UNITED STATES

SECURITIES AND EXCHANGE COMMISSION

Washington, D.C. 20549

FORM 10-Q

x QUARTERLY REPORT PURSUANT TO SECTION 13 OR 15(d) OF THE SECURITIES EXCHANGE ACT OF 1934

For the quarterly period ended September 30, 2015

OR

¨ TRANSITION REPORT PURSUANT TO SECTION 13 OR 15(d) OF THE SECURITIES EXCHANGE ACT OF 1934

For the transition period from to

CHENIERE ENERGY, INC.

(Exact name of registrant as specified in its charter)

|

| | |

Delaware | 001-16383 | 95-4352386 |

(State or other jurisdiction of incorporation or organization) | (Commission File Number) | (I.R.S. Employer Identification No.) |

| | |

700 Milam Street, Suite 1900 | | |

Houston, Texas | | 77002 |

(Address of principal executive offices) | | (Zip code) |

(713) 375-5000

(Registrant’s telephone number, including area code)

Indicate by check mark whether the registrant (1) has filed all reports required to be filed by Section 13 or 15(d) of the Securities Exchange Act of 1934 during the preceding 12 months (or for such shorter period that the registrant was required to file such reports), and (2) has been subject to such filing requirements for the past 90 days. Yes x No ¨

Indicate by check mark whether the registrant has submitted electronically and posted on its corporate Web site, if any, every Interactive Data File required to be submitted and posted pursuant to Rule 405 of Regulation S-T (§232.405 of this chapter) during the preceding 12 months (or for such shorter period that the registrant was required to submit and post such files). Yes x No ¨

Indicate by check mark whether the registrant is a large accelerated filer, an accelerated filer, a non-accelerated filer, or a smaller reporting company. See the definitions of “large accelerated filer,” “accelerated filer” and “smaller reporting company” in Rule 12b-2 of the Exchange Act. (Check one):

|

| | | | | | |

Large accelerated filer x | Accelerated filer ¨ |

Non-accelerated filer ¨ | Smaller reporting company ¨ |

(Do not check if a smaller reporting company) |

Indicate by check mark whether the registrant is a shell company (as defined in Rule 12b-2 of the Exchange Act). Yes ¨ No x

As of October 20, 2015, the issuer had 236,032,655 shares of Common Stock outstanding.

CHENIERE ENERGY, INC.

TABLE OF CONTENTS

DEFINITIONS

As commonly used in the liquefied natural gas industry, to the extent applicable, and as used in this quarterly report, the terms listed below have the following meanings:

Common Industry and Other Terms

|

| | |

Bcf/d | | billion cubic feet per day |

Bcf/yr | | billion cubic feet per year |

Bcfe | | billion cubic feet equivalent |

DOE | | U.S. Department of Energy |

EPC | | engineering, procurement and construction |

FERC | | Federal Energy Regulatory Commission |

FTA countries | | countries with which the United States has a free trade agreement providing for national treatment for trade in natural gas |

GAAP | | generally accepted accounting principles in the United States |

Henry Hub | | the final settlement price (in USD per MMBtu) for the New York Mercantile Exchange’s Henry Hub natural gas futures contract for the month in which a relevant cargo’s delivery window is scheduled to begin |

LIBOR | | London Interbank Offered Rate |

LNG | | liquefied natural gas, a product of natural gas consisting primarily of methane (CH4) that is in liquid form at near atmospheric pressure |

MMBtu | | million British thermal units, an energy unit |

mtpa | | million tonnes per annum |

non-FTA countries | | countries without a free trade agreement providing for national treatment for trade in natural gas and with which trade is permitted |

SEC | | Securities and Exchange Commission |

SPA | | LNG sale and purchase agreement |

Train | | a refrigerant compressor train used in the industrial process to convert natural gas into LNG |

TUA | | terminal use agreement |

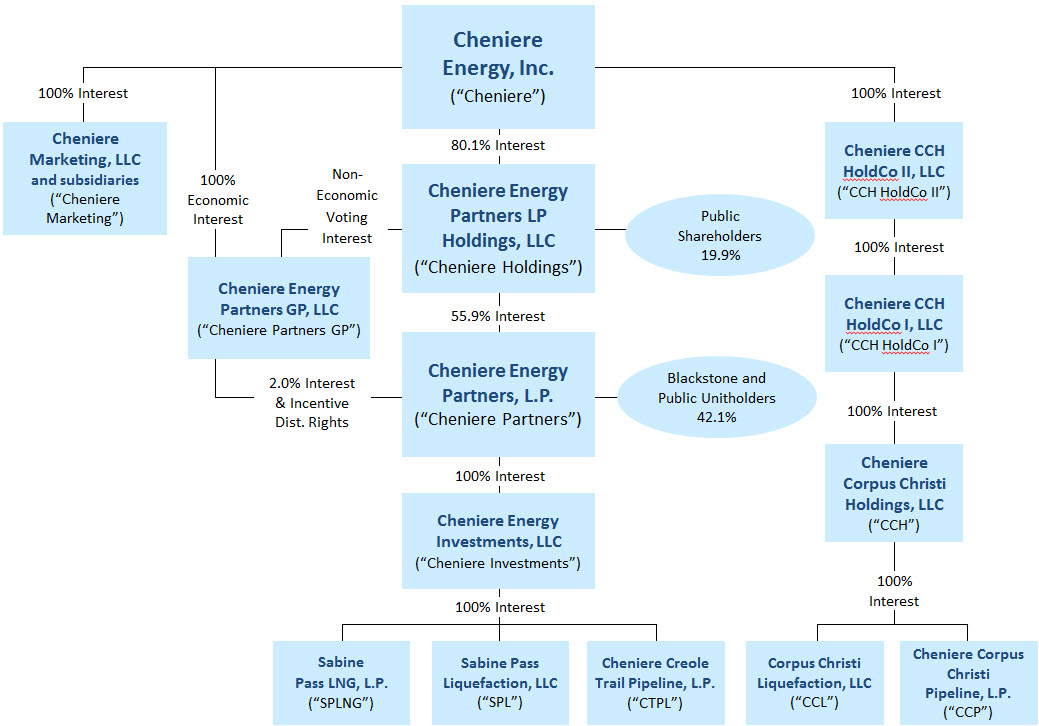

Abbreviated Organizational Structure

The following diagram depicts our abbreviated organizational structure as of September 30, 2015, including our ownership of certain subsidiaries, and the references to these entities used in this quarterly report:

Unless the context requires otherwise, references to “Cheniere,” the “Company,” “we,” “us” and “our” refer to Cheniere Energy, Inc. (NYSE MKT: LNG) and its consolidated subsidiaries, including our publicly traded subsidiaries, Cheniere Partners (NYSE MKT: CQP) and Cheniere Holdings (NYSE MKT: CQH).

PART I. FINANCIAL INFORMATION

ITEM 1. CONSOLIDATED FINANCIAL STATEMENTS

CHENIERE ENERGY, INC. AND SUBSIDIARIES

CONSOLIDATED BALANCE SHEETS

(in thousands, except share data)

|

| | | | | | | |

| September 30, | | December 31, |

| 2015 | | 2014 |

ASSETS | (unaudited) | | |

Current assets | | | |

Cash and cash equivalents | $ | 1,340,262 |

| | $ | 1,747,583 |

|

Restricted cash | 652,225 |

| | 481,737 |

|

Accounts and interest receivable | 6,645 |

| | 4,419 |

|

LNG inventory | 9,032 |

| | 4,294 |

|

Other current assets | 78,108 |

| | 20,844 |

|

Total current assets | 2,086,272 |

| | 2,258,877 |

|

| | | |

Non-current restricted cash | 118,909 |

| | 550,811 |

|

Property, plant and equipment, net | 15,225,250 |

| | 9,246,753 |

|

Debt issuance costs, net | 640,399 |

| | 242,323 |

|

Non-current derivative assets | 30,770 |

| | 11,744 |

|

Goodwill | 76,819 |

| | 76,819 |

|

Other non-current assets | 273,840 |

| | 186,356 |

|

Total assets | $ | 18,452,259 |

| | $ | 12,573,683 |

|

| | | |

LIABILITIES AND STOCKHOLDERS’ EQUITY | | | |

|

Current liabilities | | | |

|

Accounts payable | $ | 11,558 |

| | $ | 13,426 |

|

Accrued liabilities | 457,901 |

| | 169,129 |

|

Deferred revenue | 26,653 |

| | 26,655 |

|

Derivative liabilities | 33,839 |

| | 23,247 |

|

Other current liabilities | 268 |

| | 18 |

|

Total current liabilities | 530,219 |

| | 232,475 |

|

| | | |

Long-term debt, net | 15,835,910 |

| | 9,806,084 |

|

Non-current deferred revenue | 10,500 |

| | 13,500 |

|

Non-current derivative liabilities | 125,473 |

| | 267 |

|

Other non-current liabilities | 85,226 |

| | 19,840 |

|

| | | |

Commitments and contingencies (see Note 11) |

|

| |

|

|

| | | |

Stockholders’ equity |

|

| | |

|

Preferred stock, $0.0001 par value, 5.0 million shares authorized, none issued | — |

| | — |

|

Common stock, $0.003 par value | | | |

|

Authorized: 480.0 million shares at September 30, 2015 and December 31, 2014 | | | |

Issued and outstanding: 236.0 million shares and 236.7 million shares at September 30, 2015 and December 31, 2014, respectively | 708 |

| | 712 |

|

Treasury stock: 11.2 million shares and 10.6 million shares at September 30, 2015 and December 31, 2014, respectively, at cost | (337,057 | ) | | (292,752 | ) |

Additional paid-in-capital | 3,029,317 |

| | 2,776,702 |

|

Accumulated deficit | (3,332,851 | ) | | (2,648,839 | ) |

Total stockholders’ deficit | (639,883 | ) | | (164,177 | ) |

Non-controlling interest | 2,504,814 |

| | 2,665,694 |

|

Total equity | 1,864,931 |

| | 2,501,517 |

|

Total liabilities and equity | $ | 18,452,259 |

| | $ | 12,573,683 |

|

The accompanying notes are an integral part of these consolidated financial statements.

