Corporate Presentation

January 2005

*Artist’s Rendition

*Creole Trail LNG L.P. (Cheniere 100%)

*Corpus Christi LNG L.P. (Cheniere G.P. & 67% L.P.)

*Sabine Pass LNG L.P. (Cheniere 100%)

*Freeport LNG L.P. (Cheniere 30% Limited Partner)

Cheniere Energy, Inc.

Safe Harbor Act Statement Under the Private Securities Litigation Reform Act of 1995: Certain information in this presentation are forward looking statements that are based on management's belief, as well as assumptions made by, and information currently available to management. While the company believes that its expectations are based upon reasonable assumptions, there can be no assurances that the company's financial goals will be realized. Numerous uncertainties and risk factors may affect the company's actual results and may cause results to differ materially from those expressed in forward-looking statements made by or on behalf of the company. These uncertainties and risk factors include political, economic, environmental and geological issues, including but not limited to, the continued need for additional capital, the competition within the oil and gas industry, the price of oil and gas, currency fluctuations, and other risks detailed from time to time in the company's periodic reports filed with the United States Securities and Exchange Commission.

Safe Harbor Act

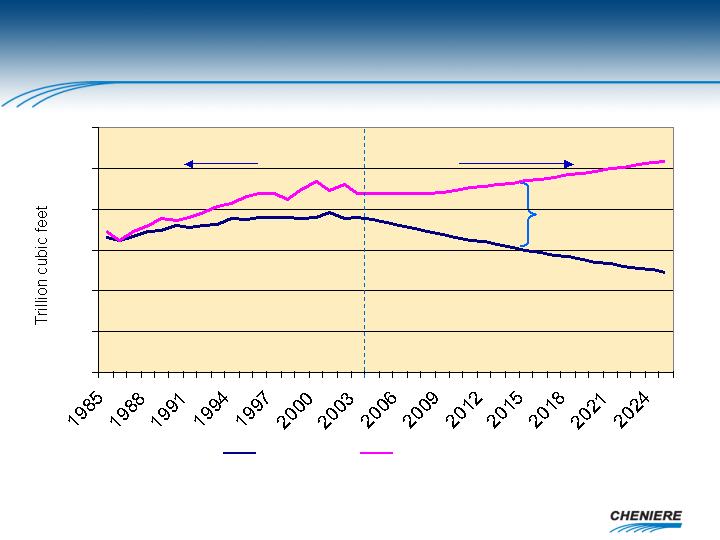

Cheniere estimate based on 2% annual average decline in production,

1% annual average growth in consumption post-2008

8 Tcf

0

5

10

15

20

25

30

Forecast

Historical

Production

Consumption

Production vs Consumption (Tcf)

Source: IHS Energy

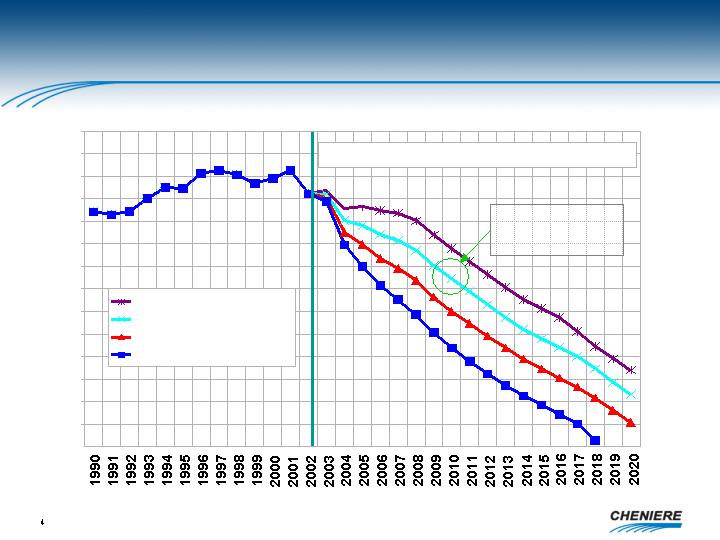

Domestic Production

US Lower 48 Dry Gas Production Forecast

25

27

29

31

33

35

37

39

41

43

45

47

49

51

53

$6/Mcf (89% Rig Utilization)

