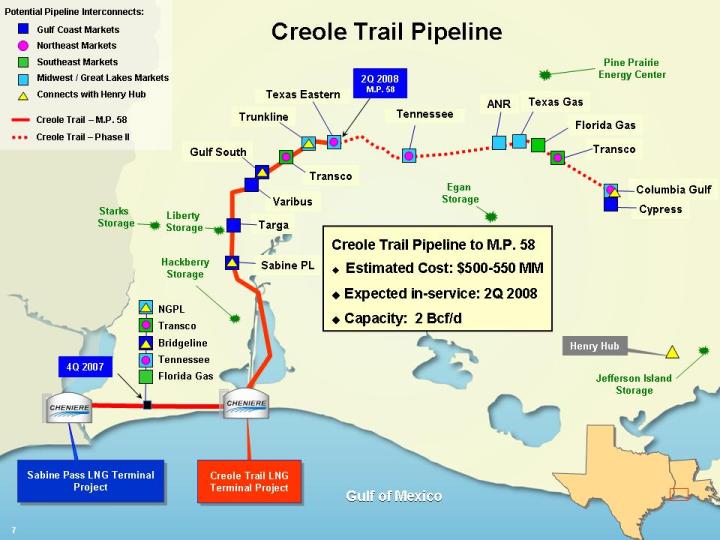

Sabine PL Targa Transco Gulf South Trunkline Jefferson Island Storage Sabine

Pass LNG Terminal Project Creole Trail LNG Terminal Project Henry Hub Varibus

NGPL Transco Bridgeline Tennessee Florida Gas Creole Trail Pipeline Liberty

Storage

Starks Storage Hackberry Storage Texas Eastern Gulf Coast

Markets Northeast Markets Southeast Markets Midwest / Great Lakes Markets

Connects with Henry Hub Gulf of Mexico 4Q 2007 ANR Texas Gas Transco Florida

Gas

Columbia Gulf Cypress Egan Storage Pine Prairie Energy Center

Tennessee 2Q 2008 M.P. 58 Creole Trail – M.P. 58 Creole Trail – Phase II 7

Potential Pipeline Interconnects: Creole Trail Pipeline to M.P. 58 Estimated

Cost: $500-550 MM Expected in-service: 2Q 2008 Capacity: 2

Bcf/d

8

Fuel Efficiency Projects Projects include installation of waste heat recovery

units and ambient air vaporizers Waste heat recovery utilizes waste heat

from

gas turbine generator exhaust to heat water for use in the submerged combustion

vaporizers Ambient air vaporizers reheat LNG without using fuel Proposed

projects would result in fuel savings, which would allow for partial

monetization of the 2% LNG retained Savings depends on LNG throughput at

the

terminal Savings will also depend on number of ambient air vaporizers that

can