3

CHENIERE ENERGY, INC. AND SUBSIDIARIES

CONSOLIDATED STATEMENTS OF OPERATIONS

(in thousands, except per share data)

(unaudited)

|

| | | | | | | | | | | | | | | |

| Three Months Ended | | Nine Months Ended |

| September 30, | | September 30, |

| 2015 | | 2014 | | 2015 | | 2014 |

Revenues | | | | | | | |

LNG terminal revenues | $ | 67,212 |

| | $ | 66,983 |

| | $ | 202,698 |

| | $ | 200,243 |

|

Marketing and trading revenues (losses) | (1,557 | ) | | (499 | ) | | (1,601 | ) | | 482 |

|

Other | 404 |

| | 323 |

| | 1,356 |

| | 1,277 |

|

Total revenues | 66,059 |

| | 66,807 |

| | 202,453 |

| | 202,002 |

|

| | | | | | | |

Operating costs and expenses | | | | | | | |

Operating and maintenance expense (income) | (6,251 | ) | | 25,908 |

| | 49,319 |

| | 69,262 |

|

Depreciation expense | 21,638 |

| | 16,189 |

| | 59,561 |

| | 48,962 |

|

Development expense | 4,935 |

| | 11,544 |

| | 37,640 |

| | 38,919 |

|

General and administrative expense | 97,332 |

| | 74,255 |

| | 263,205 |

| | 215,783 |

|

Other | 479 |

| | 75 |

| | 920 |

| | 245 |

|

Total operating costs and expenses | 118,133 |

| | 127,971 |

| | 410,645 |

| | 373,171 |

|

| | | | | | | |

Loss from operations | (52,074 | ) | | (61,164 | ) | | (208,192 | ) | | (171,169 | ) |

| | | | | | | |

Other income (expense) | | | | | | | |

Interest expense, net of capitalized interest | (93,566 | ) | | (46,884 | ) | | (238,664 | ) | | (130,943 | ) |

Loss on early extinguishment of debt | — |

| | — |

| | (96,273 | ) | | (114,335 | ) |

Derivative gain (loss), net | (161,482 | ) | | 5,379 |

| | (242,123 | ) | | (89,222 | ) |

Other income (expense) | (39 | ) | | (160 | ) | | 616 |

| | (39 | ) |

Total other expense | (255,087 | ) | | (41,665 | ) | | (576,444 | ) | | (334,539 | ) |

| | | | | | | |

Loss before income taxes and non-controlling interest | (307,161 | ) |

| (102,829 | ) |

| (784,636 | ) |

| (505,708 | ) |

Income tax benefit (expense) | 69 |

|

| (1,971 | ) |

| (102 | ) |

| (2,147 | ) |

Net loss | (307,092 | ) |

| (104,800 | ) |

| (784,738 | ) |

| (507,855 | ) |

Less: net loss attributable to non-controlling interest | (9,284 | ) |

| (15,219 | ) |

| (100,726 | ) |

| (118,536 | ) |

Net loss attributable to common stockholders | $ | (297,808 | ) |

| $ | (89,581 | ) |

| $ | (684,012 | ) |

| $ | (389,319 | ) |

|

|

|

|

|

|

|

|

|

|

|

|

Net loss per share attributable to common stockholders—basic and diluted | $ | (1.31 | ) |

| $ | (0.40 | ) |

| $ | (3.02 | ) |

| $ | (1.74 | ) |

|

|

|

|

|

|

|

|

|

|

|

|

Weighted average number of common shares outstanding—basic and diluted | 227,126 |

|

| 224,309 |

|

| 226,648 |

|

| 223,710 |

|

The accompanying notes are an integral part of these consolidated financial statements.

4

CHENIERE ENERGY, INC. AND SUBSIDIARIES

CONSOLIDATED STATEMENT OF STOCKHOLDERS’ EQUITY

(in thousands)

(unaudited)

|

| | | | | | | | | | | | | | | | | | | | | | | | | | | | | |

| Total Stockholders’ Equity | | | |

| Common Stock | | Treasury Stock | | Additional Paid-in Capital | | Accumulated Deficit | | Non-controlling Interest | | Total Equity |

| Shares | | Amount | | Shares | | Amount | | | | |

Balance at December 31, 2014 | 236,745 |

| | $ | 712 |

| | 10,596 |

| | $ | (292,752 | ) | | $ | 2,776,702 |

| | $ | (2,648,839 | ) | | $ | 2,665,694 |

| | $ | 2,501,517 |

|

Exercise of stock options | 67 |

| | — |

| | — |

| | — |

| | 2,279 |

| | — |

| | — |

| | 2,279 |

|

Issuances of restricted stock | 19 |

| | — |

| | — |

| | — |

| | — |

| | — |

| | — |

| | — |

|

Forfeitures of restricted stock | (152 | ) | | (1 | ) | | 17 |

| | — |

| | 1 |

| | — |

| | — |

| | — |

|

Share-based compensation | — |

| | — |

| | — |

| | — |

| | 50,582 |

| | — |

| | — |

| | 50,582 |

|

Shares repurchased related to share-based compensation | (635 | ) | | (3 | ) | | 635 |

| | (44,305 | ) | | 3 |

| | — |

| | — |

| | (44,305 | ) |

Excess tax benefit from share-based compensation | — |

| | — |

| | — |

| | — |

| | 1,424 |

| | — |

| | — |

| | 1,424 |

|

Equity portion of issuance of convertible notes, net | — |

| | — |

| | — |

| | — |

| | 198,326 |

| | — |

| | — |

| | 198,326 |

|

Loss attributable to non-controlling interest | — |

| | — |

| | — |

| | — |

| | — |

| | — |

| | (100,726 | ) | | (100,726 | ) |

Distributions to non-controlling interest | — |

| | — |

| | — |

| | — |

| | — |

| | — |

| | (60,154 | ) | | (60,154 | ) |

Net loss | — |

| | — |

| | — |

| | — |

| | — |

| | (684,012 | ) | | — |

| | (684,012 | ) |

Balance at September 30, 2015 | 236,044 |

| | $ | 708 |

| | 11,248 |

| | $ | (337,057 | ) | | $ | 3,029,317 |

| | $ | (3,332,851 | ) | | $ | 2,504,814 |

| | $ | 1,864,931 |

|

The accompanying notes are an integral part of these consolidated financial statements.

5

CHENIERE ENERGY, INC. AND SUBSIDIARIES

CONSOLIDATED STATEMENTS OF CASH FLOWS

(in thousands)

(unaudited)

|

| | | | | | | |

| Nine Months Ended |

| September 30, |

| 2015 | | 2014 |

Cash flows from operating activities | | | |

Net loss | $ | (784,738 | ) | | $ | (507,855 | ) |

Adjustments to reconcile net loss to net cash used in operating activities: | | | |

Non-cash LNG inventory write-downs | 17,826 |

| | 23,505 |

|

Depreciation expense | 59,561 |

| | 48,962 |

|

Share-based compensation | 90,412 |

| | 84,449 |

|

Amortization of debt issuance costs and discount (premium) | 36,782 |

| | 10,971 |

|

Loss on early extinguishment of debt | 96,273 |

| | 114,335 |

|

Total losses on derivatives, net | 208,769 |

| | 89,286 |

|

Net cash used for settlement of derivative instruments | (94,170 | ) | | (19,745 | ) |

Other | 1,406 |

| | (1,975 | ) |

Changes in restricted cash for certain operating activities | 92,589 |

| | 102,851 |

|

Changes in operating assets and liabilities: | | | |

Accounts and interest receivable | (2,226 | ) | | (18,899 | ) |

LNG inventory | (22,564 | ) | | (26,908 | ) |

Accounts payable and accrued liabilities | 10,656 |

| | 62,797 |

|

Deferred revenue | (3,003 | ) | | (2,955 | ) |

Other, net | 17,850 |

| | 131 |

|

Net cash used in operating activities | (274,577 | ) | | (41,050 | ) |

| | | |

Cash flows from investing activities | | | |

Property, plant and equipment, net | (5,747,596 | ) | | (2,047,957 | ) |

Use of restricted cash for the acquisition of property, plant and equipment | 5,330,526 |

| | 1,980,436 |

|

Other | (111,518 | ) | | (24,113 | ) |

Net cash used in investing activities | (528,588 | ) | | (91,634 | ) |

| | | |

Cash flows from financing activities | | | |

Proceeds from issuances of long-term debt | 6,178,000 |

| | 2,584,500 |

|

Repayments of long-term debt | — |

| | (177,000 | ) |

Debt issuance and deferred financing costs | (519,699 | ) | | (94,220 | ) |

Investment in restricted cash | (5,161,701 | ) | | (2,254,733 | ) |

Distributions and dividends to non-controlling interest | (60,154 | ) | | (59,478 | ) |

Proceeds from exercise of stock options | 2,279 |

| | 9,502 |

|

Payments related to tax withholdings for share-based compensation | (44,305 | ) | | (44,516 | ) |

Other | 1,424 |

| | (557 | ) |

Net cash provided by (used in) financing activities | 395,844 |

| | (36,502 | ) |

| | | |

Net decrease in cash and cash equivalents | (407,321 | ) | | (169,186 | ) |

Cash and cash equivalents—beginning of period | 1,747,583 |

| | 960,842 |

|

Cash and cash equivalents—end of period | $ | 1,340,262 |

| | $ | 791,656 |

|

The accompanying notes are an integral part of these consolidated financial statements.