$5/Mcf (83% Rig Utilization)

$4/Mcf (77% Rig Utilization)

$3/Mcf (71% Rig Utilization)

Bcf/d

Estimate ------------------------------------------------- >

Bcm/d

1.48

1.42

1.37

1.31

1.26

1.14

1.09

1.03

0.98

0.92

0.86

0.81

0.75

0.70

1.20

$5.00 @ 2010

40 Bcf/d

Gulf of Mexico Production

Source: PIRA, 2004

Shallow Water GoM

9.0 Bcf/d

2003 Total U.S. Production = 52 Bcf/d

Deep Water GoM

3.7 Bcf/d

Onshore Gulf

12.71 Bcf/d

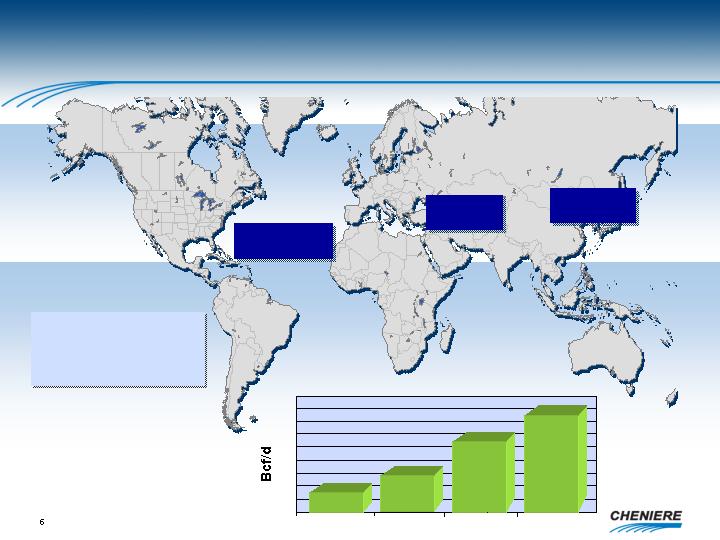

Supplies Ample

Existing &

Committed LNG Capacity 2010

Asia Pacific

14.2 Bcf/d

ME Gulf

12.5 Bcf/d

Atlantic Basin

14.5 Bcf/d

Liquefaction Growth

0

10

20

30

40

1997

2003

2010

30.5

17.1

12.9

2008

Source: GIIGNL, Cheniere Research

41.2

2003 LNG Consumption

Asia – 11 Bcf/d

Europe – 4 Bcf/d

Americas – 2 Bcf/d

Committed Shipping Investment over $13 Billion by 2008

Source: *Poten & Partners July 2004

World Fleet*

Increasing number of ships uncommitted to a trade

Shipping

1995

2001

2003

2008

93

128

152

244

Status of Industry

In the next three years:

Liquefaction growth of 13.4 Bcf/d represents 78%

increase over next 3 years

Shipping growth of 92 vessels represents 60%

increase over next 3 years

The supply - demand gap in the US continues to

make this market the prime target for LNG producers

14 - 18 Bcf/d of regas capacity needed

Bottleneck: U.S. receiving capacity

-

Everett

Closed Access

- Tractebel

Cove Pt.

