0000003570false--12-312025FYhttp://fasb.org/us-gaap/2025#Revenueshttp://fasb.org/us-gaap/2025#Revenueshttp://fasb.org/us-gaap/2025#Revenueshttp://fasb.org/us-gaap/2025#DerivativeAssetsCurrenthttp://fasb.org/us-gaap/2025#DerivativeAssetsCurrenthttp://fasb.org/us-gaap/2025#DerivativeAssetsNoncurrenthttp://fasb.org/us-gaap/2025#DerivativeAssetsNoncurrenthttp://fasb.org/us-gaap/2025#DerivativeLiabilitiesCurrenthttp://fasb.org/us-gaap/2025#DerivativeLiabilitiesCurrenthttp://fasb.org/us-gaap/2025#DerivativeLiabilitiesNoncurrenthttp://fasb.org/us-gaap/2025#DerivativeLiabilitiesNoncurrenthttp://fasb.org/us-gaap/2025#DerivativeAssetsCurrenthttp://fasb.org/us-gaap/2025#DerivativeAssetsCurrenthttp://fasb.org/us-gaap/2025#DerivativeAssetsNoncurrenthttp://fasb.org/us-gaap/2025#DerivativeAssetsNoncurrenthttp://fasb.org/us-gaap/2025#DerivativeLiabilitiesCurrenthttp://fasb.org/us-gaap/2025#DerivativeLiabilitiesCurrenthttp://fasb.org/us-gaap/2025#DerivativeLiabilitiesNoncurrenthttp://fasb.org/us-gaap/2025#DerivativeLiabilitiesNoncurrentSOFR or base rateSOFR or base rateSOFR or base rateSOFR or base rateSOFR or base ratehttp://fasb.org/us-gaap/2025#OperatingLeaseRightOfUseAssethttp://fasb.org/us-gaap/2025#OperatingLeaseRightOfUseAssethttp://fasb.org/us-gaap/2025#PropertyPlantAndEquipmentNethttp://fasb.org/us-gaap/2025#PropertyPlantAndEquipmentNethttp://fasb.org/us-gaap/2025#OperatingLeaseLiabilityCurrenthttp://fasb.org/us-gaap/2025#OperatingLeaseLiabilityCurrenthttp://fasb.org/us-gaap/2025#OtherLiabilitiesCurrenthttp://fasb.org/us-gaap/2025#OtherLiabilitiesCurrenthttp://fasb.org/us-gaap/2025#OperatingLeaseLiabilityNoncurrenthttp://fasb.org/us-gaap/2025#OperatingLeaseLiabilityNoncurrenthttp://fasb.org/us-gaap/2025#OtherLiabilitiesNoncurrenthttp://fasb.org/us-gaap/2025#OtherLiabilitiesNoncurrent1iso4217:USDxbrli:sharesiso4217:USDxbrli:shareslng:unitlng:itemutr:mixbrli:purelng:customerlng:tbtulng:unitslng:Employees00000035702025-01-012025-12-3100000035702025-06-3000000035702026-02-200000003570lng:LiquefiedNaturalGasMember2025-01-012025-12-310000003570lng:LiquefiedNaturalGasMember2024-01-012024-12-310000003570lng:LiquefiedNaturalGasMember2023-01-012023-12-310000003570lng:RegasificationServiceMember2025-01-012025-12-310000003570lng:RegasificationServiceMember2024-01-012024-12-310000003570lng:RegasificationServiceMember2023-01-012023-12-310000003570us-gaap:ProductAndServiceOtherMember2025-01-012025-12-310000003570us-gaap:ProductAndServiceOtherMember2024-01-012024-12-310000003570us-gaap:ProductAndServiceOtherMember2023-01-012023-12-3100000035702024-01-012024-12-3100000035702023-01-012023-12-3100000035702025-12-3100000035702024-12-310000003570us-gaap:VariableInterestEntityPrimaryBeneficiaryMember2025-12-310000003570us-gaap:CommonStockMember2022-12-310000003570us-gaap:TreasuryStockCommonMember2022-12-310000003570us-gaap:AdditionalPaidInCapitalMember2022-12-310000003570us-gaap:RetainedEarningsMember2022-12-310000003570us-gaap:NoncontrollingInterestMember2022-12-3100000035702022-12-310000003570lng:RedeemableNoncontrollingInterestMember2022-12-310000003570us-gaap:RetainedEarningsMember2023-01-012023-12-310000003570us-gaap:NoncontrollingInterestMember2023-01-012023-12-310000003570lng:O2023ADividendsMember2023-01-012023-12-310000003570us-gaap:CommonStockMember2023-01-012023-12-310000003570us-gaap:TreasuryStockCommonMember2023-01-012023-12-310000003570us-gaap:AdditionalPaidInCapitalMember2023-01-012023-12-310000003570us-gaap:CommonStockMember2023-12-310000003570us-gaap:TreasuryStockCommonMember2023-12-310000003570us-gaap:AdditionalPaidInCapitalMember2023-12-310000003570us-gaap:RetainedEarningsMember2023-12-310000003570us-gaap:NoncontrollingInterestMember2023-12-3100000035702023-12-310000003570lng:RedeemableNoncontrollingInterestMember2023-12-310000003570us-gaap:RetainedEarningsMember2024-01-012024-12-310000003570us-gaap:NoncontrollingInterestMember2024-01-012024-12-310000003570lng:O2024ADividendsMember2024-01-012024-12-310000003570us-gaap:CommonStockMember2024-01-012024-12-310000003570us-gaap:TreasuryStockCommonMember2024-01-012024-12-310000003570lng:RedeemableNoncontrollingInterestMember2024-01-012024-12-310000003570us-gaap:AdditionalPaidInCapitalMember2024-01-012024-12-310000003570us-gaap:CommonStockMember2024-12-310000003570us-gaap:TreasuryStockCommonMember2024-12-310000003570us-gaap:AdditionalPaidInCapitalMember2024-12-310000003570us-gaap:RetainedEarningsMember2024-12-310000003570us-gaap:NoncontrollingInterestMember2024-12-310000003570lng:RedeemableNoncontrollingInterestMember2024-12-310000003570us-gaap:RetainedEarningsMember2025-01-012025-12-310000003570us-gaap:NoncontrollingInterestMember2025-01-012025-12-310000003570lng:RedeemableNoncontrollingInterestMember2025-01-012025-12-310000003570lng:O2025ADividendsMember2025-01-012025-12-310000003570us-gaap:CommonStockMember2025-01-012025-12-310000003570us-gaap:TreasuryStockCommonMember2025-01-012025-12-310000003570us-gaap:AdditionalPaidInCapitalMember2025-01-012025-12-310000003570us-gaap:CommonStockMember2025-12-310000003570us-gaap:TreasuryStockCommonMember2025-12-310000003570us-gaap:AdditionalPaidInCapitalMember2025-12-310000003570us-gaap:RetainedEarningsMember2025-12-310000003570us-gaap:NoncontrollingInterestMember2025-12-310000003570lng:RedeemableNoncontrollingInterestMember2025-12-310000003570srt:MinimumMember2025-01-012025-12-310000003570lng:UnderConstructionMembersrt:MinimumMember2025-01-012025-12-310000003570lng:OperationalStatusMembersrt:MinimumMemberlng:SabinePassLNGTerminalMember2025-01-012025-12-310000003570lng:SabinePassLNGTerminalMember2025-01-012025-12-310000003570lng:CreoleTrailPipelineMember2025-01-012025-12-310000003570lng:CheniereEnergyPartnersLPMemberus-gaap:GeneralPartnerMember2025-01-012025-12-310000003570lng:CheniereEnergyPartnersLPMember2025-01-012025-12-310000003570srt:MinimumMemberlng:CorpusChristiLNGTerminalMember2025-01-012025-12-310000003570lng:UnderConstructionMembersrt:MinimumMemberlng:CorpusChristiLNGTerminalMember2025-01-012025-12-310000003570lng:CorpusChristiLNGTerminalMember2025-01-012025-12-310000003570lng:CorpusChristiPipelineMember2025-01-012025-12-310000003570lng:CorpusChristiStage3ProjectMember2025-01-012025-12-310000003570srt:MinimumMemberlng:CorpusChristiStage3ProjectMember2025-01-012025-12-310000003570lng:UnderConstructionMemberlng:CorpusChristiStage3ProjectMember2025-01-012025-12-310000003570lng:OperationalStatusMemberlng:CorpusChristiStage3ProjectMember2025-01-012025-12-310000003570lng:MidscaleTrains89ProjectMember2025-01-012025-12-310000003570lng:UnderConstructionMemberlng:MidscaleTrains89ProjectMember2025-01-012025-12-310000003570lng:SPACustomersMemberus-gaap:CustomerConcentrationRiskMember2025-01-012025-12-310000003570srt:MaximumMemberlng:SabinePassLNGTerminalMember2025-12-310000003570lng:SabinePassLNGTerminalMember2025-12-310000003570lng:CreoleTrailPipelineMember2025-12-310000003570lng:CorpusChristiPipelineMember2025-12-310000003570lng:SabinePassLiquefactionAndCorpusChristiLiquefactionMember2025-12-310000003570lng:SabinePassLiquefactionAndCorpusChristiLiquefactionMember2024-12-310000003570lng:CheniereMarketingLLCMember2025-12-310000003570lng:CheniereMarketingLLCMember2024-12-310000003570lng:OtherSubsidiariesMember2025-12-310000003570lng:OtherSubsidiariesMember2024-12-310000003570lng:MaterialsInventoryMember2025-12-310000003570lng:MaterialsInventoryMember2024-12-310000003570lng:LiquefiedNaturalGasInventoryMember2025-12-310000003570lng:LiquefiedNaturalGasInventoryMember2024-12-310000003570lng:LiquefiedNaturalGasInTransitInventoryMember2025-12-310000003570lng:LiquefiedNaturalGasInTransitInventoryMember2024-12-310000003570lng:NaturalGasInventoryMember2025-12-310000003570lng:NaturalGasInventoryMember2024-12-310000003570lng:OtherInventoryMember2025-12-310000003570lng:OtherInventoryMember2024-12-310000003570srt:MinimumMemberlng:TerminalAndInterconnectingPipelineFacilitiesMember2025-12-310000003570srt:MaximumMemberlng:TerminalAndInterconnectingPipelineFacilitiesMember2025-12-310000003570lng:TerminalAndInterconnectingPipelineFacilitiesMember2025-12-310000003570lng:TerminalAndInterconnectingPipelineFacilitiesMember2024-12-310000003570us-gaap:LandAndLandImprovementsMember2025-12-310000003570us-gaap:LandAndLandImprovementsMember2024-12-310000003570us-gaap:ConstructionInProgressMember2025-12-310000003570us-gaap:ConstructionInProgressMember2024-12-310000003570lng:TerminalAndRelatedAssetsMember2025-12-310000003570lng:TerminalAndRelatedAssetsMember2024-12-310000003570srt:MinimumMemberlng:FixedAssetsMember2025-12-310000003570srt:MaximumMemberlng:FixedAssetsMember2025-12-310000003570lng:FixedAssetsMember2025-12-310000003570lng:FixedAssetsMember2024-12-310000003570srt:MinimumMemberus-gaap:AssetsHeldUnderCapitalLeasesMember2025-12-310000003570srt:MaximumMemberus-gaap:AssetsHeldUnderCapitalLeasesMember2025-12-310000003570us-gaap:AssetsHeldUnderCapitalLeasesMember2025-12-310000003570us-gaap:AssetsHeldUnderCapitalLeasesMember2024-12-310000003570us-gaap:PriceRiskDerivativeMemberus-gaap:FairValueInputsLevel1Member2025-12-310000003570us-gaap:PriceRiskDerivativeMemberus-gaap:FairValueInputsLevel2Member2025-12-310000003570us-gaap:PriceRiskDerivativeMemberus-gaap:FairValueInputsLevel3Member2025-12-310000003570us-gaap:PriceRiskDerivativeMember2025-12-310000003570us-gaap:PriceRiskDerivativeMemberus-gaap:FairValueInputsLevel1Member2024-12-310000003570us-gaap:PriceRiskDerivativeMemberus-gaap:FairValueInputsLevel2Member2024-12-310000003570us-gaap:PriceRiskDerivativeMemberus-gaap:FairValueInputsLevel3Member2024-12-310000003570us-gaap:PriceRiskDerivativeMember2024-12-310000003570lng:LNGTradingDerivativeMemberus-gaap:FairValueInputsLevel1Member2025-12-310000003570lng:LNGTradingDerivativeMemberus-gaap:FairValueInputsLevel2Member2025-12-310000003570lng:LNGTradingDerivativeMemberus-gaap:FairValueInputsLevel3Member2025-12-310000003570lng:LNGTradingDerivativeMember2025-12-310000003570lng:LNGTradingDerivativeMemberus-gaap:FairValueInputsLevel1Member2024-12-310000003570lng:LNGTradingDerivativeMemberus-gaap:FairValueInputsLevel2Member2024-12-310000003570lng:LNGTradingDerivativeMemberus-gaap:FairValueInputsLevel3Member2024-12-310000003570lng:LNGTradingDerivativeMember2024-12-310000003570us-gaap:ForeignExchangeContractMemberus-gaap:FairValueInputsLevel1Member2025-12-310000003570us-gaap:ForeignExchangeContractMemberus-gaap:FairValueInputsLevel2Member2025-12-310000003570us-gaap:ForeignExchangeContractMemberus-gaap:FairValueInputsLevel3Member2025-12-310000003570us-gaap:ForeignExchangeContractMember2025-12-310000003570us-gaap:ForeignExchangeContractMemberus-gaap:FairValueInputsLevel1Member2024-12-310000003570us-gaap:ForeignExchangeContractMemberus-gaap:FairValueInputsLevel2Member2024-12-310000003570us-gaap:ForeignExchangeContractMemberus-gaap:FairValueInputsLevel3Member2024-12-310000003570us-gaap:ForeignExchangeContractMember2024-12-310000003570us-gaap:PriceRiskDerivativeMemberus-gaap:FairValueInputsLevel3Memberus-gaap:MarketApproachValuationTechniqueMembersrt:MinimumMember2025-01-012025-12-310000003570us-gaap:PriceRiskDerivativeMemberus-gaap:FairValueInputsLevel3Memberus-gaap:MarketApproachValuationTechniqueMembersrt:MaximumMember2025-01-012025-12-310000003570us-gaap:PriceRiskDerivativeMemberus-gaap:FairValueInputsLevel3Memberus-gaap:MarketApproachValuationTechniqueMembersrt:WeightedAverageMember2025-01-012025-12-310000003570us-gaap:PriceRiskDerivativeMemberus-gaap:FairValueInputsLevel3Memberus-gaap:ValuationTechniqueOptionPricingModelMembersrt:MinimumMember2025-01-012025-12-310000003570us-gaap:PriceRiskDerivativeMemberus-gaap:FairValueInputsLevel3Memberus-gaap:ValuationTechniqueOptionPricingModelMembersrt:MaximumMember2025-01-012025-12-310000003570us-gaap:PriceRiskDerivativeMemberus-gaap:FairValueInputsLevel3Memberus-gaap:ValuationTechniqueOptionPricingModelMembersrt:WeightedAverageMember2025-01-012025-12-310000003570us-gaap:PriceRiskDerivativeMember2023-12-310000003570us-gaap:PriceRiskDerivativeMember2022-12-310000003570us-gaap:PriceRiskDerivativeMember2025-01-012025-12-310000003570us-gaap:PriceRiskDerivativeMember2024-01-012024-12-310000003570us-gaap:PriceRiskDerivativeMember2023-01-012023-12-310000003570us-gaap:PriceRiskDerivativeMembersrt:MaximumMember2025-01-012025-12-310000003570lng:LNGTradingDerivativeMembersrt:MaximumMember2025-01-012025-12-310000003570us-gaap:CommodityContractMember2025-01-012025-12-310000003570lng:LNGTradingDerivativeMemberus-gaap:SalesMember2025-01-012025-12-310000003570lng:LNGTradingDerivativeMemberus-gaap:SalesMember2024-01-012024-12-310000003570lng:LNGTradingDerivativeMemberus-gaap:SalesMember2023-01-012023-12-310000003570lng:LNGTradingDerivativeMemberus-gaap:CostOfSalesMember2025-01-012025-12-310000003570lng:LNGTradingDerivativeMemberus-gaap:CostOfSalesMember2024-01-012024-12-310000003570lng:LNGTradingDerivativeMemberus-gaap:CostOfSalesMember2023-01-012023-12-310000003570us-gaap:PriceRiskDerivativeMemberus-gaap:SalesMember2025-01-012025-12-310000003570us-gaap:PriceRiskDerivativeMemberus-gaap:SalesMember2024-01-012024-12-310000003570us-gaap:PriceRiskDerivativeMemberus-gaap:SalesMember2023-01-012023-12-310000003570us-gaap:PriceRiskDerivativeMemberus-gaap:CostOfSalesMember2025-01-012025-12-310000003570us-gaap:PriceRiskDerivativeMemberus-gaap:CostOfSalesMember2024-01-012024-12-310000003570us-gaap:PriceRiskDerivativeMemberus-gaap:CostOfSalesMember2023-01-012023-12-310000003570us-gaap:ForeignExchangeContractMembersrt:MaximumMember2025-01-012025-12-310000003570us-gaap:ForeignExchangeContractMember2025-01-012025-12-310000003570us-gaap:ForeignExchangeContractMember2023-01-012023-12-310000003570us-gaap:ForeignExchangeContractMember2024-01-012024-12-310000003570lng:PriceRiskDerivativeAssetMember2025-12-310000003570lng:LNGTradingDerivativeAssetMember2025-12-310000003570lng:ForeignExchangeContractAssetMember2025-12-310000003570lng:PriceRiskDerivativeLiabilityMember2025-12-310000003570lng:LNGTradingDerivativesLiabilityMember2025-12-310000003570lng:ForeignExchangeContractLiabilityMember2025-12-310000003570lng:PriceRiskDerivativeAssetMember2024-12-310000003570lng:LNGTradingDerivativeAssetMember2024-12-310000003570lng:ForeignExchangeContractAssetMember2024-12-310000003570lng:PriceRiskDerivativeLiabilityMember2024-12-310000003570lng:LNGTradingDerivativesLiabilityMember2024-12-310000003570lng:ForeignExchangeContractLiabilityMember2024-12-310000003570lng:BlackstoneInc.AndBrookfieldAssetManagementInc.AndThePublicMember2025-01-012025-12-310000003570lng:CheniereEnergyPartnersGPLLCMemberlng:CQPHoldcoLPMember2025-01-012025-12-310000003570lng:CheniereEnergyPartnersGPLLCMemberlng:CheniereEnergyIncMember2025-01-012025-12-310000003570lng:CheniereEnergyPartnersGPLLCMemberlng:CQPHoldcoLPAndCheniereEnergyIncMember2025-01-012025-12-310000003570lng:CQPHoldcoLPMember2025-01-012025-12-310000003570lng:CheniereEnergyPartnersLPMemberlng:DirectorAppointmentEntitlementMinimumMemberlng:CQPHoldcoLPMember2025-01-012025-12-310000003570us-gaap:VariableInterestEntityPrimaryBeneficiaryMember2025-01-012025-12-310000003570us-gaap:VariableInterestEntityPrimaryBeneficiaryMember2024-12-310000003570lng:A2025SabinePassLiquefactionSeniorNotesMember2025-12-310000003570lng:A2025SabinePassLiquefactionSeniorNotesMember2024-12-310000003570lng:A2026SabinePassLiquefactionSeniorNotesMember2025-12-310000003570lng:A2026SabinePassLiquefactionSeniorNotesMember2024-12-310000003570lng:A2027SabinePassLiquefactionSeniorNotesMember2025-12-310000003570lng:A2027SabinePassLiquefactionSeniorNotesMember2024-12-310000003570lng:A2028SabinePassLiquefactionSeniorNotesMember2025-12-310000003570lng:A2028SabinePassLiquefactionSeniorNotesMember2024-12-310000003570lng:A2030SabinePassLiquefactionSeniorNotesMember2025-12-310000003570lng:A2030SabinePassLiquefactionSeniorNotesMember2024-12-310000003570lng:A2037SabinePassLiquefactionNotesMembersrt:WeightedAverageMember2025-12-310000003570lng:A2037SabinePassLiquefactionNotesMembersrt:WeightedAverageMember2024-12-310000003570lng:A2037SabinePassLiquefactionNotesMember2025-12-310000003570lng:A2037SabinePassLiquefactionNotesMember2024-12-310000003570lng:SabinePassLiquefactionSeniorNotesMember2025-12-310000003570lng:SabinePassLiquefactionSeniorNotesMember2024-12-310000003570lng:SPLRevolvingCreditFacilityMember2025-12-310000003570lng:SPLRevolvingCreditFacilityMember2024-12-310000003570lng:SabinePassLiquefactionMember2025-12-310000003570lng:SabinePassLiquefactionMember2024-12-310000003570lng:A2029CheniereEnergyPartnersSeniorNotesMember2025-12-310000003570lng:A2029CheniereEnergyPartnersSeniorNotesMember2024