be effectively installed Estimated to save potentially 50-75% of the 2% LNG

retainage Estimated project completions Waste heat recovery: 2010

Ambient air vaporizers: 2010-2011

9

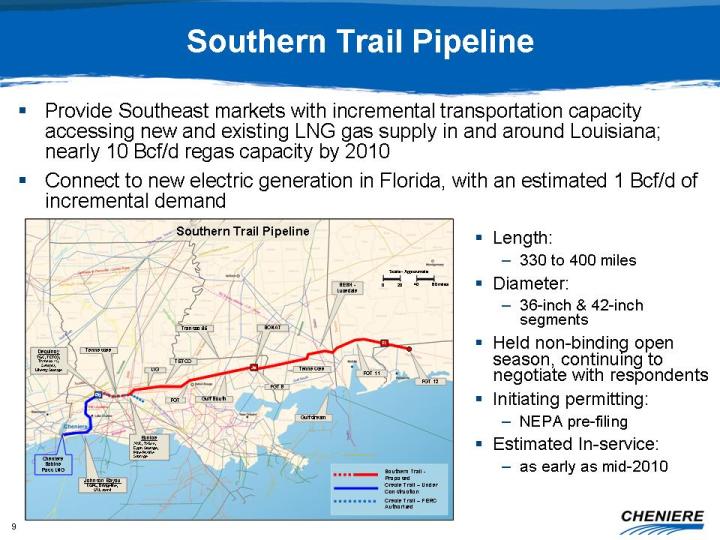

Length: 330 to 400 miles Diameter: 36-inch & 42-inch

segments Held non-binding open season, continuing to negotiate with respondents

Initiating permitting: NEPA pre-filing Estimated In-service: as early

as mid-2010 Southern Trail Pipeline Provide Southeast markets with incremental

transportation capacity accessing new and existing LNG gas supply in and

around

Louisiana; nearly 10 Bcf/d regas capacity by 2010 Connect to new

electric generation in Florida, with an estimated 1 Bcf/d of incremental

demand

10

LNG Fundamentals Value of Marketing

11

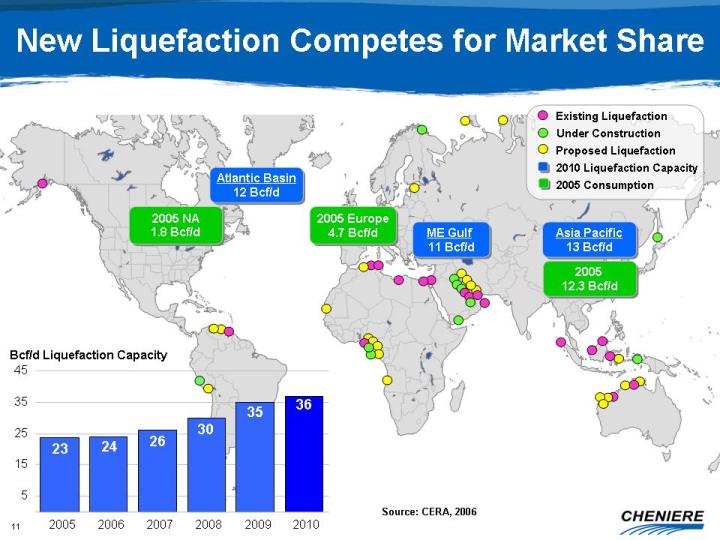

New Liquefaction Competes for Market Share Source: CERA, 2006 Atlantic Basin

12

Bcf/d ME Gulf 11 Bcf/d Asia Pacific 13 Bcf/d 2005 Europe 4.7 Bcf/d

2005 12.3 Bcf/d 2005 NA 1.8 Bcf/d (Gp:) 2010 Liquefaction Capacity

(Gp:) 2005 Consumption 5 15 25 35 45 36 23 24 26 30 35 Bcf/d Liquefaction

Capacity Existing Liquefaction Under Construction Proposed Liquefaction 2005

2006 2007 2008 2009 2010

12

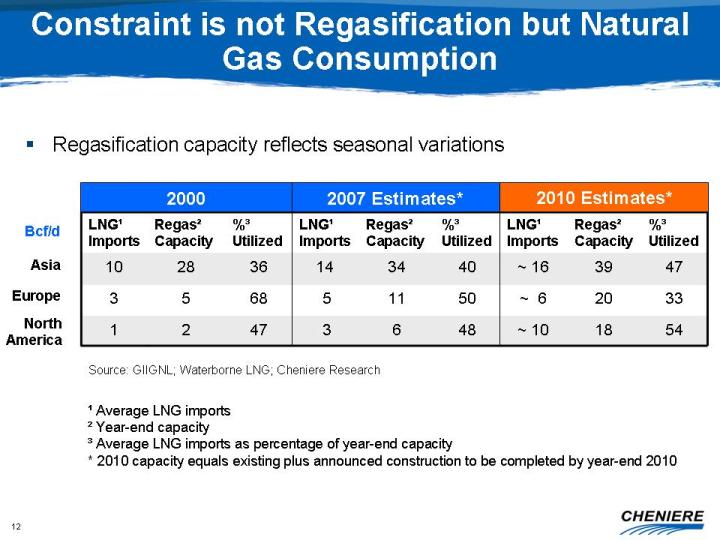

Constraint is not Regasification but Natural Gas Consumption Source: GIIGNL;