Fully-reserved

- BP, Statoil & Shell

Elba Island

Fully-reserved

- BG, Marathon

Lake Charles

Fully-reserved

- BG

US LNG Import Facilities

Existing 2.5 Bcf/d

Expanded 5.0 Bcf/d

Source: EIA, FERC, Cheniere Research

Coastal States Gas Consumption

1.0

1.7

0.9

0.8

1.1

0.5

0.6

0.2

0.5

0.6

0.7

Top 5 Coastal Consumers

TX, CA, LA, NY, FLA

Source: EIA, NG Monthly, April 2004

In Bcf/d

2002

10.8

3.2

1.8

6.1

3.2

Source: EIAGIS-Natural Gas Annual, 2001

11

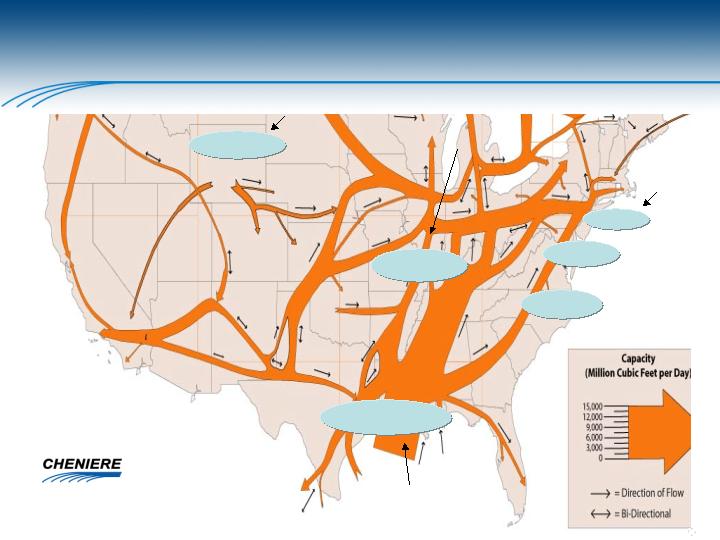

Source: EIA

US Gas Flows - 2001

Into Chicago

Area Hub

Canada to MW

From Gulf Coast

Production

Canada

to NE

Into NY

Metro Area

Into Boston

Metro Area

5.8 Bcf/d

0.5 Bcf/d

0.8 Bcf/d

1.8 Bcf/d

7.2 Bcf/d

19 Bcf/d

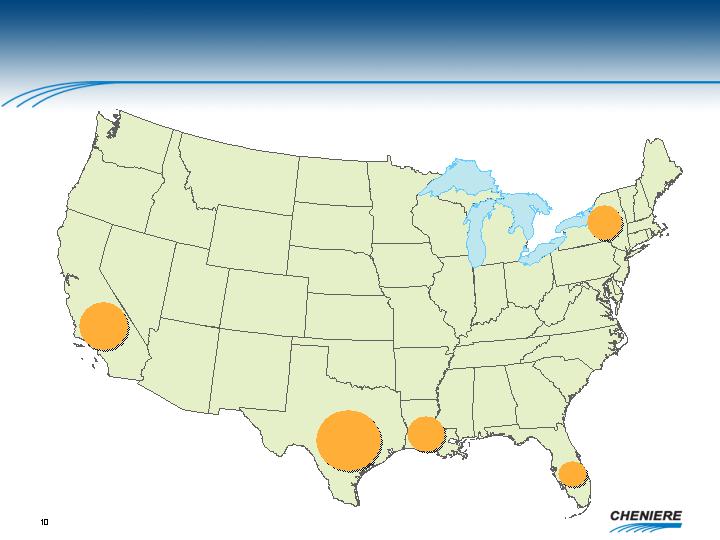

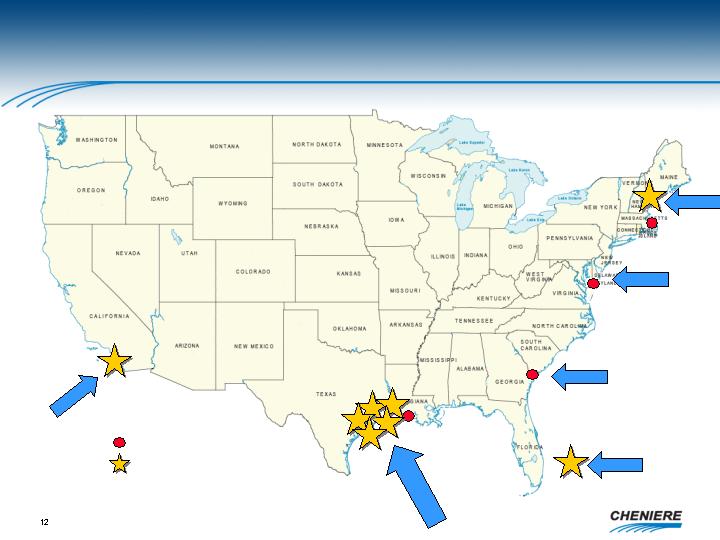

U.S. Regasification Terminal Locations

2010

Existing Facilities

New Terminals

Cheniere Expectation

Creole Trail

4 Deepwater Ports

7 Unloading Docks

12 Storage Tanks

(40 Bcf equivalent)