6

CHENIERE ENERGY, INC. AND SUBSIDIARIES

NOTES TO CONSOLIDATED FINANCIAL STATEMENTS

(unaudited)

NOTE 1—BASIS OF PRESENTATION

The accompanying unaudited Consolidated Financial Statements of Cheniere have been prepared in accordance with GAAP for interim financial information and with Rule 10-01 of Regulation S-X. Accordingly, they do not include all of the information and footnotes required by GAAP for complete financial statements. In our opinion, all adjustments, consisting only of normal recurring adjustments necessary for a fair presentation, have been included. Certain reclassifications have been made to conform prior period information to the current presentation. The reclassifications had no effect on our overall consolidated financial position, results of operations or cash flows.

Results of operations for the three and nine months ended September 30, 2015 are not necessarily indicative of the results of operations that will be realized for the year ending December 31, 2015.

For further information, refer to the Consolidated Financial Statements and accompanying notes included in our Annual Report on Form 10-K for the year ended December 31, 2014.

NOTE 2—RESTRICTED CASH

Restricted cash consists of funds that are contractually restricted as to usage or withdrawal and have been presented separately from cash and cash equivalents on our Consolidated Balance Sheets. Restricted cash includes the following:

SPLNG Senior Notes Debt Service Reserve

SPLNG has consummated private offerings of an aggregate principal amount of $1,665.5 million, before discount, of 7.50% Senior Secured Notes due 2016 (the “2016 SPLNG Senior Notes”) and $420.0 million of 6.50% Senior Secured Notes due 2020 (the “2020 SPLNG Senior Notes” and collectively with the 2016 SPLNG Senior Notes, the “SPLNG Senior Notes”). Under the indentures governing the SPLNG Senior Notes (the “SPLNG Indentures”), except for permitted tax distributions, SPLNG may not make distributions until certain conditions are satisfied, including: (1) there must be on deposit in an interest payment account an amount equal to one-sixth of the semi-annual interest payment multiplied by the number of elapsed months since the last semi-annual interest payment, and (2) there must be on deposit in a permanent debt service reserve fund an amount equal to one semi-annual interest payment. Distributions are permitted only after satisfying the foregoing funding requirements, a fixed charge coverage ratio test of 2:1 and other conditions specified in the SPLNG Indentures.

As of September 30, 2015 and December 31, 2014, we classified $53.0 million and $15.0 million, respectively, as current restricted cash for the payment of current interest due. As of both September 30, 2015 and December 31, 2014, we classified the permanent debt service reserve fund of $76.1 million as non-current restricted cash. These cash accounts are controlled by a collateral trustee; therefore, these amounts are shown as restricted cash on our Consolidated Balance Sheets.

SPL Reserve

During 2013, SPL entered into four credit facilities aggregating $5.9 billion (collectively, the “2013 SPL Credit Facilities”). In June 2015, SPL entered into four credit facilities aggregating $4.6 billion (collectively, the “2015 SPL Credit Facilities”), which replaced the 2013 SPL Credit Facilities. Under the terms and conditions of the 2015 SPL Credit Facilities (and previously the 2013 SPL Credit Facilities), SPL is required to deposit all cash received into reserve accounts controlled by a collateral trustee. The usage or withdrawal of such cash is restricted to the payment of liabilities related to the natural gas liquefaction facilities that are being developed and constructed in Cameron Parish, Louisiana (the “SPL Project”); therefore, these amounts are shown as restricted cash on our Consolidated Balance Sheets.

During 2013, SPL issued an aggregate principal amount of $2.0 billion, before premium, of 5.625% Senior Secured Notes due 2021 (the “2021 SPL Senior Notes”), $1.0 billion of 6.25% Senior Secured Notes due 2022 (the “2022 SPL Senior Notes”) and $1.0 billion of 5.625% Senior Secured Notes due 2023 (the “Initial 2023 SPL Senior Notes”). During 2014, SPL issued an aggregate principal amount of $2.0 billion of 5.75% Senior Secured Notes due 2024 (the “2024 SPL Senior Notes”) and additional 5.625% Senior Secured Notes due 2023 in an aggregate principal amount of $0.5 billion, before premium (the “Additional 2023 SPL Senior Notes” and collectively with the Initial 2023 SPL Senior Notes, the “2023 SPL Senior Notes”). In March 2015, SPL issued an aggregate principal amount of $2.0 billion of 5.625% Senior Secured Notes due 2025 (the “2025 SPL Senior Notes” and

CHENIERE ENERGY, INC. AND SUBSIDIARIES

NOTES TO CONSOLIDATED FINANCIAL STATEMENTS—CONTINUED

(unaudited)

collectively with the 2021 SPL Senior Notes, the 2022 SPL Senior Notes, the 2023 SPL Senior Notes and the 2024 SPL Senior Notes, the “SPL Senior Notes”). The use of cash proceeds from the SPL Senior Notes is restricted to the payment of liabilities related to the SPL Project; therefore, these amounts are shown as restricted cash on our Consolidated Balance Sheets. See Note 7—Long-Term Debt for additional details about our long-term debt.

As of September 30, 2015 and December 31, 2014, we classified $327.2 million and $155.8 million, respectively, as current restricted cash held by SPL for the payment of current liabilities, including interest payments, related to the SPL Project and zero and $457.1 million, respectively, as non-current restricted cash held by SPL for future SPL Project construction costs.

CTPL Reserve

In May 2013, CTPL entered into a $400.0 million term loan facility (the “CTPL Term Loan”). As of September 30, 2015 and December 31, 2014, we classified $11.3 million and $24.9 million, respectively, as current restricted cash held by CTPL for the payment of current liabilities and zero and $11.3 million, respectively, as non-current restricted cash held by CTPL, because the usage and withdrawal of such funds is primarily restricted to the payment of liabilities related to modifications of the 94-mile pipeline which interconnects the Sabine Pass LNG terminal with a number of large interstate pipelines (the “Creole Trail Pipeline”) in order to enable bi-directional natural gas flow, and for the payment of interest during construction of such modifications. The restricted cash reserved to pay interest during construction is controlled by a collateral agent, and can only be released by the collateral agent upon satisfaction of certain terms and conditions. CTPL is required to pay annual fees to the administrative and collateral agents.

CCH Reserve

In May 2015, CCH entered into a credit facility agreement for an aggregate commitment of approximately $11.5 billion (the “2015 CCH Credit Facility”), comprising approximately $8.4 billion linked to the first stage (“Stage 1”) of the natural gas liquefaction and export facility and pipeline facility near Corpus Christi, Texas (the “CCL Project”) and approximately $3.1 billion linked to the second stage (“Stage 2”) of the CCL Project. Stage 1 includes Trains 1 and 2, two LNG storage tanks, one complete marine berth and second partial berth and all of the project’s necessary infrastructure facilities. The pipeline facility is a 23-mile, 48” natural gas pipeline that will interconnect the Corpus Christi LNG terminal with several interstate and intrastate natural gas pipelines (the “Corpus Christi Pipeline”). Stage 2 includes Train 3, one LNG storage tank and the completion of the second partial berth. Under the terms and conditions of the 2015 CCH Credit Facility, all cash reserved to pay interest during construction is controlled by a collateral agent. These funds can only be released by the collateral agent upon satisfaction of certain terms and conditions and are classified as restricted on our Consolidated Balance Sheets. CCH is required to pay annual fees to the administrative and collateral agents. As of September 30, 2015, we classified $35.6 million and $35.7 million as current restricted cash and non-current restricted cash, respectively, held by CCH.

Other Restricted Cash

As of September 30, 2015 and December 31, 2014, $171.4 million and $250.1 million, respectively, of cash was held by SPLNG, Cheniere Partners and Cheniere Holdings that was restricted to Cheniere. In addition, as of September 30, 2015 and December 31, 2014, $53.7 million and $35.9 million, respectively, had been classified as current restricted cash, and as of September 30, 2015 and December 31, 2014, $7.1 million and $6.3 million, respectively, had been classified as non-current restricted cash on our Consolidated Balance Sheets due to various other contractual restrictions.