Waterborne LNG; Cheniere Research Regasification capacity reflects

seasonal variations Bcf/d Asia Europe North America ¹ Average LNG imports ²

Year-end capacity ³ Average LNG imports as percentage of year-end capacity *

2010 capacity equals existing plus announced construction to be completed

by

year-end 2010

13

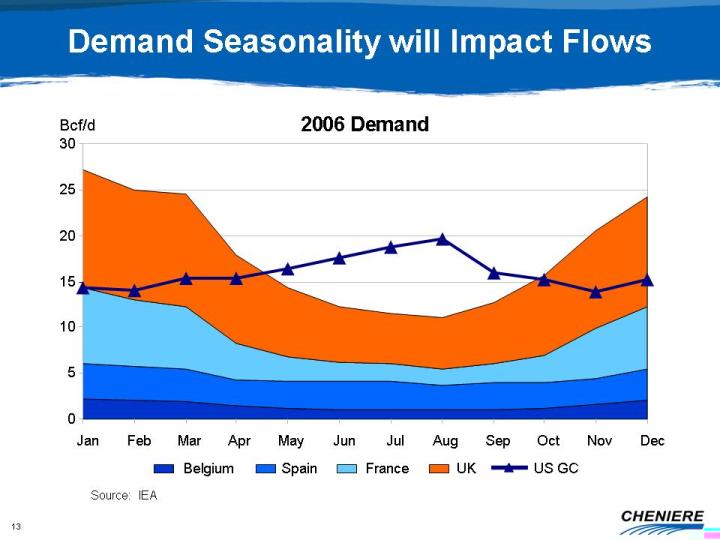

Demand Seasonality will Impact Flows Source: IEA 2006 Demand 0 5 10 15 20

25 30 Jan Feb Mar Apr May Jun Jul Aug Sep Oct Nov Dec Belgium Spain France

UK US

GC Bcf/d

14

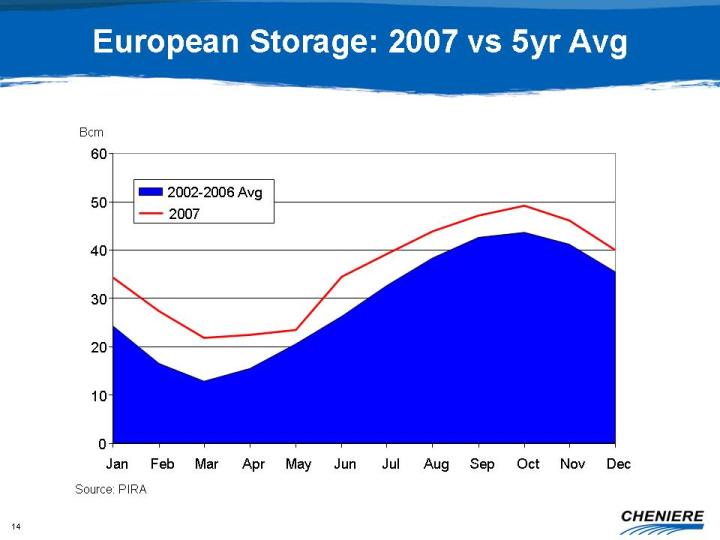

European Storage: 2007 vs 5yr Avg Source: PIRA 0 10 20 30 40 50 60

Jan Feb Mar Apr May Jun Jul Aug Sep Oct Nov Dec Bcm 2002-2006 Avg

2007

15

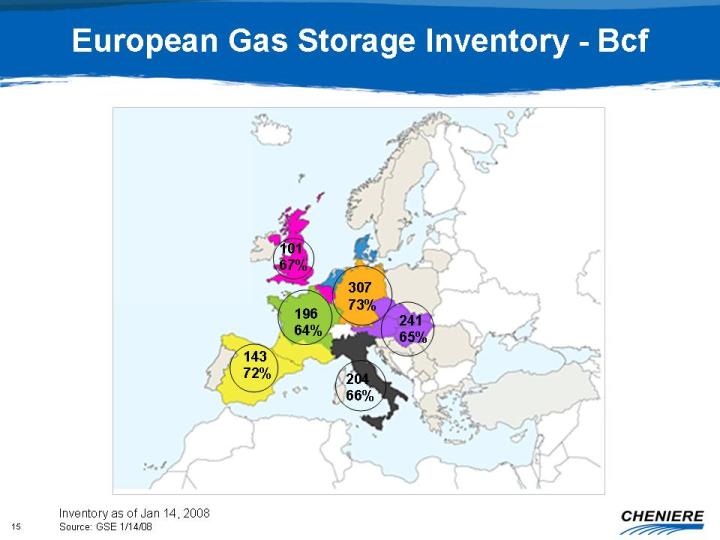

307 73% 143 72% 196 64% 101 67% 204 66% 241 65% European Gas Storage Inventory