10 Bcf/d Sendout

Cheniere LNG Receipt Network

Optionality

Flexibility

Reliability

Liquidity

Low Cost

Corpus Christi

Freeport LNG L.P.

Sabine Pass

Project Overviews

NEPA Pre-filing

Start Jan 2005

Expected

Q2 2005

December 2004

June 2004

FERC Permit

1463 acres

610 acres

568 acres

233 acres

Land

Q3 2006

Q3 2005

Q1 2005

Q1 2005

Estimated

Ground Breaking

13.5 Bcfe

10.1 Bcfe

10.1 Bcfe

6.7 Bcfe

Storage Capacity

$850 - $950

million

$650 - $750

million

$750 – $850

million

$650 – $750

million

Capex*

4 tanks

3 tanks

3 tanks

2 tanks

Tanks

2 docks

3.3 Bcf/d

Creole Trail

2 docks

2 docks

1 dock

Berths

Initial Capacity

2.6 Bcf/d

2.6 Bcf/d

1.5 Bcf/d

Corpus Christi

Sabine Pass

Freeport LNG**

*Estimated construction costs before financing costs

**Freeport LNG L.P. (Cheniere 30% Limited Partner)

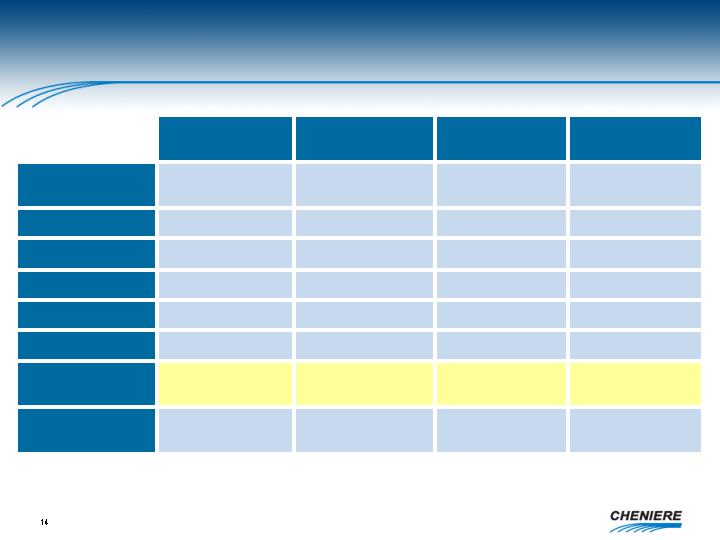

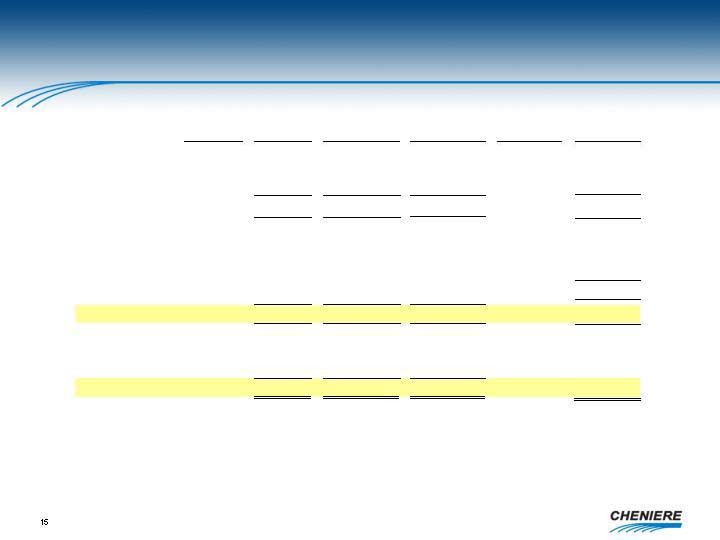

Terminal Capacity Sales & Cheniere Financial Impact

Total

Retained

Long-term

Tariff

*Calculated

TUA

Capacity

Capacity

TUAs

Rate

Revenues to Cheniere

Status

(Bcf/d)