-12-310000003570lng:A2031CheniereEnergyPartnersSeniorNotesMember2025-12-310000003570lng:A2031CheniereEnergyPartnersSeniorNotesMember2024-12-310000003570lng:A2032CheniereEnergyPartnersSeniorNotesMember2025-12-310000003570lng:A2032CheniereEnergyPartnersSeniorNotesMember2024-12-310000003570lng:A2033CheniereEnergyPartnersSeniorNotesMember2025-12-310000003570lng:A2033CheniereEnergyPartnersSeniorNotesMember2024-12-310000003570lng:A2034CheniereEnergyPartnersSeniorNotesMember2025-12-310000003570lng:A2034CheniereEnergyPartnersSeniorNotesMember2024-12-310000003570lng:A2035CheniereEnergyPartnersSeniorNotesMember2025-12-310000003570lng:A2035CheniereEnergyPartnersSeniorNotesMember2024-12-310000003570lng:CheniereEnergyPartnersSeniorNotesMember2025-12-310000003570lng:CheniereEnergyPartnersSeniorNotesMember2024-12-310000003570lng:CQPRevolvingCreditFacilityMember2025-12-310000003570lng:CQPRevolvingCreditFacilityMember2024-12-310000003570lng:CheniereEnergyPartnersLPMember2025-12-310000003570lng:CheniereEnergyPartnersLPMember2024-12-310000003570lng:A2027CorpusChristiHoldingsSeniorNotesMember2025-12-310000003570lng:A2027CorpusChristiHoldingsSeniorNotesMember2024-12-310000003570lng:A2029CorpusChristiHoldingsSeniorNotesMember2025-12-310000003570lng:A2029CorpusChristiHoldingsSeniorNotesMember2024-12-310000003570lng:A2039CorpusChristiHoldingsSeniorNotesMembersrt:WeightedAverageMember2025-12-310000003570lng:A2039CorpusChristiHoldingsSeniorNotesMember2025-12-310000003570lng:A2039CorpusChristiHoldingsSeniorNotesMember2024-12-310000003570lng:CorpusChristiHoldingsSeniorNotesMember2025-12-310000003570lng:CorpusChristiHoldingsSeniorNotesMember2024-12-310000003570lng:A2015CCHTermLoanFacilityMember2025-12-310000003570lng:A2015CCHTermLoanFacilityMember2024-12-310000003570lng:CorpusChristiHoldingsWorkingCapitalFacilityMember2025-12-310000003570lng:CorpusChristiHoldingsWorkingCapitalFacilityMember2024-12-310000003570lng:CheniereCorpusChristiHoldingsLLCMember2025-12-310000003570lng:CheniereCorpusChristiHoldingsLLCMember2024-12-310000003570lng:A2028CheniereSeniorSecuredNotesMember2025-12-310000003570lng:A2028CheniereSeniorSecuredNotesMember2024-12-310000003570lng:A2034CheniereSeniorNotesMember2025-12-310000003570lng:A2034CheniereSeniorNotesMember2024-12-310000003570lng:CheniereSeniorNotesMember2025-12-310000003570lng:CheniereSeniorNotesMember2024-12-310000003570lng:CheniereRevolvingCreditFacilityMember2025-12-310000003570lng:CheniereRevolvingCreditFacilityMember2024-12-310000003570srt:ParentCompanyMember2025-12-310000003570srt:ParentCompanyMember2024-12-310000003570lng:A2026SabinePassLiquefactionSeniorNotesMemberus-gaap:SubsequentEventMember2026-02-012026-02-250000003570lng:CheniereEnergyPartners2029SeniorNotes2031SeniorNotesAnd2032SeniorNotesMemberlng:CheniereEnergyPartnersLPMember2025-01-012025-12-310000003570lng:SPLRevolvingCreditFacilityMemberus-gaap:SecuredOvernightFinancingRateSofrOvernightIndexSwapRateMember2025-01-012025-12-310000003570us-gaap:SecuredOvernightFinancingRateSofrOvernightIndexSwapRateMemberlng:SPLRevolvingCreditFacilityMembersrt:MinimumMember2025-01-012025-12-310000003570us-gaap:SecuredOvernightFinancingRateSofrOvernightIndexSwapRateMemberlng:SPLRevolvingCreditFacilityMembersrt:MaximumMember2025-01-012025-12-310000003570us-gaap:BaseRateMemberlng:SPLRevolvingCreditFacilityMembersrt:MinimumMember2025-01-012025-12-310000003570us-gaap:BaseRateMemberlng:SPLRevolvingCreditFacilityMembersrt:MaximumMember2025-01-012025-12-310000003570lng:CQPRevolvingCreditFacilityMemberus-gaap:SecuredOvernightFinancingRateSofrOvernightIndexSwapRateMember2025-01-012025-12-310000003570us-gaap:SecuredOvernightFinancingRateSofrOvernightIndexSwapRateMemberlng:CQPRevolvingCreditFacilityMembersrt:MinimumMember2025-01-012025-12-310000003570us-gaap:SecuredOvernightFinancingRateSofrOvernightIndexSwapRateMemberlng:CQPRevolvingCreditFacilityMembersrt:MaximumMember2025-01-012025-12-310000003570us-gaap:BaseRateMemberlng:CQPRevolvingCreditFacilityMembersrt:MinimumMember2025-01-012025-12-310000003570us-gaap:BaseRateMemberlng:CQPRevolvingCreditFacilityMembersrt:MaximumMember2025-01-012025-12-310000003570lng:A2015CCHTermLoanFacilityMemberus-gaap:SecuredOvernightFinancingRateSofrOvernightIndexSwapRateMember2025-01-012025-12-310000003570lng:A2015CCHTermLoanFacilityMemberus-gaap:BaseRateMember2025-01-012025-12-310000003570lng:CorpusChristiHoldingsWorkingCapitalFacilityMemberus-gaap:SecuredOvernightFinancingRateSofrOvernightIndexSwapRateMember2025-01-012025-12-310000003570us-gaap:SecuredOvernightFinancingRateSofrOvernightIndexSwapRateMemberlng:CorpusChristiHoldingsWorkingCapitalFacilityMembersrt:MinimumMember2025-01-012025-12-310000003570us-gaap:SecuredOvernightFinancingRateSofrOvernightIndexSwapRateMemberlng:CorpusChristiHoldingsWorkingCapitalFacilityMembersrt:MaximumMember2025-01-012025-12-310000003570us-gaap:BaseRateMemberlng:CorpusChristiHoldingsWorkingCapitalFacilityMembersrt:MinimumMember2025-01-012025-12-310000003570us-gaap:BaseRateMemberlng:CorpusChristiHoldingsWorkingCapitalFacilityMembersrt:MaximumMember2025-01-012025-12-310000003570us-gaap:SecuredOvernightFinancingRateSofrOvernightIndexSwapRateMemberlng:CheniereRevolvingCreditFacilityMembersrt:MinimumMember2025-01-012025-12-310000003570us-gaap:SecuredOvernightFinancingRateSofrOvernightIndexSwapRateMemberlng:CheniereRevolvingCreditFacilityMembersrt:MaximumMember2025-01-012025-12-310000003570us-gaap:BaseRateMemberlng:CheniereRevolvingCreditFacilityMembersrt:MinimumMember2025-01-012025-12-310000003570us-gaap:BaseRateMemberlng:CheniereRevolvingCreditFacilityMembersrt:MaximumMember2025-01-012025-12-310000003570lng:SPLRevolvingCreditFacilityMembersrt:MinimumMember2025-01-012025-12-310000003570lng:SPLRevolvingCreditFacilityMembersrt:MaximumMember2025-01-012025-12-310000003570lng:CQPRevolvingCreditFacilityMembersrt:MinimumMember2025-01-012025-12-310000003570lng:CQPRevolvingCreditFacilityMembersrt:MaximumMember2025-01-012025-12-310000003570lng:A2015CCHTermLoanFacilityMember2025-01-012025-12-310000003570lng:CorpusChristiHoldingsWorkingCapitalFacilityMembersrt:MinimumMember2025-01-012025-12-310000003570lng:CorpusChristiHoldingsWorkingCapitalFacilityMembersrt:MaximumMember2025-01-012025-12-310000003570lng:CheniereRevolvingCreditFacilityMembersrt:MinimumMember2025-01-012025-12-310000003570lng:CheniereRevolvingCreditFacilityMembersrt:MaximumMember2025-01-012025-12-310000003570us-gaap:LetterOfCreditMemberlng:SPLRevolvingCreditFacilityMembersrt:MinimumMember2025-12-310000003570us-gaap:LetterOfCreditMemberlng:SPLRevolvingCreditFacilityMembersrt:MaximumMember2025-12-310000003570us-gaap:LetterOfCreditMemberlng:CQPRevolvingCreditFacilityMembersrt:MinimumMember2025-12-310000003570us-gaap:LetterOfCreditMemberlng:CQPRevolvingCreditFacilityMembersrt:MaximumMember2025-12-310000003570us-gaap:LetterOfCreditMemberlng:CorpusChristiHoldingsWorkingCapitalFacilityMembersrt:MinimumMember2025-12-310000003570us-gaap:LetterOfCreditMemberlng:CorpusChristiHoldingsWorkingCapitalFacilityMembersrt:MaximumMember2025-12-310000003570us-gaap:LetterOfCreditMemberlng:CheniereRevolvingCreditFacilityMembersrt:MinimumMember2025-12-310000003570us-gaap:LetterOfCreditMemberlng:CheniereRevolvingCreditFacilityMembersrt:MaximumMember2025-12-310000003570lng:SPLRevolvingCreditFacilityMember2025-01-012025-12-310000003570lng:CQPRevolvingCreditFacilityMember2025-01-012025-12-310000003570lng:CorpusChristiHoldingsWorkingCapitalFacilityMember2025-01-012025-12-310000003570lng:CheniereRevolvingCreditFacilityMember2025-01-012025-12-310000003570lng:A2015CCHTermLoanFacilityMembersrt:MaximumMember2025-01-012025-12-310000003570lng:SabinePassLiquefactionAndCheniereCorpusChristiHoldingsMember2025-01-012025-12-310000003570us-gaap:CarryingReportedAmountFairValueDisclosureMemberlng:FairValueInputsLevel2AndLevel3Memberus-gaap:SeniorNotesMember2025-12-310000003570us-gaap:EstimateOfFairValueFairValueDisclosureMemberlng:FairValueInputsLevel2AndLevel3Memberus-gaap:SeniorNotesMember2025-12-310000003570us-gaap:CarryingReportedAmountFairValueDisclosureMemberlng:FairValueInputsLevel2AndLevel3Memberus-gaap:SeniorNotesMember2024-12-310000003570us-gaap:EstimateOfFairValueFairValueDisclosureMemberlng:FairValueInputsLevel2AndLevel3Memberus-gaap:SeniorNotesMember2024-12-310000003570us-gaap:EstimateOfFairValueFairValueDisclosureMemberus-gaap:FairValueInputsLevel3Memberus-gaap:SeniorNotesMember2025-12-310000003570us-gaap:EstimateOfFairValueFairValueDisclosureMemberus-gaap:FairValueInputsLevel3Memberus-gaap:SeniorNotesMember2024-12-310000003570us-gaap:OperatingExpenseMember2025-01-012025-12-310000003570us-gaap:OperatingExpenseMember2024-01-012024-12-310000003570us-gaap:OperatingExpenseMember2023-01-012023-12-310000003570lng:DepreciationandAmortizationExpenseMember2025-01-012025-12-310000003570lng:DepreciationandAmortizationExpenseMember2024-01-012024-12-310000003570lng:DepreciationandAmortizationExpenseMember2023-01-012023-12-310000003570us-gaap:InterestExpenseMember2025-01-012025-12-310000003570us-gaap:InterestExpenseMember2024-01-012024-12-310000003570us-gaap:InterestExpenseMember2023-01-012023-12-310000003570us-gaap:OperatingLeaseLeaseNotYetCommencedMember2025-12-310000003570srt:MaximumMember2025-12-310000003570lng:LiquefiedNaturalGasProcuredFromThirdPartiesMember2025-01-012025-12-310000003570lng:LiquefiedNaturalGasProcuredFromThirdPartiesMember2024-01-012024-12-310000003570lng:LiquefiedNaturalGasProcuredFromThirdPartiesMember2023-01-012023-12-310000003570lng:TotalEnergiesGasPowerNorthAmericaIncMember2025-01-012025-12-310000003570lng:SabinePassLiquefactionMember2025-01-012025-12-310000003570lng:TerminalUseAgreementRegasificationCapacityPartialMember2025-01-012025-12-310000003570lng:TerminalUseAgreementRegasificationCapacityPartialMember2024-01-012024-12-310000003570lng:TerminalUseAgreementRegasificationCapacityPartialMember2023-01-012023-12-310000003570lng:LiquefiedNaturalGasMember2026-01-012025-12-310000003570lng:LiquefiedNaturalGasMember2025-01-012024-12-310000003570lng:RegasificationServiceMember2026-01-012025-12-310000003570lng:RegasificationServiceMember2025-01-012024-12-3100000035702026-01-012025-12-3100000035702025-01-012024-12-310000003570us-gaap:ProductAndServiceOtherMemberus-gaap:EquityMethodInvesteeMemberlng:OperationAgreementAndConstructionManagementAgreementMember2025-01-012025-12-310000003570us-gaap:ProductAndServiceOtherMemberus-gaap:EquityMethodInvesteeMemberlng:OperationAgreementAndConstructionManagementAgreementMember2024-01-012024-12-310000003570us-gaap:ProductAndServiceOtherMemberus-gaap:EquityMethodInvesteeMemberlng:OperationAgreementAndConstructionManagementAgreementMember2023-01-012023-12-310000003570lng:NaturalGasTransportationAndStorageAgreementsMemberus-gaap:EquityMethodInvesteeMember2025-01-012025-12-310000003570lng:NaturalGasTransportationAndStorageAgreementsMemberus-gaap:EquityMethodInvesteeMember2024-01-012024-12-310000003570lng:NaturalGasTransportationAndStorageAgreementsMemberus-gaap:EquityMethodInvesteeMember2023-01-012023-12-310000003570lng:NaturalGasTransportationAndStorageAgreementsMemberus-gaap:RelatedPartyMember2025-01-012025-12-310000003570lng:NaturalGasTransportationAndStorageAgreementsMemberus-gaap:RelatedPartyMember2024-01-012024-12-310000003570lng:NaturalGasTransportationAndStorageAgreementsMemberus-gaap:RelatedPartyMember2023-01-012023-12-310000003570us-gaap:ProductAndServiceOtherMemberlng:EquityMethodInvesteeSoldMemberlng:OperationAgreementAndConstructionManagementAgreementMember2025-01-012025-12-310000003570us-gaap:ProductAndServiceOtherMemberlng:EquityMethodInvesteeSoldMemberlng:OperationAgreementAndConstructionManagementAgreementMember2024-01-012024-12-310000003570us-gaap:ProductAndServiceOtherMemberlng:EquityMethodInvesteeSoldMemberlng:OperationAgreementAndConstructionManagementAgreementMember2023-01-012023-12-310000003570lng:NaturalGasTransportationAndStorageAgreementsMemberlng:EquityMethodInvesteeSoldMember2025-01-012025-12-310000003570lng:NaturalGasTransportationAndStorageAgreementsMemberlng:EquityMethodInvesteeSoldMember2024-01-012024-12-310000003570lng:NaturalGasTransportationAndStorageAgreementsMemberlng:EquityMethodInvesteeSoldMember2023-01-012023-12-310000003570us-gaap:RelatedPartyMember2025-12-310000003570us-gaap:RelatedPartyMember2024-12-310000003570us-gaap:DomesticCountryMember2025-12-310000003570us-gaap:StateAndLocalJurisdictionMember2025-12-3100000035702025-12-012025-12-310000003570country:GB2025-01-012025-12-310000003570us-gaap:ForeignTaxJurisdictionOtherMember2025-01-012025-12-310000003570srt:MaximumMemberus-gaap:RestrictedStockUnitsRSUMember2025-01-012025-12-310000003570us-gaap:PerformanceSharesMember2025-01-012025-12-310000003570srt:MinimumMemberus-gaap:PerformanceSharesMember2025-01-012025-12-310000003570srt:MaximumMemberus-gaap:PerformanceSharesMember2025-01-012025-12-310000003570lng:LiabilityAwardsMember2025-01-012025-12-310000003570lng:LiabilityAwardsMember2024-01-012024-12-310000003570lng:LiabilityAwardsMember2023-01-012023-12-310000003570lng:EquityAwardsMember2025-01-012025-12-310000003570lng:EquityAwardsMember2024-01-012024-12-310000003570lng:EquityAwardsMember2023-01-012023-12-310000003570lng:EquityClassifiedRestrictedStockUnitsMember2024-12-310000003570lng:LiabilityClassifiedRestrictedStockUnitsMember2024-12-310000003570lng:EquityClassifiedPerformanceStockUnitsMember2024-12-310000003570lng:LiabilityClassifiedPerformanceStockUnitsMember2024-12-310000003570lng:EquityClassifiedRestrictedStockUnitsMember2025-01-012025-12-310000003570lng:LiabilityClassifiedRestrictedStockUnitsMember2025-01-012025-12-310000003570lng:EquityClassifiedPerformanceStockUnitsMember2025-01-012025-12-310000003570lng:LiabilityClassifiedPerformanceStockUnitsMember2025-01-012025-12-310000003570lng:EquityClassifiedRestrictedStockUnitsMember2025-12-310000003570lng:LiabilityClassifiedRestrictedStockUnitsMember2025-12-310000003570lng:EquityClassifiedPerformanceStockUnitsMember2025-12-310000003570lng:LiabilityClassifiedPerformanceStockUnitsMember2025-12-310000003570us-gaap:RestrictedStockUnitsRSUMember2025-01-012025-12-310000003570us-gaap:PerformanceSharesMember2024-01-012024-12-310000003570us-gaap:PerformanceSharesMember2023-01-012023-12-310000003570us-gaap:SubsequentEventMember2026-01-272026-01-270000003570us-gaap:SubsequentEventMember2026-02-250000003570lng:CorpusChristiLiquefactionMemberlng:BechtelEPCContractCorpusChristiStage3Member2025-01-012025-12-310000003570lng:CorpusChristiLiquefactionMemberlng:BechtelEPCContractMidscale89Member2025-01-012025-12-310000003570lng:CorpusChristiLiquefactionMemberlng:BechtelEPCContractCorpusChristiStage3Member2025-12-310000003570lng:CorpusChristiLiquefactionMemberlng:BechtelEPCContractMidscale89Member2025-12-310000003570us-gaap:CustomerConcentrationRiskMemberus-gaap:SalesRevenueNetMember2025-01-012025-12-310000003570us-gaap:CustomerConcentrationRiskMemberus-gaap:SalesRevenueNetMember2024-01-012024-12-310000003570us-gaap:CustomerConcentrationRiskMemberus-gaap:SalesRevenueNetMember2023-01-012023-12-310000003570us-gaap:CustomerConcentrationRiskMemberlng:AccountsReceivableAndContractAssetsMember2025-01-012025-12-310000003570us-gaap:CustomerConcentrationRiskMemberlng:AccountsReceivableAndContractAssetsMember2024-01-012024-12-310000003570lng:MajorCustomerMemberus-gaap:CustomerConcentrationRiskMemberlng:AccountsReceivableAndContractAssetsMember2025-01-012025-12-310000003570lng:MajorCustomerMemberus-gaap:CustomerConcentrationRiskMemberlng:AccountsReceivableAndContractAssetsMember2024-01-012024-12-310000003570country:USus-gaap:GeographicConcentrationRiskMember2025-01-012025-12-310000003570country:USus-gaap:GeographicConcentrationRiskMember2024-01-012024-12-310000003570country:USus-gaap:GeographicConcentrationRiskMember2023-01-012023-12-310000003570country:SGus-gaap:GeographicConcentrationRiskMember2025-01-012025-12-310000003570country:SGus-gaap:GeographicConcentrationRiskMember2024-01-012024-12-310000003570country:SGus-gaap:GeographicConcentrationRiskMember2023-01-012023-12-310000003570country:GBus-gaap:GeographicConcentrationRiskMember2025-01-012025-12-310000003570country:GBus-gaap:GeographicConcentrationRiskMember2024-01-012024-12-310000003570country:GBus-gaap:GeographicConcentrationRiskMember2023-01-012023-12-310000003570lng:OtherCountriesMemberus-gaap:GeographicConcentrationRiskMember2025-01-012025-12-310000003570lng:OtherCountriesMemberus-gaap:GeographicConcentrationRiskMember2024-01-012024-12-310000003570lng:OtherCountriesMemberus-gaap:GeographicConcentrationRiskMember2023-01-012023-12-3100000035702025-10-012025-12-31