CHENIERE ENERGY, INC. AND SUBSIDIARIES

NOTES TO CONSOLIDATED FINANCIAL STATEMENTS—CONTINUED

(unaudited)

NOTE 3—PROPERTY, PLANT AND EQUIPMENT

Property, plant and equipment consists of LNG terminal costs and fixed assets and other, as follows (in thousands):

|

| | | | | | | |

| September 30, | | December 31, |

| 2015 | | 2014 |

LNG terminal costs | | | |

LNG terminal | $ | 2,478,167 |

| | $ | 2,269,429 |

|

LNG terminal construction-in-process | 12,887,040 |

| | 7,155,046 |

|

LNG site and related costs, net | 32,823 |

| | 9,395 |

|

Accumulated depreciation | (397,758 | ) | | (350,497 | ) |

Total LNG terminal costs, net | 15,000,272 |

| | 9,083,373 |

|

Fixed assets and other | |

| | |

|

Computer and office equipment | 11,197 |

| | 7,464 |

|

Furniture and fixtures | 16,737 |

| | 10,733 |

|

Computer software | 64,432 |

| | 46,882 |

|

Leasehold improvements | 38,573 |

| | 36,067 |

|

Land | 60,984 |

| | 55,522 |

|

Other | 65,138 |

| | 36,881 |

|

Accumulated depreciation | (32,083 | ) | | (30,169 | ) |

Total fixed assets and other, net | 224,978 |

| | 163,380 |

|

Property, plant and equipment, net | $ | 15,225,250 |

| | $ | 9,246,753 |

|

NOTE 4—DERIVATIVE INSTRUMENTS

We have entered into the following derivative instruments that are reported at fair value:

| |

• | commodity derivatives to hedge the exposure to price risk attributable to future: (1) sales of our LNG inventory and (2) purchases of natural gas to operate the Sabine Pass LNG terminal (“Natural Gas Derivatives”); |

| |

• | commodity derivatives consisting of natural gas purchase agreements and associated economic hedges to secure natural gas feedstock for the SPL Project (“Liquefaction Supply Derivatives”); |

| |

• | financial derivatives to hedge the exposure to the commodity markets in which we have contractual arrangements to purchase or sell physical LNG (“LNG Trading Derivatives”); |

| |

• | interest rate swaps to hedge the exposure to volatility in a portion of the floating-rate interest payments under the 2015 SPL Credit Facilities (and previously the 2013 SPL Credit Facilities) (“SPL Interest Rate Derivatives”); and |

| |

• | interest rate swaps to hedge the exposure to volatility in a portion of the floating-rate interest payments under the 2015 CCH Credit Facility (“CCH Interest Rate Derivatives” and, collectively with the SPL Interest Rate Derivatives, the “Interest Rate Derivatives”). |

None of our derivative instruments are designated as cash flow hedging instruments, and changes in fair value are recorded within our Consolidated Statements of Operations.

CHENIERE ENERGY, INC. AND SUBSIDIARIES

NOTES TO CONSOLIDATED FINANCIAL STATEMENTS—CONTINUED

(unaudited)

The following table (in thousands) shows the fair value of our derivative instruments that are required to be measured at fair value on a recurring basis as of September 30, 2015 and December 31, 2014, which are classified as other current assets, non-current derivative assets, derivative liabilities or non-current derivative liabilities in our Consolidated Balance Sheets.

|

| | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | |

| Fair Value Measurements as of |

| September 30, 2015 | | December 31, 2014 |

| Quoted Prices in Active Markets (Level 1) | | Significant Other Observable Inputs (Level 2) | | Significant Unobservable Inputs (Level 3) | | Total | | Quoted Prices in Active Markets (Level 1) | | Significant Other Observable Inputs (Level 2) | | Significant Unobservable Inputs (Level 3) | | Total |

Natural Gas Derivatives asset | $ | — |

| | $ | 97 |

| | $ | — |

| | $ | 97 |

| | $ | — |

| | $ | 219 |

| | $ | — |

| | $ | 219 |

|

Liquefaction Supply Derivatives asset | — |

| | — |

| | 32,546 |

| | 32,546 |

| | — |

| | — |

| | 342 |

| | 342 |

|

LNG Trading Derivatives asset | — |

| | 113 |

| | — |

| | 113 |

| | — |

| | — |

| | — |

| | — |

|

SPL Interest Rate Derivatives liability | — |

| | (15,738 | ) | | — |

| | (15,738 | ) | | — |

| | (12,036 | ) | | — |

| | (12,036 | ) |

CCH Interest Rate Derivatives liability | — |

| | (143,092 | ) | | — |

| | (143,092 | ) | | — |

| | — |

| | — |

| | — |

|

The estimated fair values of our Natural Gas Derivatives and the economic hedges related to the LNG Trading Derivatives are the amounts at which the instruments could be exchanged currently between willing parties. We value these derivatives using observable commodity price curves and other relevant data. We value the Interest Rate Derivatives using valuations based on the initial trade prices. Using an income-based approach, subsequent valuations are based on observable inputs to the valuation model including interest rate curves, risk adjusted discount rates, credit spreads and other relevant data.

The fair value of substantially all of the Liquefaction Supply Derivatives is developed through the use of internal models which are impacted by inputs that are unobservable in the marketplace. As a result, the fair value of the Liquefaction Supply Derivatives is designated as Level 3 within the valuation hierarchy. The curves used to generate the fair value of the Liquefaction Supply Derivatives are based on basis adjustments applied to forward curves for a liquid trading point. In addition, there may be observable liquid market basis information in the near term, but terms of a particular Liquefaction Supply Derivatives contract may exceed the period for which such information is available, resulting in a Level 3 classification. In these instances, the fair value of the contract incorporates extrapolation assumptions made in the determination of the market basis price for future delivery periods in which applicable commodity basis prices were either not observable or lacked corroborative market data. Internal fair value models that include contractual pricing with a fixed basis include fixed basis amounts for delivery at locations for which no market currently exists. Internal fair value models also include conditions precedent to the respective long-term natural gas purchase agreements. As of September 30, 2015 and December 31, 2014, some of the Liquefaction Supply Derivatives existed within markets for which the pipeline infrastructure has not been developed to accommodate marketable physical gas flow. In the absence of infrastructure to accommodate marketable physical gas flow, our internal fair value models are based on a market price that equates to our own contractual pricing due to: (1) the inactive and unobservable market and (2) conditions precedent and their impact on the uncertainty in the timing of our actual receipt of the physical volumes associated with each forward. The fair value of the Liquefaction Supply Derivatives is predominantly driven by market commodity basis prices and our assessment of the associated conditions precedent, including evaluating whether the respective market is available as pipeline infrastructure is developed. Upon the completion and placement into service of relevant pipeline infrastructure to accommodate marketable physical gas flow, we recognize a gain or loss based on the fair value of the respective natural gas purchase agreements as of the reporting date.

CHENIERE ENERGY, INC. AND SUBSIDIARIES

NOTES TO CONSOLIDATED FINANCIAL STATEMENTS—CONTINUED

(unaudited)

There were no transfers into or out of Level 3 Liquefaction Supply Derivatives for the three and nine months ended September 30, 2015 and 2014. As all of the physical Liquefaction Supply Derivatives are either purely index-priced or index-priced with a fixed basis, we do not believe that a significant change in market commodity prices would have a material impact on our Level 3 fair value measurements. The following table includes quantitative information for the unobservable inputs for the Level 3 Liquefaction Supply Derivatives as of September 30, 2015:

|

| | | | | | | | |

| | Net Fair Value Asset (in thousands) | | Valuation Technique | | Significant Unobservable Input | | Significant Unobservable Inputs Range |

Liquefaction Supply Derivatives | | $32,546 | | Income Approach | | Basis Spread | | $ (0.350) - $0.050 |

Derivative assets and liabilities arising from our derivative contracts with the same counterparty are reported on a net basis, as all counterparty derivative contracts provide for net settlement. The use of derivative instruments exposes us to counterparty credit risk, or the risk that a counterparty will be unable to meet its commitments in instances when our derivative instruments are in an asset position.

Commodity Derivatives

We recognize all commodity derivative instruments, including our Natural Gas Derivatives, Liquefaction Supply Derivatives and LNG Trading Derivatives (collectively, “Commodity Derivatives”), as either assets or liabilities and measure those instruments at fair value. Changes in the fair value of our Commodity Derivatives are reported in earnings.

The following table (in thousands) shows the fair value and location of our Commodity Derivatives on our Consolidated Balance Sheets:

|

| | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | |

| | September 30, 2015 | | December 31, 2014 |

| | Natural Gas Derivatives (1) | | Liquefaction Supply Derivatives | | LNG Trading Derivatives | | Total | | Natural Gas Derivatives (1) | | Liquefaction Supply Derivatives | | LNG Trading Derivatives | | Total |

Balance Sheet Location | | | | | | | | | | | | | | | | |

Other current assets | | $ | 97 |

| | $ | 2,371 |

| | $ | — |

| | $ | 2,468 |

| | $ | 219 |

| | $ | 76 |

| | $ | — |

| | $ | 295 |

|

Non-current derivative assets | | — |

| | 30,657 |

| | 113 |

| | 30,770 |

| | — |

| | 586 |

| | — |

| | 586 |

|

Total derivative assets | | 97 |

| | 33,028 |

| | 113 |

| | 33,238 |

| | 219 |

| | 662 |

| | — |

| | 881 |

|

| | | | | | | | | | | | | | | | |

Derivative liabilities | | — |

| | (349 | ) | | — |

| | (349 | ) | | — |

| | (53 | ) | | — |

| | (53 | ) |

Non-current derivative liabilities | | — |

| | (133 | ) | | — |

| | (133 | ) | | — |

| | (267 | ) | | — |

| | (267 | ) |

Total derivative liabilities | | — |

| | (482 | ) | | — |

| | (482 | ) | | — |

| | (320 | ) | | — |

| | (320 | ) |

| | | | | | | | | | | | | | | | |

Derivative asset, net | | $ | 97 |

| | $ | 32,546 |

| | $ | 113 |

| | $ | 32,756 |

| | $ | 219 |

| | $ | 342 |

| | $ | — |

| | $ | 561 |

|

| |

(1) | Does not include collateral of $5.6 million and $5.7 million deposited for such contracts, which is included in other current assets in our Consolidated Balance Sheets as of September 30, 2015 and December 31, 2014, respectively. |

CHENIERE ENERGY, INC. AND SUBSIDIARIES

NOTES TO CONSOLIDATED FINANCIAL STATEMENTS—CONTINUED

(unaudited)

The following table (in thousands) shows the changes in the fair value and settlements and location of our Commodity Derivatives recorded on our Consolidated Statements of Operations during the three and nine months ended September 30, 2015 and 2014:

|

| | | | | | | | | | | | | | | | | |

| | | Three Months Ended September 30, | | Nine Months Ended September 30, |

| Statement of Operations Location | | 2015 | | 2014 | | 2015 | | 2014 |

Natural Gas Derivatives loss | Marketing and trading revenues (losses) | | $ | (152 | ) | | $ | (525 | ) | | $ | (260 | ) | | $ | (155 | ) |

Natural Gas Derivatives gain (loss) | Operating and maintenance expense (income) | | 857 |

| | 194 |

| | 1,317 |

| | (64 | ) |

Liquefaction Supply Derivatives gain (1) | Operating and maintenance expense (income) | | 32,103 |

| | — |

| | 32,184 |

| | — |

|

LNG Trading Derivatives gain | Marketing and trading revenues (losses) | | 113 |

| | — |

| | 113 |

| | — |

|

| |

(1) | There were no physical settlements during the reporting period. |

Natural Gas Derivatives

Our Natural Gas Derivatives are executed through over-the-counter contracts which are subject to nominal credit risk as these transactions are settled on a daily margin basis with investment grade financial institutions. We are required by these financial institutions to use margin deposits as credit support for our Natural Gas Derivatives activities.