-

Bcf Inventory as of Jan 14, 2008 Source: GSE 1/14/08

16

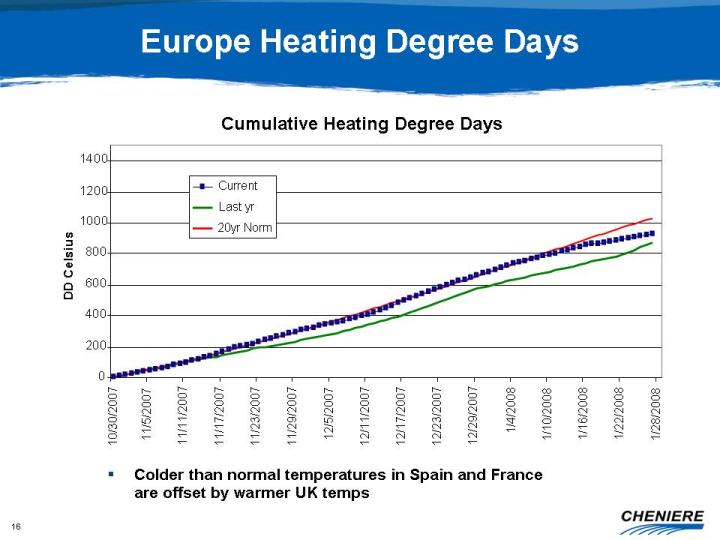

Europe Heating Degree Days Colder than normal temperatures in Spain and France

are offset by warmer UK temps Cumulative Heating Degree Days 0 200 400 600

800

1000 1200 1400 10/30/2007 11/5/2007 11/11/2007 11/17/2007 11/23/2007 11/29/2007

12/5/2007 12/11/2007 12/17/2007 12/23/2007 12/29/2007 1/4/2008 1/10/2008

1/16/2008 1/22/2008 1/28/2008 DD Celsius Current Last yr 20yr

Norm

17

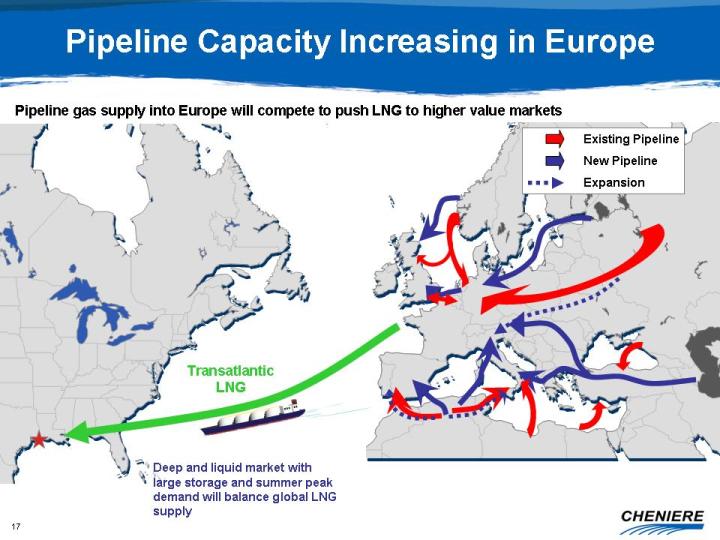

Pipeline Capacity Increasing in Europe Transatlantic LNG Deep and liquid

market

with large storage and summer peak demand will balance global LNG supply

Pipeline gas supply into Europe will compete to push LNG to higher value