(Bcf/d)

(Bcf/d)

($/Mmbtu)

($MM)

Freeport LNG L.P. (Cheniere 30% Limited Partner)

ConocoPhillips

Contracted

-

1.0

Dow Chemical

Contracted

-

0.5

1.5

-

1.5

15

$

Sabine Pass

Total S.A.

Contracted

-

1.0

0.32

$

125

**ChevronTexaco

-

0.7

0.32

$

90

2.6

0.9

1.7

215

Total to date – Contracted

4.1

0.9

3.2

230

Corpus Christi LNG

(Cheniere 67% Limited Partner)

Marketing

2.6

1.1

1.5

?

Creole Trail

Marketing

3.3

1.3

2.0

?

Total

10.0

3.3

6.7

?

Expansions

Potential

2.0

2.0

-

?

Note: Operating expenses for the Sabine Pass terminal (2.6 Bcf/d capacity) are estimated to be $25-30 MM/year.

Sabine Pass will also retain 2% of throughput for fuel usage.

*Calculated revenues are based solely on TUA’s currently contracted and reflect numerous assumptions. In the case of Freeport LNG L.P.

revenues, they represent the mid-point of the currently estimated pre-tax cash distributions for our minority interest of $10-20 MM/year.

**ChevronTexaco has the option to reduce to 500 MMcf/d until July 2005 or increase to 1 Bcf/d by December 2005.

Contracted

$

Low Risk Base Business

Provider of service for fees

Conventional, proved technology

Anchor customer strategy

Large customers: 500 MMcf/d - 1 Bcf/d each

Credit-worthy

Long-term commitments – take or pay

Covers facility costs, debt service, reasonable equity return

Cheniere’s Competitive Advantage

Early mover = prime real estate

Low cost supplier of LNG regas capacity

Local support

Size of sites

Economies of scale

Existing technology

Transparency: $0.32/MMbtu

Flexibility

Logistics

Marketing

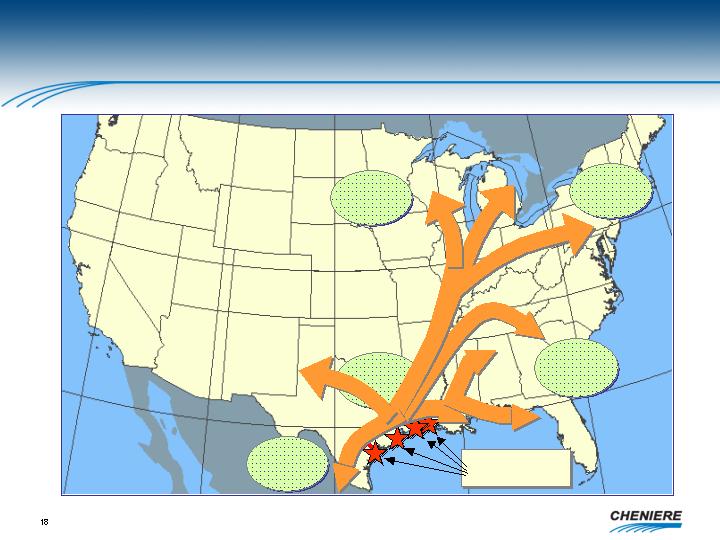

Target Gas Demand Corridor

Market Access – 29 Bcf/d

Cheniere LNG

Receipt Network

Source: Cheniere Research

Mexican

Markets

1.7 Bcf/d

Gulf Coast

Markets

4.9 Bcfd

Southeast

Markets

4.6 Bcfd

Northeast

Markets

5.7 Bcfd

Midwest

Markets

11.8 Bcfd