Liquefaction Supply Derivatives

SPL has entered into index-based physical natural gas supply contracts and associated economic hedges to secure natural gas feedstock for the SPL Project. The terms of the physical contracts range from approximately one to seven years and commence upon the occurrence of conditions precedent, including the date of first commercial operation of specified Trains of the SPL Project. We recognize the Liquefaction Supply Derivatives as either assets or liabilities and measure those instruments at fair value. Changes in the fair value of the Liquefaction Supply Derivatives are reported in earnings. As of September 30, 2015, SPL has secured up to approximately 2,156.6 million MMBtu of natural gas feedstock through long-term natural gas purchase agreements, of which the forward notional natural gas buy position of the Liquefaction Supply Derivatives was approximately 1,244.1 million MMBtu, which were recorded as derivatives due to minimum purchase requirements.

LNG Trading Derivatives

As of September 30, 2015, we have entered into certain LNG Trading Derivatives representing a short position of 1.5 million MMBtu, and we may from time to time enter into certain financial derivatives in the form of swaps, forwards, options or futures to economically hedge exposure to the commodity markets in which we have contractual arrangements to purchase or sell physical LNG. We have entered into LNG Trading Derivatives to secure a fixed price position to minimize future cash flow variability associated with such LNG transactions.

Interest Rate Derivatives

SPL Interest Rate Derivatives

SPL has entered into SPL Interest Rate Derivatives to protect against volatility of future cash flows and hedge a portion of the variable interest payments on the 2015 SPL Credit Facilities. The SPL Interest Rate Derivatives hedge a portion of the expected outstanding borrowings over the term of the 2015 SPL Credit Facilities.

In March 2015, SPL settled a portion of the SPL Interest Rate Derivatives and recognized a derivative loss of $34.7 million within our Consolidated Statements of Operations in conjunction with the termination of approximately $1.8 billion of commitments under the 2013 SPL Credit Facilities as discussed in Note 7—Long-Term Debt. In May 2014, SPL settled a portion of the SPL Interest Rate Derivatives and recognized a derivative loss of $9.3 million within our Consolidated Statements of Operations in conjunction with the early termination of approximately $2.1 billion of commitments under the 2013 SPL Credit Facilities.

CHENIERE ENERGY, INC. AND SUBSIDIARIES

NOTES TO CONSOLIDATED FINANCIAL STATEMENTS—CONTINUED

(unaudited)

CCH Interest Rate Derivatives

In February 2015, CCH entered into CCH Interest Rate Derivatives to protect against volatility of future cash flows and hedge a portion of the variable interest payments on the 2015 CCH Credit Facility. The CCH Interest Rate Derivatives hedge a portion of the expected outstanding borrowings over the term of the 2015 CCH Credit Facility. The CCH Interest Rate Derivatives have a seven-year term and were contingent upon reaching a final investment decision with respect to the CCL Project, which was reached in May 2015. Upon meeting the contingency related to the CCH Interest Rate Derivatives in May 2015, we paid $50.1 million related to contingency and syndication premiums, which is included in derivative gain (loss), net on our Consolidated Statements of Operations.

As of September 30, 2015, we had the following Interest Rate Derivatives outstanding:

|

| | | | | | | | | | | | |

| | Initial Notional Amount | | Maximum Notional Amount | | Effective Date | | Maturity Date | | Weighted Average Fixed Interest Rate Paid | | Variable Interest Rate Received |

SPL Interest Rate Derivatives | | $20.0 million | | $628.8 million | | August 14, 2012 | | July 31, 2019 | | 1.98% | | One-month LIBOR |

CCH Interest Rate Derivatives | | $28.8 million | | $5.5 billion | | May 20, 2015 | | May 31, 2022 | | 2.29% | | One-month LIBOR |

The following table (in thousands) shows the fair value and location of the Interest Rate Derivatives on our Consolidated Balance Sheets:

|

| | | | | | | | | | | | | | | | | | | | | | | | |

| | September 30, 2015 | | December 31, 2014 |

| | SPL Interest Rate Derivatives | | CCH Interest Rate Derivatives | | Total | | SPL Interest Rate Derivatives | | CCH Interest Rate Derivatives | | Total |

Balance Sheet Location | | | | | | | | | | | | |

Non-current derivative assets | | $ | — |

| | $ | — |

| | $ | — |

| | $ | 11,158 |

| | $ | — |

| | $ | 11,158 |

|

| | | | | | | | | | | | |

Derivative liabilities | | (7,039 | ) | | (26,451 | ) | | (33,490 | ) | | (23,194 | ) | | — |

| | (23,194 | ) |

Non-current derivative liabilities | | (8,699 | ) | | (116,641 | ) | | (125,340 | ) | | — |

| | — |

| | — |

|

Total derivative liabilities | | (15,738 | ) | | (143,092 | ) | | (158,830 | ) | | (23,194 | ) | | — |

| | (23,194 | ) |

| | | | | | | | | | | | |

Derivative liability, net | | $ | (15,738 | ) | | $ | (143,092 | ) | | $ | (158,830 | ) | | $ | (12,036 | ) | | $ | — |

| | $ | (12,036 | ) |

The following table (in thousands) shows the changes in the fair value and settlements of the Interest Rate Derivatives, including contingency and syndication premiums related to the CCH Interest Rate Derivatives, recorded in derivative gain (loss), net on our Consolidated Statements of Operations during the three and nine months ended September 30, 2015 and 2014:

|

| | | | | | | | | | | | | | | | |

| | Three Months Ended September 30, | | Nine Months Ended September 30, |

| | 2015 | | 2014 | | 2015 | | 2014 |

SPL Interest Rate Derivatives gain (loss) | | $ | (10,872 | ) | | $ | 5,379 |

| | $ | (46,541 | ) | | $ | (89,222 | ) |

CCH Interest Rate Derivatives loss | | (150,610 | ) | | — |

| | (195,582 | ) | | — |

|

CHENIERE ENERGY, INC. AND SUBSIDIARIES

NOTES TO CONSOLIDATED FINANCIAL STATEMENTS—CONTINUED

(unaudited)

Balance Sheet Presentation

Our Commodity Derivatives and Interest Rate Derivatives are presented on a net basis on our Consolidated Balance Sheets as described above. The following table (in thousands) shows the fair value of our derivatives outstanding on a gross and net basis:

|

| | | | | | | | | | | | |

| | Gross Amounts Recognized | | Gross Amounts Offset in the Consolidated Balance Sheets | | Net Amounts Presented in the Consolidated Balance Sheets |

Offsetting Derivative Assets (Liabilities) | | | |

As of September 30, 2015 | | | | | | |

Natural Gas Derivatives | | $ | 513 |

| | $ | (416 | ) | | $ | 97 |

|

Liquefaction Supply Derivatives | | 33,028 |

| | — |

| | 33,028 |

|

Liquefaction Supply Derivatives | | (482 | ) | | — |

| | (482 | ) |

LNG Trading Derivatives | | 113 |

| | — |

| | 113 |

|

SPL Interest Rate Derivatives | | (15,738 | ) | | — |

| | (15,738 | ) |

CCH Interest Rate Derivatives | | (143,092 | ) | | — |

| | (143,092 | ) |

As of December 31, 2014 | | | | | | |

Natural Gas Derivatives | | 223 |

| | (4 | ) | | 219 |

|

Liquefaction Supply Derivatives | | 662 |

| | — |

| | 662 |

|

Liquefaction Supply Derivatives | | (320 | ) | | — |

| | (320 | ) |

SPL Interest Rate Derivatives | | 11,158 |

| | — |

| | 11,158 |

|

SPL Interest Rate Derivatives | | (23,194 | ) | | — |

| | (23,194 | ) |

NOTE 5—NON-CONTROLLING INTEREST

Cheniere Holdings was formed by us to hold our limited partner interest in Cheniere Partners and in December 2013, completed its initial public offering. Additionally, in November 2014, Cheniere Holdings sold 10.1 million common shares at $22.76 per common share to redeem from us the same number of common shares. As of both September 30, 2015 and December 31, 2014, our ownership interest in Cheniere Holdings was 80.1%, with the remaining non-controlling interest held by the public. Cheniere Holdings owns a 55.9% limited partner interest in Cheniere Partners in the form of 12.0 million common units, 45.3 million Class B units and 135.4 million subordinated units, with the remaining non-controlling interest held by Blackstone CQP Holdco LP and the public. We also own 100% of the general partner interest and the incentive distribution rights in Cheniere Partners.