UNITED STATES

SECURITIES AND EXCHANGE COMMISSION

Washington, D.C. 20549

FORM 10-K

☒ ANNUAL REPORT PURSUANT TO SECTION 13 OR 15(d) OF THE SECURITIES EXCHANGE ACT OF 1934

For the fiscal year ended December 31, 2025

or

☐ TRANSITION REPORT PURSUANT TO SECTION 13 OR 15(d) OF THE SECURITIES EXCHANGE ACT OF 1934

For the transition period from to

Commission file number 001-16383

CHENIERE ENERGY, INC.

(Exact name of registrant as specified in its charter)

| | | | | |

| Delaware | 95-4352386 |

| (State or other jurisdiction of incorporation or organization) | (I.R.S. Employer Identification No.) |

845 Texas Avenue, Suite 1250

Houston, Texas 77002

(Address of principal executive offices) (Zip Code)

(713) 375-5000

(Registrant’s telephone number, including area code)

Securities registered pursuant to Section 12(b) of the Act:

| | | | | | | | |

| Title of each class | Trading Symbol | Name of each exchange on which registered |

| Common Stock, $ 0.003 par value | LNG | New York Stock Exchange |

Securities registered pursuant to Section 12(g) of the Act: None

Indicate by check mark if the registrant is a well-known seasoned issuer, as defined in Rule 405 of the Securities Act. Yes ☒ No ☐

Indicate by check mark if the registrant is not required to file reports pursuant to Section 13 or Section 15(d) of the Act. Yes ☐ No ☒

Indicate by check mark whether the registrant (1) has filed all reports required to be filed by Section 13 or 15(d) of the Securities Exchange Act of 1934 during the preceding 12 months (or for such shorter period that the registrant was required to file such reports), and (2) has been subject to such filing requirements for the past 90 days. Yes ☒ No ☐

Indicate by check mark whether the registrant has submitted electronically every Interactive Data File required to be submitted pursuant to Rule 405 of Regulation S-T (§232.405 of this chapter) during the preceding 12 months (or for such shorter period that the registrant was required to submit such files). Yes ☒ No ☐

Indicate by check mark whether the registrant is a large accelerated filer, an accelerated filer, a non-accelerated filer, a smaller reporting company, or an emerging growth company. See the definitions of “large accelerated filer,” “accelerated filer,” “smaller reporting company” and “emerging growth company” in Rule 12b-2 of the Exchange Act.

| | | | | | | | | | | | | | | | | |

| Large accelerated filer | ☒ | | Accelerated filer | ☐ |

| Non-accelerated filer | ☐ | | Smaller reporting company | ☐ |

| | | | Emerging growth company | ☐ |

If an emerging growth company, indicate by check mark if the registrant has elected not to use the extended transition period for complying with any new or revised financial accounting standards provided pursuant to Section 13(a) of the Exchange Act. ☐

Indicate by check mark whether the registrant has filed a report on and attestation to its management’s assessment of the effectiveness of its internal control over financial reporting under Section 404(b) of the Sarbanes-Oxley Act (15 U.S.C. 7262(b)) by the registered public accounting firm that prepared or issued its audit report. ☒

If securities are registered pursuant to Section 12(b) of the Act, indicate by check mark whether the financial statements of the registrant included in the filing reflect the correction of an error to previously issued financial statements. ☐

Indicate by check mark whether any of those error corrections are restatements that required a recovery analysis of incentive-based compensation received by any of the registrant’s executive officers during the relevant recovery period pursuant to §240.10D-1(b). ☐

Indicate by check mark whether the registrant is a shell company (as defined in Rule 12b-2 of the Exchange Act). Yes ☐ No ☒

The aggregate market value of the registrant’s Common Stock held by non-affiliates of the registrant was approximately $53.6 billion as of June 30, 2025.

As of February 20, 2026, the issuer had 210,202,883 shares of Common Stock outstanding.

Documents incorporated by reference: The definitive proxy statement for the registrant’s Annual Meeting of Stockholders (to be filed within 120 days of the close of the registrant’s fiscal year) is incorporated by reference into Part III.

CHENIERE ENERGY, INC.

TABLE OF CONTENTS

DEFINITIONS

As used in this annual report, the terms listed below have the following meanings:

Common Industry and Other Terms

| | | | | | | | |

| ASU | | Accounting Standards Update |

| | |

| | |

| Bcf/d | | billion cubic feet per day |

| Bcf/yr | | billion cubic feet per year |

| Bcfe | | billion cubic feet equivalent |

| CAMT | | corporate alternative minimum tax |

| DAP | | delivered at place, which requires the buyer to take delivery at one or more designated receiving terminals |

| DOE | | U.S. Department of Energy |

| EPC | | engineering, procurement and construction |

| | |

| FASB | | Financial Accounting Standards Board |

| FERC | | Federal Energy Regulatory Commission |

| FID | | final investment decision |

| FOB | | free-on-board, which requires the buyer to take delivery at seller's export terminal |

| FTA countries | | countries with which the U.S. has a free trade agreement providing for national treatment for trade in natural gas |

| GAAP | | generally accepted accounting principles in the U.S. |

| Henry Hub | | the final settlement price (in U.S. dollars per MMBtu) for the New York Mercantile Exchange’s Henry Hub natural gas futures contract for the month in which a relevant cargo’s delivery window is scheduled to begin |

| International Climate Change-Related Policies | | value-chain accountability and sectoral decarbonization standards, including EU Methane Emissions Regulation, FuelEU Maritime Regulation, International Maritime Organization's Net Zero Framework and Corporate Sustainability Due Diligence Directive |

| IPM agreements | | integrated production marketing agreements in which the gas producer sells to us gas on a global LNG or natural gas index price, less a fixed liquefaction fee, shipping and other costs |

| LNG | | liquefied natural gas, a product of natural gas that, through a refrigeration process, has been cooled to a liquid state, which occupies a volume that is approximately 1/600th of its gaseous state |

| MMBtu | | million British thermal units; one British thermal unit measures the amount of energy required to raise the temperature of one pound of water by one degree Fahrenheit |

| mtpa | | million tonnes per annum |

| NGA | | Natural Gas Act of 1938, as amended |

| NCI | | non-controlling interests |

| non-FTA countries | | countries with which the U.S. does not have a free trade agreement providing for national treatment for trade in natural gas and with which trade is permitted |

| | |

| SEC | | U.S. Securities and Exchange Commission |

| SOFR | | Secured Overnight Financing Rate |

| SPA | | LNG sale and purchase agreement |

| TBtu | | trillion British thermal units; one British thermal unit measures the amount of energy required to raise the temperature of one pound of water by one degree Fahrenheit |

| Tcf | | trillion cubic feet |

| Train | | an industrial facility comprised of a series of refrigerant compressor loops used to cool natural gas into LNG |

| TUA | | terminal use agreement |

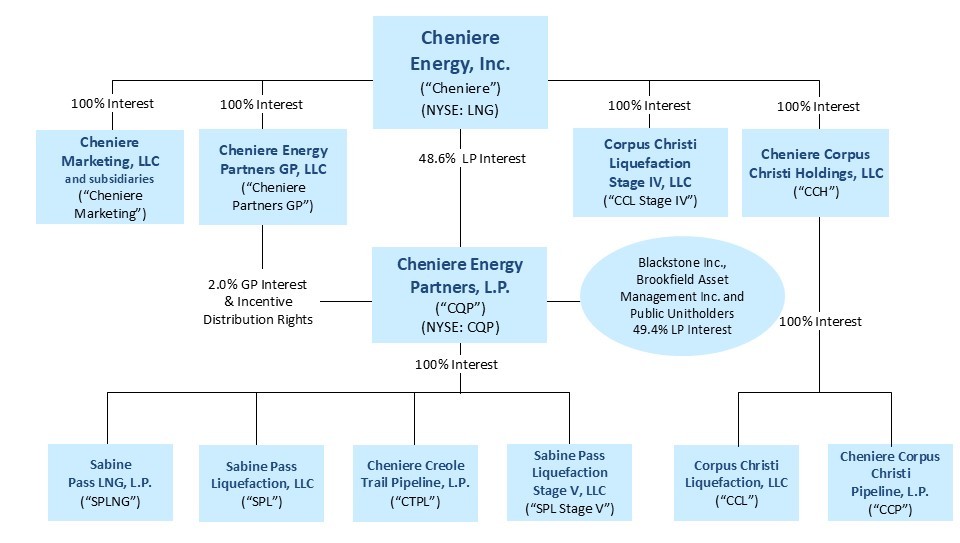

Abbreviated Legal Entity Structure

The following diagram depicts our abbreviated legal entity structure as of December 31, 2025, including our ownership of certain subsidiaries, and the references to these entities used in this annual report:

Unless the context requires otherwise, references to the “Company,” “we,” “us” and “our” refer to Cheniere Energy, Inc. and its consolidated subsidiaries, including our publicly traded subsidiary, CQP.