markets

(Gp:) New Pipeline (Gp:) Existing Pipeline (Gp:) Expansion

18

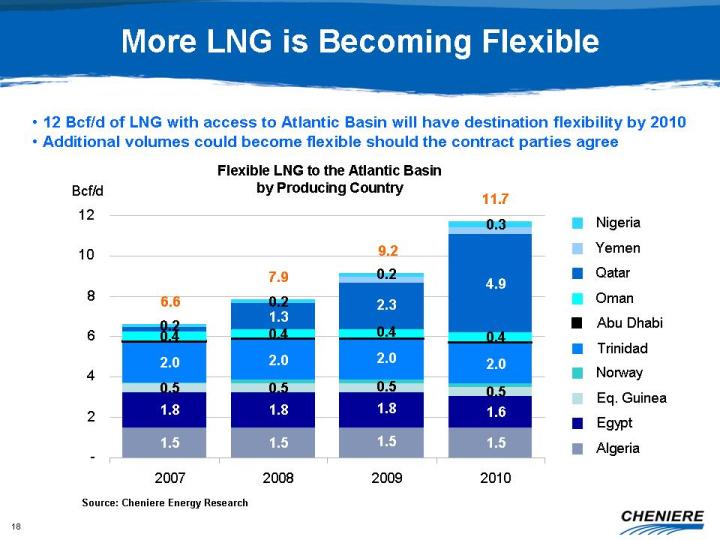

1.5 1.5 1.5 1.5 1.8 1.8 1.8 1.6 0.5 0.5 0.5 0.5 2.0 2.0 2.0 2.0 0.4 0.4 0.4

0.4

1.3 2.3 4.9 0.2 0.2 0.2 0.3 9.2 11.7 7.9 6.6 - 2 4 6 8 10 12 2007 2008 2009

2010

Bcf/d Nigeria Yemen Qatar Oman Abu Dhabi Trinidad Norway Eq. Guinea Egypt

Algeria More LNG is Becoming Flexible Flexible LNG to the Atlantic

Basin by Producing Country 12 Bcf/d of LNG with access to

Atlantic Basin will have destination flexibility by 2010 Additional volumes

could become flexible should the contract parties agree Source: Cheniere

Energy

Research

19

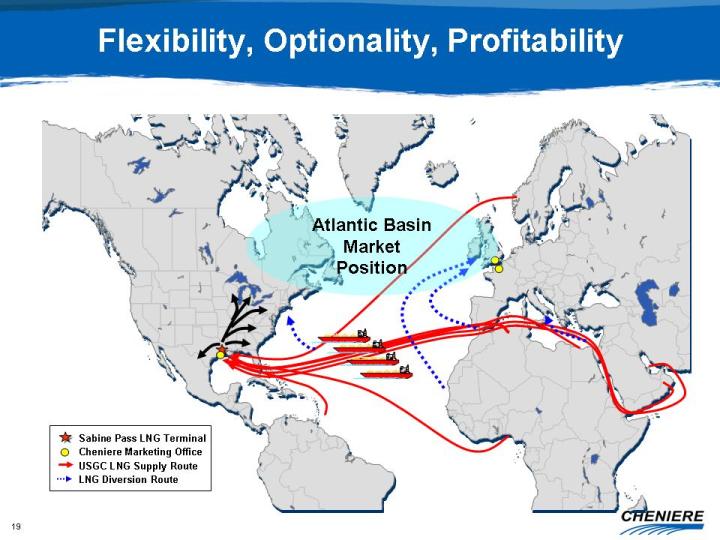

Flexibility, Optionality, Profitability Atlantic

Basin Market Position (Gp:) Sabine Pass LNG Terminal (Gp:)