NOTE 6—ACCRUED LIABILITIES

As of September 30, 2015 and December 31, 2014, accrued liabilities consisted of the following (in thousands):

|

| | | | | | | | |

| | September 30, | | December 31, |

| | 2015 | | 2014 |

Interest expense and related debt fees | | $ | 170,254 |

| | $ | 112,858 |

|

Compensation and benefits | | 83,581 |

| | 6,425 |

|

Liquefaction Project costs | | 181,219 |

| | 22,014 |

|

LNG terminal costs | | 5,987 |

| | 1,077 |

|

Other accrued liabilities | | 16,860 |

| | 26,755 |

|

Total accrued liabilities | | $ | 457,901 |

| | $ | 169,129 |

|

CHENIERE ENERGY, INC. AND SUBSIDIARIES

NOTES TO CONSOLIDATED FINANCIAL STATEMENTS—CONTINUED

(unaudited)

NOTE 7—LONG-TERM DEBT

As of September 30, 2015 and December 31, 2014, our long-term debt consisted of the following (in thousands):

|

| | | | | | | | | | |

| | Interest | | September 30, | | December 31, |

| | Rate | | 2015 | | 2014 |

Long-term debt | | | | | | |

2016 SPLNG Senior Notes | | 7.500% | | $ | 1,665,500 |

| | $ | 1,665,500 |

|

2020 SPLNG Senior Notes | | 6.500% | | 420,000 |

| | 420,000 |

|

2021 SPL Senior Notes | | 5.625% | | 2,000,000 |

| | 2,000,000 |

|

2022 SPL Senior Notes | | 6.250% | | 1,000,000 |

| | 1,000,000 |

|

2023 SPL Senior Notes | | 5.625% | | 1,500,000 |

| | 1,500,000 |

|

2024 SPL Senior Notes | | 5.750% | | 2,000,000 |

| | 2,000,000 |

|

2025 SPL Senior Notes | | 5.625% | | 2,000,000 |

| | — |

|

2015 SPL Credit Facilities (1) | | (2) | | 250,000 |

| | — |

|

2021 Cheniere Convertible Unsecured Notes | | 4.875% | | 1,028,953 |

| | 1,004,469 |

|

2025 CCH HoldCo II Convertible Senior Notes | | 11.000% | | 1,003,667 |

| | — |

|

2045 Cheniere Convertible Senior Notes | | 4.250% | | 625,000 |

| | — |

|

CTPL Term Loan (3) | | (4) | | 400,000 |

| | 400,000 |

|

2015 CCH Credit Facility (5) | | (6) | | 2,428,000 |

| | — |

|

SPL Working Capital Facility (7) | | (8) | | — |

| | — |

|

Total long-term debt | | | | 16,321,120 |

| | 9,989,969 |

|

Long-term debt premium (discount) | | | | |

| | |

|

2016 SPLNG Senior Notes | | | | (5,477 | ) | | (8,998 | ) |

2021 SPL Senior Notes | | | | 9,090 |

| | 10,177 |

|

2023 SPL Senior Notes | | | | 6,570 |

| | 7,088 |

|

2021 Cheniere Convertible Unsecured Notes | | | | (174,133 | ) | | (189,717 | ) |

2045 Cheniere Convertible Senior Notes | | | | (319,579 | ) | | — |

|

CTPL Term Loan | | | | (1,681 | ) | | (2,435 | ) |

Total long-term debt, net | | | | $ | 15,835,910 |

| | $ | 9,806,084 |

|

| |

(1) | Matures on the earlier of December 31, 2020 or the second anniversary of the completion date of Trains 1 through 5 of the SPL Project. |

| |

(2) | Variable interest rate, at SPL’s election, is LIBOR or the base rate plus the applicable margin. The applicable margins for LIBOR loans range from 1.30% to 1.75%, depending on the applicable 2015 SPL Credit Facility, and the applicable margin for base rate loans is 1.75%. Interest on LIBOR loans is due and payable at the end of each LIBOR period, and interest on base rate loans is due and payable at the end of each quarter. |

| |

(3) | Matures on May 28, 2017 when the full amount of the outstanding principal obligations must be repaid. |

| |

(4) | Variable interest rate, at CTPL’s election, is LIBOR or the base rate plus the applicable margin. CTPL has historically elected LIBOR loans, for which the applicable margin is 3.25% and is due and payable at the end of each LIBOR period. |

| |

(5) | Matures on the earlier of May 13, 2022 or the second anniversary of the completion date of the first two Trains of the CCL Project. |

| |

(6) | Variable interest rate, at CCH’s election, is LIBOR or the base rate plus the applicable margin. The applicable margins for LIBOR loans are 2.25% prior to completion of the first two Trains of the CCL Project and 2.50% on completion and thereafter. The applicable margins for base rate loans are 1.25% prior to completion of the first two Trains of the CCL Project and 1.50% on completion and thereafter. Interest on LIBOR loans is due and payable at the end of each applicable interest period, and interest on base rate loans is due and payable at the end of each quarter. |

| |

(7) | Matures on December 31, 2020, with various terms for underlying loans, as further described below under SPL Working Capital Facility. As of September 30, 2015 and December 31, 2014, no loans were outstanding under the SPL Working Capital Facility or the SPL LC Agreement it replaced. |

| |

(8) | Variable interest rates, based on LIBOR or the base rate, as further described below under SPL Working Capital Facility. |

For the three months ended September 30, 2015 and 2014, we incurred $286.0 million and $154.8 million of total interest cost, respectively, of which we capitalized and deferred $192.4 million and $107.9 million, respectively, including amortization

CHENIERE ENERGY, INC. AND SUBSIDIARIES

NOTES TO CONSOLIDATED FINANCIAL STATEMENTS—CONTINUED

(unaudited)

of debt issuance costs, primarily related to the construction of the SPL Project in both periods and additionally the CCL Project in 2015. For the nine months ended September 30, 2015 and 2014, we incurred $707.8 million and $423.8 million of total interest cost, respectively, of which we capitalized and deferred $469.2 million and $292.8 million, respectively, including amortization of debt issuance costs, primarily related to this construction.

SPLNG Senior Notes

Under the SPLNG Indentures, except for permitted tax distributions, SPLNG may not make distributions until certain conditions are satisfied as described in Note 2—Restricted Cash. During the nine months ended September 30, 2015 and 2014, SPLNG made distributions of $267.9 million and $237.7 million, respectively, after satisfying all the applicable conditions in the SPLNG Indentures. SPL Senior Notes

In March 2015, SPL issued an aggregate principal amount of $2.0 billion of the 2025 SPL Senior Notes, for which borrowings accrue interest at a fixed rate of 5.625%. The terms of the 2025 SPL Senior Notes are governed by the same common indenture with the other SPL Senior Notes. In connection with the closing of the sale of the 2025 SPL Senior Notes, SPL entered into a Registration Rights Agreement dated March 3, 2015 (the “2025 SPL Registration Rights Agreement”). Under the terms of the 2025 SPL Registration Rights Agreement, SPL has agreed, and any future guarantors of the 2025 SPL Senior Notes will agree, to use commercially reasonable efforts to file with the SEC and cause to become effective a registration statement within 360 days after March 3, 2015 with respect to an offer to exchange any and all of the 2025 SPL Senior Notes for a like aggregate principal amount of debt securities of SPL with terms identical in all material respects to the respective 2025 SPL Senior Notes sought to be exchanged (other than with respect to restrictions on transfer or to any increase in annual interest rate), and that are registered under the Securities Act of 1933, as amended (the “Securities Act”). Under specified circumstances, SPL has also agreed, and any future guarantors will also agree, to use commercially reasonable efforts to cause to become effective a shelf registration statement relating to resales of the 2025 SPL Senior Notes. SPL will be obligated to pay additional interest if it fails to comply with its obligations to register the 2025 SPL Senior Notes within the specified time period.

2015 SPL Credit Facilities

In June 2015, SPL entered into the 2015 SPL Credit Facilities with commitments aggregating $4.6 billion. The 2015 SPL Credit Facilities are being used to fund a portion of the costs of developing, constructing and placing into operation Trains 1 through 5 of the SPL Project. Borrowings under the 2015 SPL Credit Facilities may be refinanced, in whole or in part, at any time without premium or penalty; however, interest rate hedging and interest rate breakage costs may be incurred. As of September 30, 2015, SPL had $4.3 billion of available commitments and $250.0 million of outstanding borrowings under the 2015 SPL Credit Facilities.

SPL incurred $88.2 million of debt issuance costs in connection with the 2015 SPL Credit Facilities. In addition to interest, SPL is required to pay insurance/guarantee premiums of 0.45% per annum on any drawn amounts under the covered tranches of the 2015 SPL Credit Facilities. The 2015 SPL Credit Facilities also require SPL to pay a quarterly commitment fee calculated at a rate per annum equal to either: (1) 40% of the applicable margin, multiplied by the average daily amount of the undrawn commitment, or (2) 0.70% of the undrawn commitment, depending on the applicable 2015 SPL Credit Facility. The principal of the loans made under the 2015 SPL Credit Facilities must be repaid in quarterly installments, commencing with the earlier of June 30, 2020 and the last day of the first full calendar quarter after the completion date of Trains 1 through 5 of the SPL Project. Scheduled repayments are based upon an 18-year amortization profile, with the remaining balance due upon the maturity of the 2015 SPL Credit Facilities.