CAUTIONARY STATEMENT

REGARDING FORWARD-LOOKING STATEMENTS

This annual report contains certain statements that are, or may be deemed to be, “forward-looking statements” within the meaning of Section 27A of the Securities Act of 1933, as amended (the “Securities Act”), and Section 21E of the Securities Exchange Act of 1934, as amended (the “Exchange Act”). All statements, other than statements of historical or present facts or conditions, included herein or incorporated herein by reference are “forward-looking statements.” Included among “forward-looking statements” are, among other things:

•statements that we expect to commence or complete construction of our proposed LNG terminals, liquefaction facilities, pipeline facilities or other projects, or any expansions or portions thereof, by certain dates, or at all;

•statements regarding future levels of domestic and international natural gas production, supply or consumption or future levels of LNG imports into or exports from North America and other countries worldwide or purchases of natural gas, regardless of the source of such information, or the transportation or other infrastructure or demand for and prices related to natural gas, LNG or other hydrocarbon products;

•statements regarding any financing transactions or arrangements, or our ability to enter into such transactions;

•statements relating to Cheniere’s capital deployment, including intent, ability, extent and timing of capital expenditures, debt repayment, dividends, share repurchases and execution on the capital allocation plan;

•statements regarding our future sources of liquidity and cash requirements;

•statements relating to the construction of our Trains and pipelines, including statements concerning the engagement of any EPC contractor or other contractor and the anticipated terms and provisions of any agreement with any EPC or other contractor, and anticipated costs related thereto;

•statements regarding any SPA or other agreement to be entered into or performed substantially in the future, including any revenues anticipated to be received and the anticipated timing thereof, and statements regarding the amounts of total LNG regasification, natural gas liquefaction or storage capacities that are, or may become, subject to contracts;

•statements regarding counterparties to our commercial contracts, construction contracts and other contracts;

•statements regarding our planned development and construction of additional Trains or pipelines, including the financing of such Trains or pipelines;

•statements that our Trains, when completed, will have certain characteristics, including amounts of liquefaction capacities;

•statements regarding our business strategy, our strengths, our business and operation plans or any other plans, forecasts, projections, or objectives, including anticipated revenues, capital expenditures, maintenance and operating costs and cash flows, any or all of which are subject to change;

•statements relating to our goals, commitments and strategies in relation to environmental matters;

•statements regarding legislative, governmental, regulatory, administrative or other public body actions, approvals, requirements, permits, applications, filings, investigations, proceedings or decisions;

•statements regarding our anticipated LNG and natural gas marketing activities;

•any other statements that relate to non-historical or future information; and

All of these types of statements, other than statements of historical or present facts or conditions, are forward-looking statements. In some cases, forward-looking statements can be identified by terminology such as “may,” “will,” “could,” “should,” “achieve,” “anticipate,” “believe,” “contemplate,” “continue,” “estimate,” “expect,” “intend,” “plan,” “potential,” “predict,” “project,” “pursue,” “target,” the negative of such terms or other comparable terminology. The forward-looking statements contained in this annual report are largely based on our expectations, which reflect estimates and assumptions made by our management. These estimates and assumptions reflect our best judgment based on currently known market conditions and other factors. Although we believe that such estimates are reasonable, they are inherently uncertain and involve a number of risks and uncertainties beyond our control. In addition, assumptions may prove to be inaccurate. We caution that the forward-looking statements contained in this annual report are not guarantees of future performance and that such statements may not be realized or the forward-looking statements or events may not occur. Actual results may differ materially from those anticipated or implied in forward-looking statements as a result of a variety of factors described in this annual report and in the other reports and other information that we file with the SEC. All forward-looking statements attributable to us or persons acting on our behalf are expressly qualified in their entirety by these risk factors. These forward-looking statements speak only as of the

CAUTIONARY STATEMENT

REGARDING FORWARD-LOOKING STATEMENTS

date made, and other than as required by law, we undertake no obligation to update or revise any forward-looking statement or provide reasons why actual results may differ, whether as a result of new information, future events or otherwise.

PART I

ITEMS 1. AND 2. BUSINESS AND PROPERTIES

General

Cheniere, a Delaware corporation, is a Houston-based energy infrastructure company primarily engaged in LNG-related businesses. We provide clean, secure and affordable LNG to integrated energy companies, utilities and energy trading companies around the world. We aspire to conduct our business in a safe and responsible manner, delivering a reliable, competitive and integrated source of LNG to our customers.

LNG is natural gas (primarily methane) in liquid form and is a cleaner dispatchable fuel for power generation. The LNG we produce is shipped all over the world, converted back into natural gas (called “regasification”) and then transported via pipeline to homes and businesses and used as an energy source that is essential for heating, cooking and other industrial uses.

As of December 31, 2025, we were the largest producer of LNG in the U.S. and the second largest LNG operator globally, based on the total production capacity of our natural gas liquefaction facilities. Our total production capacity is expected to be over 60 mtpa of LNG, inclusive of estimated debottlenecking opportunities, of which over 9 mtpa was under construction and the remainder was in operation as of December 31, 2025, comprised of the following:

•over 30 mtpa of total production capacity in operation from natural gas liquefaction facilities located in Cameron Parish, Louisiana at Sabine Pass (the “SPL Project”). We own and operate the SPL Project and export facility (the “Sabine Pass LNG Terminal”), one of the largest LNG production facilities in the world, through our ownership interest in and management agreements with CQP, which is a publicly traded limited partnership. As of December 31, 2025, we owned 100% of the general partner interest, a 48.6% limited partner interest and 100% of the incentive distribution rights of CQP. The Sabine Pass LNG Terminal also has five LNG storage tanks with aggregate capacity of approximately 17 Bcfe and vaporizers with regasification capacity of approximately 4 Bcf/d, as well as three marine berths, two of which can accommodate vessels with nominal capacity of up to 266,000 cubic meters and the third berth, which can accommodate vessels with nominal capacity of up to 200,000 cubic meters. We also own and operate through CQP a 94-mile natural gas supply pipeline that interconnects the Sabine Pass LNG Terminal with several large interstate and intrastate pipelines (the “Creole Trail Pipeline”).

•over 30 mtpa of total expected production capacity, inclusive of estimated debottlenecking opportunities, including over 9 mtpa under construction and the remainder in operation as of December 31, 2025, from our natural gas liquefaction and export facility located near Corpus Christi, Texas (the “Corpus Christi LNG Terminal”), of which we have 100% ownership interest. The Corpus Christi LNG Terminal also has three LNG storage tanks with aggregate capacity of approximately 10 Bcfe and two marine berths that can each accommodate vessels with nominal capacity of up to 266,000 cubic meters. We also own and operate through CCP an approximately 21-mile natural gas supply pipeline that interconnects the Corpus Christi LNG Terminal with several large interstate and intrastate natural gas pipelines (the “Corpus Christi Pipeline”). The projects under construction at the Corpus Christi LNG Terminal include:

◦a project consisting of seven midscale Trains that is expected to add total production capacity of over 10 mtpa of LNG once fully completed (the “Corpus Christi Stage 3 Project”), with over 4 mtpa under construction and the remainder in operation from the first four midscale Trains that have reached substantial completion as of December 31, 2025; and

◦a project consisting of two additional midscale Trains that is expected to add total production capacity of approximately 5 mtpa of LNG once fully completed, inclusive of estimated debottlenecking opportunities (the “CCL Midscale Trains 8 & 9 Project” and together with the existing assets at the Corpus Christi LNG Terminal, the Corpus Christi Stage 3 Project and the Corpus Christi Pipeline, the “CCL Project”), which was under construction as of December 31, 2025. Our board of directors (our “Board”) made a positive FID with respect to the CCL Midscale Trains 8 & 9 Project on June 17, 2025, and issued a full notice to proceed with construction to Bechtel Energy Inc. (“Bechtel”) effective June 18, 2025. Non-FTA export authorization on the CCL Midscale Trains 8 & 9 Project is pending with the DOE.

Our long-term counterparty arrangements form the foundation of our business and provide us with significant, stable, long-term cash flows, and include SPAs, in which our customers are generally required to pay a fixed fee with respect to the

contracted volumes irrespective of their election to cancel or suspend deliveries of LNG cargoes, and IPM agreements, in which a gas producer sells natural gas to us on a global LNG or natural gas index price, less a fixed liquefaction fee, shipping and other costs. The SPAs also have a variable fee component, which is primarily indexed to Henry Hub and generally structured to cover the cost of natural gas purchases, transportation and liquefaction fuel consumed to produce LNG. Since we procure most of our feedstock for LNG production from the U.S., the structure of these contracts helps limit our exposure to fluctuations in U.S. natural gas prices. Through our SPAs and IPM agreements currently in effect, with approximately 15 years of weighted average remaining life as of December 31, 2025, we have contracted approximately 90% of the total anticipated production from the SPL Project and the CCL Project (collectively, the “Liquefaction Projects”) through the mid-2030s, excluding volumes from contracts with terms less than 10 years and volumes from SPAs that are conditional on additional liquefaction capacity beyond what is currently in construction or operation, subject to unilateral waiver by us. LNG produced by the Liquefaction Projects that is not contracted under long-term contracts is available for Cheniere Marketing, our integrated marketing function, to sell in the global market under spot sales or other short-term agreements.

Disciplined Accretive Growth

We remain focused on safety, operational excellence and customer satisfaction. Increasing demand for LNG has allowed us to expand our liquefaction infrastructure in a financially disciplined manner. Our capital allocation plan is designed, in part, to invest in financially disciplined growth accretive to our common stock. Capital investment parameters are the foundation of our disciplined, accretive growth, and include consideration to:

•Achieve value accretive returns through long-term commercial contracts: We aim to contract approximately 90% of our current and planned liquefaction capacity under long-term SPAs and IPM agreements with creditworthy counterparties under the pricing structures described above, with financial parameters that consider, among other things, targeted unlevered returns that exceed our cost of equity and return on stock at prevailing stock prices and project leverage. Our success in securing long-term commercial contracts at desired returns is influenced by global LNG and natural gas market conditions and other uncertainties described in Item 1A. Risk Factors. •Achieve credit accretive returns: We aim to conservatively fund our projects through financing structures that sustain our long-term, run-rate leverage and credit metrics. Our ability to secure the required financing is influenced by market interest rates and other factors described in Item 1A. Risk Factors.