Cheniere Marketing Office (Gp:) USGC LNG Supply Route (Gp:) LNG Diversion

Route

20

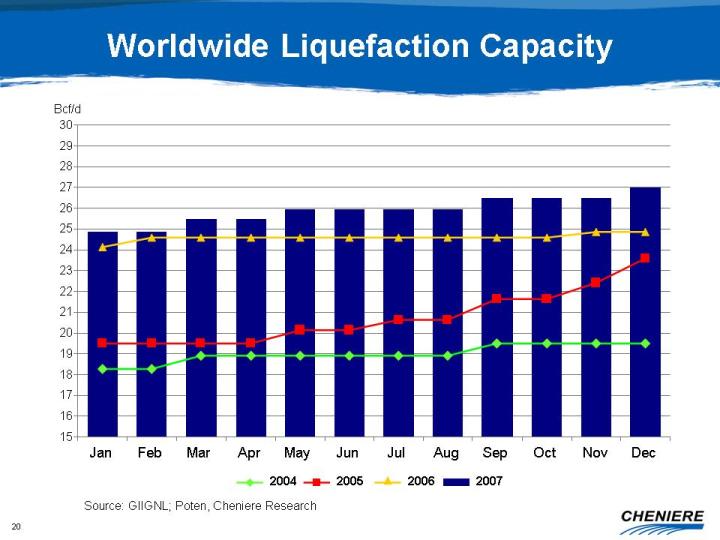

Worldwide Liquefaction Capacity Source: GIIGNL; Poten, Cheniere

Research 15 16 17 18 19 20 21 22 23 24 25 26 27 28 29 30 Jan Feb Mar

Apr May Jun Jul Aug Sep Oct Nov Dec 2007 2004 2005 2006 Bcf/d

21

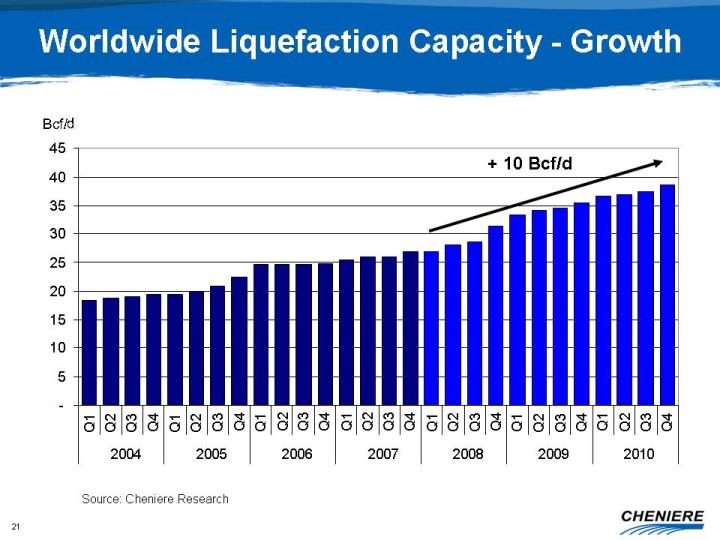

Worldwide Liquefaction Capacity - Growth - 5 10 15 20 25 30 35 40 45 Q1 Q2

Q3 Q4 Q1 Q2 Q3 Q4 Q1 Q2 Q3 Q4 Q1 Q2 Q3 Q4 Q1 Q2 Q3 Q4 Q1 Q2 Q3 Q4 Q1 Q2 Q3

Q4

2004 2005 2006 2007 2008 2009 2010 Bcf/d Source: Cheniere Research +

10 Bcf/d

22

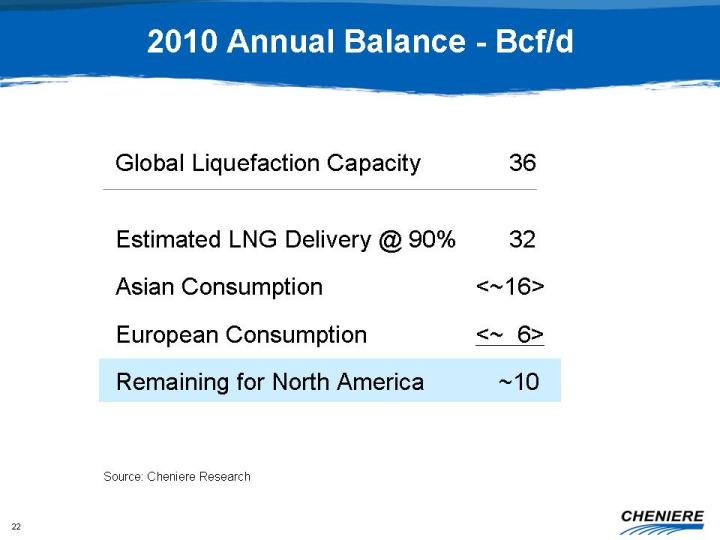

2010 Annual Balance - Bcf/d Global Liquefaction Capacity 36 Estimated LNG

Delivery 90% 32 Asian Consumption 16 European Consumption 6

Remaining for North America 10 Source: Cheniere Research