The 2015 SPL Credit Facilities contain conditions precedent for borrowings, as well as customary affirmative and negative covenants. The obligations of SPL under the 2015 SPL Credit Facilities are secured by substantially all of the assets of SPL as well as all of the membership interests in SPL on a pari passu basis with the SPL Senior Notes and the Amended and Restated Senior Working Capital Revolving Credit and Letter of Credit Reimbursement Agreement (the “SPL Working Capital Facility”) described below.

Under the terms of the 2015 SPL Credit Facilities, SPL is required to hedge not less than 65% of the variable interest rate exposure of its projected outstanding borrowings, calculated on a weighted average basis in comparison to its anticipated draw of principal.

CHENIERE ENERGY, INC. AND SUBSIDIARIES

NOTES TO CONSOLIDATED FINANCIAL STATEMENTS—CONTINUED

(unaudited)

2013 SPL Credit Facilities

In May 2013, SPL entered into the 2013 SPL Credit Facilities to fund a portion of the costs of developing, constructing and placing into operation Trains 1 through 4 of the SPL Project. As of December 31, 2014, SPL had no outstanding borrowings under the 2013 SPL Credit Facilities. In June 2015, the 2013 SPL Credit Facilities were replaced with the 2015 SPL Credit Facilities.

In March 2015, in conjunction with SPL’s issuance of the 2025 SPL Senior Notes, SPL terminated approximately $1.8 billion of commitments under the 2013 SPL Credit Facilities. This termination and the replacement of the 2013 SPL Credit Facilities with the 2015 SPL Credit Facilities in June 2015 resulted in a write-off of debt issuance costs and deferred commitment fees associated with the 2013 SPL Credit Facilities of $96.3 million for the nine months ended September 30, 2015.

Convertible Notes

2021 Cheniere Convertible Unsecured Notes

In November 2014, we issued an aggregate principal amount of $1.0 billion Convertible Unsecured Notes due 2021 (the “2021 Cheniere Convertible Unsecured Notes”) on a private placement basis in reliance on the exemption from registration provided for under section 4(a)(2) of the Securities Act and Regulation S promulgated thereunder. The 2021 Cheniere Convertible Unsecured Notes accrue interest at a rate of 4.875% per annum, which is payable in kind semi-annually in arrears by increasing the principal amount of the 2021 Cheniere Convertible Unsecured Notes outstanding. One year after the closing date, the 2021 Cheniere Convertible Unsecured Notes will be convertible at the option of the holder into our common stock at the then-applicable conversion rate, provided that the closing price of our common stock is greater than or equal to the conversion price on the conversion date. The initial conversion price was $93.64 and is subject to adjustment upon the occurrence of certain specified events. We have the option to satisfy the conversion obligation with cash, common stock or a combination thereof.

Under GAAP, certain convertible debt instruments that may be settled in cash upon conversion are required to be separately accounted for as liability (debt) and equity (conversion option) components of the instrument in a manner that reflects the issuer’s non-convertible debt borrowing rate. We determined that the fair value of the debt component was $808.8 million and the residual value of the equity component was $191.2 million as of the issuance date. As of September 30, 2015 and December 31, 2014, the carrying value of the equity component was $196.1 million and $191.9 million, respectively. The debt component is accreted to the total principal amount due at maturity by amortizing the debt discount. The effective rate of interest to amortize the debt discount was approximately 9.1% and 9.2% as of September 30, 2015 and December 31, 2014, respectively, and the remaining period over which the debt discount will be amortized was 5.7 years as of September 30, 2015. As of September 30, 2015, the if-converted value of the 2021 Cheniere Convertible Unsecured Notes did not exceed the principal balance.

2025 CCH HoldCo II Convertible Senior Notes

In May 2015, CCH HoldCo II issued $1.0 billion aggregate principal amount of 11% Senior Secured Notes due 2025 (the “2025 CCH HoldCo II Convertible Senior Notes”) on a private placement basis in reliance on the exemption from registration provided for under section 4(a)(2) of the Securities Act. The 2025 CCH HoldCo II Convertible Senior Notes were issued pursuant to the amended and restated note purchase agreement entered into among CCH HoldCo II, EIG Management Company, LLC, The Bank of New York Mellon, the Company and the note purchasers. The $1.0 billion principal of the 2025 CCH HoldCo II Convertible Senior Notes will be used to partially fund costs associated with Stage 1 of the CCL Project and the Corpus Christi Pipeline. The purchasers have made commitments, which will expire on May 1, 2016, to acquire an additional $500 million of 2025 CCH HoldCo II Convertible Senior Notes (the “Second Phase Funding”) upon satisfaction of incremental customary conditions precedent related to the construction of Stage 2 of the CCL Project. The 2025 CCH HoldCo II Convertible Senior Notes bear interest at a rate of 11.0% per annum, which is payable quarterly in arrears. Prior to the substantial completion of Train 2 of the CCL Project, if the Second Phase Funding has not occurred, and to the substantial completion of Train 3 of the CCL Project following the occurrence of the Second Phase Funding, interest on the 2025 CCH HoldCo II Convertible Senior Notes will be paid entirely in kind. Following this date, the interest generally must be paid in cash; however, a portion of the interest may be paid in kind under certain specified circumstances. The 2025 CCH HoldCo II Convertible Senior Notes are secured by a pledge by us of 100% of the equity interests in CCH HoldCo II, and a pledge by CCH HoldCo II of 100% of the equity interests in CCH HoldCo I.

CHENIERE ENERGY, INC. AND SUBSIDIARIES

NOTES TO CONSOLIDATED FINANCIAL STATEMENTS—CONTINUED

(unaudited)

At CCH HoldCo II’s option, the outstanding 2025 CCH HoldCo II Convertible Senior Notes are convertible into our common stock on or after the later of (1) 58 months from May 1, 2015, and (2) the substantial completion of Train 2 of the CCL Project and any 2025 CCH HoldCo II Convertible Senior Notes issued in connection with the Second Phase Funding will be convertible on or after the substantial completion of Train 3 of the CCL Project (in each case, the “Eligible Conversion Date”). The conversion price for 2025 CCH HoldCo II Convertible Senior Notes converted at CCH HoldCo II’s option is the lower of (1) a 10% discount to the average of the daily volume-weighted average price (“VWAP”) of our common stock for the 90 trading day period prior to the date on which notice of conversion is provided, and (2) a 10% discount to the closing price of our common stock on the trading day preceding the date on which notice of conversion is provided. At the option of the holders, the 2025 CCH HoldCo II Convertible Senior Notes are convertible on or after the six-month anniversary of the applicable Eligible Conversion Date at a conversion price equal to the average of the daily VWAP of our common stock for the 90 trading day period prior to the date on which notice of conversion is provided. Conversions are also subject to various limitations and conditions. As of September 30, 2015, the value of the 2025 CCH HoldCo II Convertible Senior Notes if converted at the holders’ option did not exceed the principal balance.

2045 Cheniere Convertible Senior Notes

In March 2015, we issued $625.0 million aggregate principal amount of 4.25% Convertible Senior Notes due 2045 (the “2045 Cheniere Convertible Senior Notes”) to certain investors through a registered direct offering. The 2045 Cheniere Convertible Senior Notes were issued with an original issue discount of 20% and accrue interest at a rate of 4.25% per annum, which is payable semi-annually in arrears. We have the right, at our option, at any time after March 15, 2020, to redeem all or any part of the 2045 Cheniere Convertible Senior Notes at a redemption price payable in cash equal to the accreted amount of the 2045 Cheniere Convertible Senior Notes to be redeemed, plus accrued and unpaid interest, if any, to such redemption date. The conversion rate will initially equal 7.2265 shares of our common stock per $1,000 principal amount of the 2045 Cheniere Convertible Senior Notes, which corresponds to an initial conversion price of approximately $138.38 per share of our common stock. The conversion rate is subject to adjustment upon the occurrence of certain specified events. We have the option to satisfy the conversion obligation with cash, common stock or a combination thereof.

We determined that the fair value of the debt component of the 2045 Cheniere Convertible Senior Notes was $304.3 million and the residual value of the equity component was $195.7 million as of the issuance date, excluding debt issuance costs. As of September 30, 2015, the carrying value of the equity component was $194.1 million. The debt component is accreted to the total principal amount due at maturity by amortizing the debt discount. The effective rate of interest to amortize the debt discount was approximately 9.4% as of September 30, 2015, and the remaining period over which the debt discount will be amortized was 29.5 years. As of September 30, 2015, the if-converted value of the 2045 Cheniere Convertible Senior Notes did not exceed the principal balance.

Interest expense, before capitalization, related to the 2021 Cheniere Convertible Unsecured Notes, the 2025 CCH HoldCo II Convertible Senior Notes and the 2045 Cheniere Convertible Senior Notes (together, the “Convertible Notes”) consisted of the following (in thousands):

|

| | | | | | | | | | | | | | | | |

| | Three Months Ended September 30, | | Nine Months Ended September 30, |

| | 2015 | | 2014 | | 2015 | | 2014 |

Interest per contractual rate | | $ | 46,782 |

| | $ | — |

| | $ | 97,991 |

| | $ | — |

|

Amortization of debt discount | | 7,233 |

| | — |

| | 20,948 |

| | — |

|

Amortization of debt issuance costs | | 1,133 |

| | — |

| | 1,748 |

| | — |

|

Total interest expense related to the Convertible Notes | | $ | 55,148 |

| | $ | — |

| | $ | 120,687 |

| | $ | — |

|

CTPL Term Loan

As of September 30, 2015, CTPL had borrowed the full amount of $400.0 million available under the CTPL Term Loan. The outstanding balance may be repaid, in whole or in part, at any time without premium or penalty.