We have increased available liquefaction capacity at our Liquefaction Projects as a result of debottlenecking and other optimization projects. We believe these factors provide a foundation for additional growth in our portfolio of customer contracts in the future. We hold significant land positions at both the Sabine Pass LNG Terminal and the Corpus Christi LNG Terminal, which provide opportunity for further liquefaction capacity expansion. We are developing a two-phased expansion adjacent to the SPL Project, inclusive of three liquefaction trains and supporting infrastructure, with an expected total peak production capacity of up to approximately 20 mtpa of LNG, inclusive of estimated debottlenecking opportunities (the “SPL Expansion Project”). Following our pre-filing in July 2025, in February 2026, we filed an application with the FERC under the NGA for authorization to site, construct and operate a further expansion of the CCL Project in a phased approach, inclusive of four liquefaction trains and supporting infrastructure, with an expected total peak production capacity of up to 24 mtpa of LNG, inclusive of estimated debottlenecking opportunities (the “CCL Expansion Project”). These projects and any future expansions at our sites require, among other things, regulatory approvals and acceptable commercial and financing arrangements before we make a positive FID. Risks associated with cost overruns and delays in the completion of our expansion projects are described in Item 1A. Risk Factors.

The following table summarizes pre-FID development efforts and certain key milestones associated with the SPL Expansion Project and the CCL Expansion Project:

| | | | | | | | | | | | | | | | | | | |

| | | | | SPL Expansion Project | | CCL Expansion Project |

| Expected total peak production capacity of LNG (1) | | | | Up to ~ 20 mtpa | | Up to 24 mtpa |

| | | | | | | |

| Milestone | | | | | | |

| Regulatory (2) | FERC authorizations: | | | | | | |

| Positive environmental assessment | | | | Pending | | Pending |

| Order under Section 3 of NGA | | | | Pending | | Pending |

| Certification to commence construction | | | | Pending | | |

| DOE export authorization: | | | | | | |

| FTA countries | | | | ü | | |

| Non-FTA countries | | | | Pending | | |

| | | | | | | |

| Financing | Financing | | | | (3) | | (3) |

| | | | | | | |

| Commercialization and Other Contracting | Definitive commercial agreements | | | | (4) | | (4) |

| Definitive full-scope EPC contract | | | | | | |

| | | | | | | |

| Target Milestone | FID (5) | | | | 2026/2027 | | 2027/2028 |

ü indicates receipt of authorization, subject to ongoing conditionality

(1)Anticipated based on capacity, scale, location and infrastructure. Subject to regulatory review and approval and may change based on design considerations, engagement with contractors and other factors. Subject to adjustment for planned maintenance, production reliability, potential overdesign and debottlenecking opportunities.

(2)Our activities, including our expansion activities, are highly regulated and require regulatory approvals at various stages, including approvals of the FERC and DOE under Sections 3 and 7 of the NGA, as well as several other material governmental and regulatory approvals and permits. The progression of our expansion projects is dependent on receiving all regulatory approvals required within the respective stages. See Item 1A. Risk Factors for further discussion of the regulations under federal, state and local statutes, rules, regulations and laws to which we are subject and associated risk factors relating to regulations. (3)We anticipate drawing on current committed facilities and/or incurring additional debt to finance the construction of this expansion project if we reach a positive FID.

(4)Liquefaction capacity partially contracted by Cheniere Marketing, through SPAs that are conditioned on additional liquefaction capacity beyond what is currently in construction or operation and may be available to be novated to SPL or CCL, and by SPL Stage V, through an IPM agreement.

(5)Expected to be subject to phased FID. Any positive FID is subject to achievement of or consideration to relevant milestones and capital investment parameters described herein.

Our Business Strategy

Our primary business strategy is to be a full-service LNG provider to worldwide end-use customers. We accomplish this objective by owning, constructing and operating LNG and natural gas infrastructure facilities to meet our long-term customers’ energy demands and:

•safely, efficiently and reliably operating and maintaining our assets;

•procuring natural gas and pipeline transport capacity to our facilities;

•commencing commercial delivery for, and continuing to fulfill all commercial commitments to, our long-term SPA customers;

•providing value to our customers through destination flexibility, options not to lift cargoes and diversity of price and geography;

•continuing to secure long-term customer contracts to support our planned expansion, including the FID of potential expansion projects beyond the Corpus Christi Stage 3 Project and CCL Midscale Trains 8 & 9 Project;

•completing our construction projects safely, on-time and on-budget;

•maximizing the production of LNG to serve our customers and generating steady and stable revenues and operating cash flows;

•maintaining a flexible capital structure to finance the acquisition, development, construction and operation of the energy assets needed to supply our customers;

•executing our “all of the above” capital allocation strategy, focused on strengthening our balance sheet, funding financially disciplined growth and returning capital to our stockholders; and

•strategically identifying actionable and economic environmental solutions.

Our Business

We shipped our first LNG cargo in February 2016 and as of February 20, 2026, over 4,610 cumulative LNG cargoes totaling over 315 million tonnes of LNG have been produced, loaded and exported from the Liquefaction Projects. Our LNG has been shipped to over 40 countries and regions around the world.

Below is a discussion of our operations. For further discussion of our contractual obligations and cash requirements related to these operations, refer to Liquidity and Capital Resources in Item 7. Management’s Discussion and Analysis of Financial Condition and Results of Operations.

Sabine Pass LNG Terminal

Liquefaction Facilities and Expansion Project

The Sabine Pass LNG Terminal, as described above under the caption General, is one of the largest LNG production facilities in the world with over 30 mtpa of total production capacity, five storage tanks and three marine berths.

The following summarizes the volumes of natural gas for which we have received approvals from the FERC to site, construct and operate the Trains at the SPL Project and the orders we have received from the DOE authorizing the export of domestically produced LNG by vessel from the Sabine Pass LNG Terminal through December 31, 2050:

| | | | | | | | | | | | | | | | | | | | | | | |

| FERC Approved Volume | | DOE Approved Volume |

| (in Bcf/yr) | | (in mtpa) | | (in Bcf/yr) | | (in mtpa) |

| FTA countries (1) | 1,661.94 | | 33 | | 1,661.94 | | 33 |

| Non-FTA countries | 1,661.94 | | 33 | | 1,661.94 | | 33 |

(1)Excludes 950 Bcf/yr to FTA countries authorized in November 2025 for the SPL Expansion Project that is effective for 25 years from the date of first commercial export from the SPL Expansion Project.

In addition, we are developing the SPL Expansion Project, as also described above under the caption General. In June 2025, certain subsidiaries of CQP updated the SPL Expansion Project’s FERC application, originally filed in February 2024, to reflect a two-phased project, inclusive of three liquefaction trains and supporting infrastructure, maintaining an expected total peak production capacity of up to approximately 20 mtpa of LNG, inclusive of estimated debottlenecking opportunities.

Natural Gas Supply, Transportation and Storage

SPL has secured a portion of its expected natural gas feedstock for the SPL Project through long-term natural gas supply agreements, including an IPM agreement. SPL Stage V also has an IPM agreement to supply the SPL Expansion Project. Additionally, to ensure that SPL is able to transport and manage the natural gas feedstock to the Sabine Pass LNG Terminal, it

has transportation precedent and other agreements to secure firm pipeline transportation and storage capacity from third parties and CTPL.

Regasification Facilities

The Sabine Pass LNG Terminal, as described above under the caption General, has operational regasification capacity of approximately 4 Bcf/d and aggregate LNG storage capacity of approximately 17 Bcfe. SPLNG has a long-term, third party TUA for 1 Bcf/d with TotalEnergies Gas & Power North America, Inc. (“TotalEnergies”), under which TotalEnergies is required to pay fixed monthly fees, whether or not it uses the regasification capacity it has reserved. Approximately 2 Bcf/d of the remaining capacity has been reserved under a TUA by SPL, which also has a partial TUA assignment agreement with TotalEnergies, as further described in Note 12—Revenues of our Notes to Consolidated Financial Statements.

Corpus Christi LNG Terminal

Liquefaction Facilities and Expansion Projects

The Corpus Christi LNG Terminal, as described above under the caption General, has over 30 mtpa of total expected production capacity, inclusive of estimated debottlenecking opportunities, including over 4 mtpa under construction from the Corpus Christi Stage 3 Project, approximately 5 mtpa under construction from the CCL Midscale Trains 8 & 9 Project and the remainder in operation as of December 31, 2025. The Corpus Christi LNG Terminal also includes three storage tanks and two marine berths.

The following table summarizes the project completion and construction status of the Corpus Christi Stage 3 Project and CCL Midscale Trains 8 & 9 Project as of December 31, 2025:

| | | | | | | | | | | |

| Corpus Christi Stage 3 Project | | CCL Midscale Trains 8 & 9 Project |

| Overall project completion percentage | 94.1% | | 31.8% |

| Completion percentage of: | | | |

| Engineering | 99.6% | | 75.5% |

| Procurement | 100.0% | | 47.3% |

| Subcontract work | 95.1% | | 29.0% |

| Construction | 84.7% | | 0.2% |

| Date of expected substantial completion | 1H 2026 - 2H 2026 | | 2H 2028 |

The following summarizes the volumes of natural gas for which we have received approvals from the FERC to site, construct and operate the Trains at the CCL Project and the orders we have received from the DOE authorizing the export of domestically produced LNG by vessel from the Corpus Christi LNG Terminal through December 31, 2050:

| | | | | | | | | | | | | | | | | | | | | | | |

| FERC Approved Volume (1) | | DOE Approved Volume (1) |

| (in Bcf/yr) | | (in mtpa) | | (in Bcf/yr) | | (in mtpa) |

| Trains 1 through 3 of the CCL Project: | | | | | | | |

| FTA countries | 875.16 | | 17 | | 875.16 | | 17 |

| Non-FTA countries | 875.16 | | 17 | | 875.16 | | 17 |

| Corpus Christi Stage 3 Project: | | | | | | | |

| FTA countries | 582.14 | | 11.45 | | 582.14 | | 11.45 |

| Non-FTA countries | 582.14 | | 11.45 | | 582.14 | | 11.45 |

(1)Excludes 170 Bcf/yr to FTA countries authorized in July 2023 for the CCL Midscale Trains 8 & 9 Project that is not effective until the date of first commercial export from the CCL Midscale Trains 8 & 9 Project, which was approved by the FERC in March 2025.