23

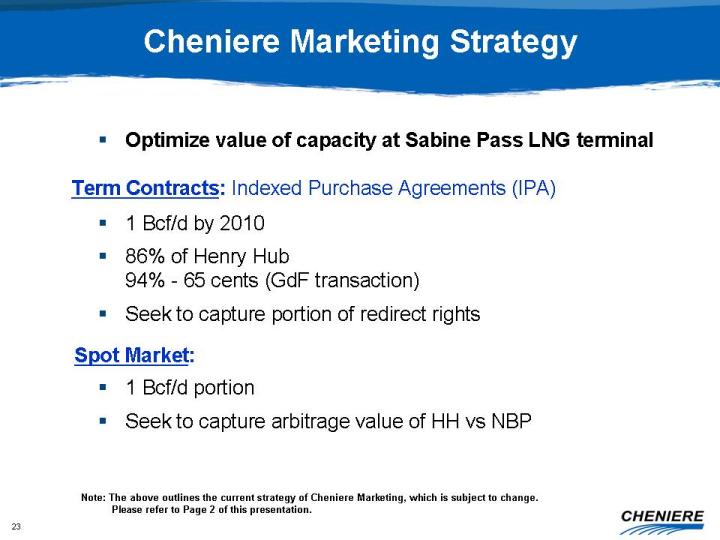

1 Bcf/d by 2010 86% of Henry Hub 94% - 65 cents (GdF transaction) Seek to

capture portion of redirect rights Cheniere Marketing Strategy Term

Contracts: Indexed Purchase Agreements (IPA) Spot Market: 1 Bcf/d portion

Seek

to capture arbitrage value of HH vs NBP Note: The above outlines the current

strategy of Cheniere Marketing, which is subject to change. Please

refer to Page 2 of this presentation. Optimize value of capacity at Sabine

Pass

LNG terminal

24

Cheniere Growth Strategy Continue asset development: terminals and

pipelines Develop a balanced supply portfolio for Cheniere Marketing

between long-term IPA’s and exposure to the spot, option and short-term markets

to optimize seasonality Pursue acquisitions for Cheniere Energy Partners,

L.P.

(AMEX: CQP)