2015 CCH Credit Facility

In May 2015, CCH entered into the 2015 CCH Credit Facility, which is being used to fund a portion of the costs associated with the development, construction, operation and maintenance of the CCL Project. The total commitment under the 2015 CCH Credit Facility is approximately $11.5 billion, comprising approximately $8.4 billion linked to Stage 1 of the CCL Project and the

CHENIERE ENERGY, INC. AND SUBSIDIARIES

NOTES TO CONSOLIDATED FINANCIAL STATEMENTS—CONTINUED

(unaudited)

Corpus Christi Pipeline and approximately $3.1 billion linked to Stage 2 of the CCL Project. Borrowings under the 2015 CCH Credit Facility may be refinanced, in whole or in part, at any time without premium or penalty; however, interest rate hedging and interest rate breakage costs may be incurred. As of September 30, 2015, CCH had $6.0 billion of available commitments and $2.4 billion of outstanding borrowings under the 2015 CCH Credit Facility.

CCH incurred $289.8 million of debt issuance costs in connection with the 2015 CCH Credit Facility. In addition to interest, CCH will incur a commitment fee at a rate per annum equal to 40% of the margin for LIBOR loans, multiplied by the outstanding undrawn debt commitments. The principal of the loans made under the 2015 CCH Credit Facility must be repaid in quarterly installments, commencing on the earlier of (1) the first quarterly payment date occurring more than three calendar months following project completion and (2) a set date determined by reference to the date under which a certain LNG buyer linked to the last Train to become operational is entitled to terminate its SPA for failure to achieve the date of first commercial delivery for that agreement. Scheduled repayments will be based upon a 19-year tailored amortization, commencing the first full quarter after the project completion and designed to achieve a minimum projected fixed debt service coverage ratio of 1.55:1.

The 2015 CCH Credit Facility contains conditions precedent for borrowings, as well as customary affirmative and negative covenants. The obligations of CCH under the 2015 CCH Credit Facility are secured by a first priority lien on substantially all of the assets of CCH and its subsidiaries and by a pledge by CCH HoldCo I of its limited liability company interests in CCH.

Under the terms of the 2015 CCH Credit Facility, CCH is required to hedge not less than 65% of the variable interest rate exposure of its senior secured debt.

SPL Working Capital Facility

In September 2015, SPL entered into a $1.2 billion SPL Working Capital Facility, which replaced the $325.0 million Senior Letter of Credit and Reimbursement Agreement that was entered into in April 2014 (the “SPL LC Agreement”). The SPL Working Capital Facility is intended to be used for loans to SPL (“Working Capital Loans”), the issuance of letters of credit on behalf of SPL (“Letters of Credit”), as well as for swing line loans to SPL (“Swing Line Loans”), primarily for certain working capital requirements related to developing and placing into operation the SPL Project. SPL may, from time to time, request increases in the commitments under the SPL Working Capital Facility of up to $760 million and, upon the completion of the debt financing of Train 6 of the SPL Project, request an incremental increase in commitments of up to an additional $390 million. As of September 30, 2015, SPL had $1.1 billion of available commitments, $127.6 million aggregate amount of issued Letters of Credit and no Working Capital Loans, Swing Line Loans or loans deemed made in connection with a draw upon a Letter of Credit (“LC Loans” and collectively with Working Capital Loans and Swing Line Loans, the “SPL Working Capital Facility Loans”) outstanding under the SPL Working Capital Facility. As of December 31, 2014, SPL had issued letters of credit in an aggregate amount of $9.5 million, and no draws had been made upon any letters of credit issued under the SPL LC Agreement.

SPL Working Capital Facility Loans accrue interest at a variable rate per annum equal to LIBOR or the base rate (equal to the highest of the senior facility agent’s published prime rate, the federal funds effective rate, as published by the Federal Reserve Bank of New York, plus 0.50% and one month LIBOR plus 0.50%), plus the applicable margin. The applicable margin for LIBOR SPL Working Capital Facility Loans is 1.75% per annum, and the applicable margin for base rate SPL Working Capital Facility Loans is 0.75% per annum. Interest on Swing Line Loans and LC Loans is due and payable on the date the loan becomes due. Interest on LIBOR Working Capital Loans is due and payable at the end of each applicable LIBOR period, and interest on base rate Working Capital Loans is due and payable at the end of each fiscal quarter. However, if such base rate Working Capital Loan is converted into a LIBOR Working Capital Loan, interest is due and payable on that date. Additionally, if the loans become due prior to such periods, the interest also becomes due on that date.

SPL incurred $27.5 million of debt issuance costs in connection with the SPL Working Capital Facility. SPL pays (1) a commitment fee on the average daily amount of the excess of the total commitment amount over the principal amount outstanding without giving effect to any outstanding Swing Line Loans in an amount equal to an annual rate of 0.70% and (2) a Letter of Credit fee equal to an annual rate of 1.75% of the undrawn portion of all Letters of Credit issued under the SPL Working Capital Facility. If draws are made upon a Letter of Credit issued under the SPL Working Capital Facility and SPL does not elect for such draw (an “LC Draw”) to be deemed an LC Loan, SPL is required to pay the full amount of the LC Draw on or prior to the business day following the notice of the LC Draw. An LC Draw accrues interest at an annual rate of 2.0% plus the base rate. As of September 30, 2015, no LC Draws had been made upon any Letters of Credit issued under the SPL Working Capital Facility.

CHENIERE ENERGY, INC. AND SUBSIDIARIES

NOTES TO CONSOLIDATED FINANCIAL STATEMENTS—CONTINUED

(unaudited)

The SPL Working Capital Facility matures on December 31, 2020, and the outstanding balance may be repaid, in whole or in part, at any time without premium or penalty upon three business days’ notice. LC Loans have a term of up to one year. Swing Line Loans terminate upon the earliest of (1) the maturity date or earlier termination of the SPL Working Capital Facility, (2) the date 15 days after such Swing Line Loan is made and (3) the first borrowing date for a Working Capital Loan or Swing Line Loan occurring at least three business days following the date the Swing Line Loan is made. SPL is required to reduce the aggregate outstanding principal amount of all Working Capital Loans to zero for a period of five consecutive business days at least once each year.

The SPL Working Capital Facility contains conditions precedent for extensions of credit, as well as customary affirmative and negative covenants. The obligations of SPL under the SPL Working Capital Facility are secured by substantially all of the assets of SPL as well as all of the membership interests in SPL on a pari passu basis with the SPL Senior Notes and 2015 SPL Credit Facilities.

Fair Value Disclosures

The following table (in thousands) shows the carrying amount and estimated fair value of our long-term debt:

|

| | | | | | | | | | | | | | | | |

| | September 30, 2015 | | December 31, 2014 |

| | Carrying Amount | | Estimated Fair Value | | Carrying Amount | | Estimated Fair Value |

2016 SPLNG Senior Notes, net of discount (1) | | $ | 1,660,023 |

| | $ | 1,684,923 |

| | $ | 1,656,502 |

| | $ | 1,718,621 |

|

2020 SPLNG Senior Notes (1) | | 420,000 |

| | 410,550 |

| | 420,000 |

| | 428,400 |

|

2021 SPL Senior Notes, net of premium (1) | | 2,009,090 |

| | 1,853,386 |

| | 2,010,177 |

| | 1,985,050 |

|

2022 SPL Senior Notes (1) | | 1,000,000 |

| | 930,000 |

| | 1,000,000 |

| | 1,020,000 |

|

2023 SPL Senior Notes, net of premium (1) | | 1,506,570 |

| | 1,344,614 |

| | 1,507,089 |

| | 1,476,947 |

|

2024 SPL Senior Notes (1) | | 2,000,000 |

| | 1,765,000 |

| | 2,000,000 |

| | 1,970,000 |

|

2025 SPL Senior Notes (1) | | 2,000,000 |

| | 1,755,000 |

| | — |

| | — |

|

2015 SPL Credit Facilities (2) | | 250,000 |

| | 250,000 |

| | — |

| | — |

|

2021 Cheniere Convertible Unsecured Notes, net of discount (3) | | 854,820 |

| | 894,160 |

| | 814,751 |

| | 1,025,563 |

|

2025 CCH HoldCo II Convertible Senior Notes (3) | | 1,003,667 |

| | 900,490 |

| | — |

| | — |

|

2045 Cheniere Convertible Senior Notes, net of discount (4) | | 305,421 |

| | 390,263 |

| | — |

| | — |

|

CTPL Term Loan, net of discount (2) | | 398,319 |

| | 400,000 |

| | 397,565 |

| | 400,000 |

|

2015 CCH Credit Facility (2) | | 2,428,000 |

| | 2,428,000 |

| | — |

| | — |

|

SPL Working Capital Facility (2) | | — |

| | — |

| | — |

| | — |

|

| |

(1) | The Level 2 estimated fair value was based on quotations obtained from broker-dealers who make markets in these and similar instruments based on the closing trading prices on September 30, 2015 and December 31, 2014, as applicable. |

| |

(2) | The Level 3 estimated fair value approximates the principal amount because the interest rates are variable and reflective of market rates and the debt may be repaid, in full or in part, at any time without penalty. |

| |

(3) | The Level 3 estimated fair value was calculated based on inputs that are observable in the market or that could be derived from, or corroborated with, observable market data, including our stock price and interest rates based on debt issued by parties with comparable credit ratings to us and inputs that are not observable in the market. |

| |

(4) | The Level 1 estimated fair value was based on unadjusted quoted prices in active markets for identical liabilities that we had the ability to access at the measurement date. |

NOTE 8—INCOME TAXES