In addition, we are developing the CCL Expansion Project, as also described above under the caption General, inclusive of four liquefaction trains and supporting infrastructure, with an expected total peak production capacity of up to 24 mtpa of LNG, inclusive of estimated debottlenecking opportunities.

Natural Gas Supply, Transportation and Storage

CCL has secured a portion of its expected natural gas feedstock for the Corpus Christi LNG Terminal through long-term natural gas supply agreements, including IPM agreements. Additionally, to ensure that CCL is able to transport and manage the natural gas feedstock to the Corpus Christi LNG Terminal, it has transportation precedent and other agreements to secure firm pipeline transportation and storage capacity from third parties and CCP.

Marketing

LNG produced by the Liquefaction Projects that is not contracted under long-term contracts is available for Cheniere Marketing, our integrated marketing function, to sell in the global market under spot sales or other short-term agreements. These volumes may be supplemented by volumes procured from third parties at other locations worldwide to support operational requirements or take advantage of market opportunities.

Additional information regarding our marketing activities can be found in Liquidity and Capital Resources in Item 7. Management’s Discussion and Analysis of Financial Condition and Results of Operations.

Major Customers

We did not have any customers accounting for 10% or more of total consolidated revenues from contracts with external customers for the year ended December 31, 2025.

Business Seasonality

Our results are affected by production levels, timing of our maintenance activities and the resulting availability of volumes. Therefore, operating profit may not be generated evenly throughout the year. Weather variations, including temperature, have an impact on LNG output at our Liquefaction Projects. Our Liquefaction Projects are capable of relatively higher production volumes during the cooler months as compared to the summer months. We typically perform our scheduled major maintenance activities at our sites during shoulder months in the second and third quarters in order to mitigate the impact to our annual operating results.

Governmental Regulation

Our LNG terminals and pipelines are subject to extensive regulation under federal, state and local statutes, rules, regulations and laws. These laws require that we engage in consultations with appropriate federal and state agencies and that we obtain and maintain applicable permits and other authorizations. As further described in Risks Relating to Regulations within Item 1A. Risk Factors, these rigorous regulatory requirements are built into the cost of construction and operation, and failure to comply with such laws could result in substantial penalties and/or loss of necessary authorizations.

Federal Energy Regulatory Commission

The design, construction, operation, maintenance and expansion of our liquefaction facilities and the transportation of natural gas in interstate commerce through our pipelines are highly regulated activities subject to the jurisdiction of the FERC pursuant to the NGA. Under the NGA, the FERC’s jurisdiction generally extends to the transportation of natural gas in interstate commerce, to the sale for resale of natural gas in interstate commerce, to natural gas companies engaged in such transportation or sale and to the construction, operation, maintenance and expansion of LNG terminals and interstate natural gas pipelines.

The FERC’s authority to regulate interstate natural gas pipelines and the services that they provide generally includes regulation of:

•rates and charges, and terms and conditions for natural gas transportation, storage and related services;

•the certification and construction of new facilities and modification of existing facilities;

•the extension and abandonment of services and facilities;

•the administration of accounting and financial reporting regulations, including the maintenance of accounts and records;

•the acquisition and abandonment of facilities; and

•various other matters.

Under the NGA, interstate pipelines are not permitted to unduly discriminate or grant undue preference as to rates or the terms and conditions of service to any shipper, including the company’s own affiliates. Those rates, terms and conditions must be public, and on file with the FERC. In contrast to pipeline regulation, the FERC does not require NGA Section 3 LNG terminal owners to provide open-access services at cost-based or regulated rates. Although the provisions that codified the FERC’s policy in this area expired on January 1, 2015, we see no indication that the FERC intends to change its policy in this area. On February 18, 2022, the FERC updated its 1999 Policy Statement on certification of new interstate natural gas facilities and the framework for the FERC’s decision-making process. On March 24, 2022, the FERC rescinded the Policy Statement and re-issued it as a draft. On September 12, 2025, the FERC issued an order terminating the proceeding to consider updates to the 1999 Policy Statement.

We are permitted to make sales of natural gas for resale in interstate commerce pursuant to a blanket marketing certificate granted by the FERC. Our sales of natural gas will be affected by the availability, terms and cost of pipeline transportation.

In order to site, construct and operate our LNG terminals, we received and are required to maintain authorizations from the FERC under Section 3 of the NGA as well as other material governmental and regulatory approvals and permits. The Energy Policy Act of 2005 (the “EPAct”) amended Section 3 of the NGA to establish or clarify the FERC’s exclusive authority to approve or deny an application for the siting, construction, expansion or operation of LNG terminals, unless specifically provided otherwise in the EPAct amendments to the NGA. For example, nothing in the EPAct amendments to the NGA were intended to affect otherwise applicable law related to any other federal agency’s authorities or responsibilities related to LNG terminals or those of a state acting under federal law.

In March 2025, we received authorization from the FERC under the NGA to site, construct and operate the CCL Midscale Trains 8 & 9 Project. In June 2025, certain subsidiaries of CQP updated the SPL Expansion Project’s FERC application, originally filed in February 2024, to reflect a two-phased project, inclusive of three liquefaction trains and supporting infrastructure, maintaining an expected total peak production capacity of up to approximately 20 mtpa of LNG, inclusive of estimated debottlenecking opportunities. In December 2025, we filed an application with the FERC to increase the LNG production capacity of the previously-authorized Corpus Christi Stage 3 Project and CCL Midscale Trains 8 & 9 Project by approximately 5 mtpa, which remains pending at the FERC. Following our pre-filing in July 2025, in February 2026, we filed an application with the FERC under the NGA for authorization to site, construct and operate the CCL Expansion Project in a phased approach, inclusive of four liquefaction trains and supporting infrastructure, with an expected total peak production capacity of up to 24 mtpa of LNG, inclusive of estimated debottlenecking opportunities.

The FERC’s Standards of Conduct apply to interstate pipelines that conduct transmission transactions with an affiliate that engages in natural gas marketing functions. The general principles of the FERC Standards of Conduct are: (1) non-discrimination, which requires transmission providers to treat all transmission customers, affiliated and non-affiliated, on a not unduly discriminatory basis, and to not make or grant any undue preference or advantage to any person or subject any person to any undue prejudice or disadvantage; (2) independent functioning, which requires transmission function employees to function independently of marketing function employees; (3) no-conduit rule, which prohibits passing transmission function information to marketing function employees; and (4) transparency, which imposes posting requirements to detect undue preference due to the improper disclosure of non-public transmission function information. We have established the required policies, procedures and training to comply with the FERC’s Standards of Conduct.

All of our FERC construction, operation, reporting, accounting and other regulated activities are subject to audit by the FERC, which may conduct routine or special inspections and issue data requests designed to ensure compliance with FERC rules, regulations, policies and procedures. The FERC’s jurisdiction under the NGA allows the imposition of civil and criminal

penalties for any violations of the NGA and any rules, regulations or orders of the FERC thereunder up to approximately $1.6 million per day per violation, including any conduct that violates the NGA’s prohibition against market manipulation.

Several other governmental and regulatory approvals and permits are required throughout the life of our LNG terminals and our pipelines. In addition, our FERC orders require us to comply with certain ongoing conditions and reporting obligations and maintain other regulatory agency approvals throughout the life of our facilities. For example, throughout the life of our LNG terminals and our pipelines, we are subject to regular reporting requirements to the FERC, the Department of Transportation’s (“DOT”) Pipeline and Hazardous Materials Safety Administration (“PHMSA”) and applicable federal and state regulatory agencies regarding the operation and maintenance of our facilities. To date, we have been able to obtain and maintain required approvals as needed, and the need for these approvals and reporting obligations has not materially affected our construction or operations.

DOE Export Licenses

The DOE has authorized the export of domestically produced LNG by vessel from the Sabine Pass LNG Terminal, as discussed in Sabine Pass LNG Terminal—Liquefaction Facilities, and the Corpus Christi LNG Terminal, as discussed in Corpus Christi LNG Terminal—Liquefaction Facilities. Although it is not expected to occur, the loss of an export authorization could be a force majeure event under our SPAs.

Under Section 3 of the NGA, applications for exports of natural gas (including LNG) to FTA countries, which allow for national treatment for trade in natural gas, are “deemed to be consistent with the public interest” and shall be granted by the DOE without “modification or delay.” FTA countries currently recognized by the DOE for exports of LNG include Australia, Bahrain, Canada, Chile, Colombia, Dominican Republic, El Salvador, Guatemala, Honduras, Jordan, Mexico, Morocco, Nicaragua, Oman, Panama, Peru, Republic of Korea and Singapore. FTAs with Israel and Costa Rica do not require national treatment for trade in natural gas. As part of its review of applications for export of LNG to non-FTA countries, the DOE publishes a Notice of Application in the Federal Register whereby the public and other interveners are provided the opportunity to comment and may assert that such authorization would not be consistent with the public interest. We currently have the SPL Expansion Project and the CCL Midscale Trains 8 & 9 Project pending non-FTA export approval with the DOE. However, the outstanding DOE approval for the SPL Expansion Project is first subject to the receipt of regulatory permit approval from the FERC, responsive to our formal application. In June 2025, certain subsidiaries of CQP updated the SPL Expansion Project’s application to the DOE for authorization to export LNG to FTA countries and non-FTA countries. In November 2025, the updated authorization to export LNG to FTA countries was received. See Sabine Pass LNG Terminal and Corpus Christi LNG Terminal sections above for FERC and DOE approved volumes on our existing Liquefaction Projects.

Pipeline and Hazardous Materials Safety Administration

Our LNG terminals as well as the Creole Trail Pipeline and the Corpus Christi Pipeline are subject to regulation by PHMSA. PHMSA is authorized by the applicable pipeline safety laws to establish minimum safety standards for certain pipelines and LNG facilities. The regulatory standards PHMSA has established are applicable to the design, installation, testing, construction, operation, maintenance and management of natural gas and hazardous liquid pipeline facilities and LNG facilities that affect interstate or foreign commerce. PHMSA has also established training, worker qualification and reporting requirements.

PHMSA performs inspections of pipeline and LNG facilities and has authority to undertake enforcement actions, including issuance of civil penalties up to approximately $273,000 per day per violation, with a maximum administrative civil penalty of approximately $2.7 million for any related series of violations.

Other Governmental Permits, Approvals and Authorizations